84% tariffs slam U.S. dairy exports to China. Why can’t farmers capitalize on China’s milk shortage despite crashing prices & production?

EXECUTIVE SUMMARY: China’s dairy production is plummeting (-9.2% in 2025), but U.S. farmers face insurmountable barriers: 84% retaliatory tariffs, New Zealand’s duty-free dominance, and China’s lactose-intolerant population. While milk prices crashed by 15% and skim powder production dropped by 30%, structural issues like shrinking birth rates and economic stagnation limit demand. With FTAs favoring competitors and trade tensions escalating, experts urge dairy producers to pivot to Mexico, Southeast Asia, and value-added niches instead of chasing China’s shrinking market.

KEY TAKEAWAYS:

84% tariffs make U.S. dairy exports to China 104% more expensive than New Zealand’s duty-free shipments.

New Zealand controls 46% of China’s import market—their FTA advantage is irreversible without policy shifts.

China’s milk consumption growth is capped by lactose intolerance (87% in teens) and declining birth rates.

Diversify or die: USDA grants and co-ops offer lifelines for exploring Latin America, MENA, and specialty markets.

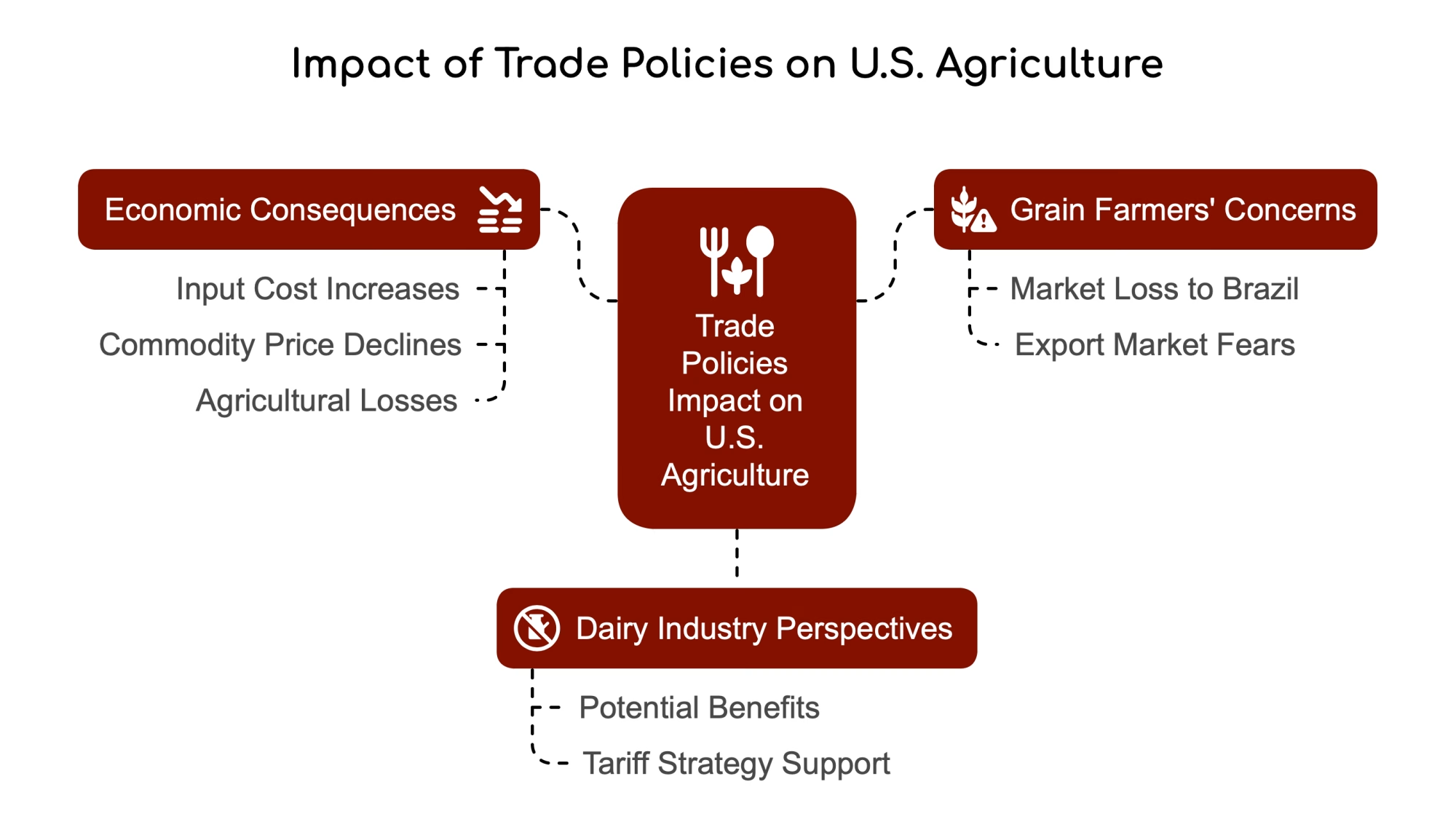

Economic headwinds (real estate crisis, youth unemployment) slash Chinese spending on “non-essential” dairy.

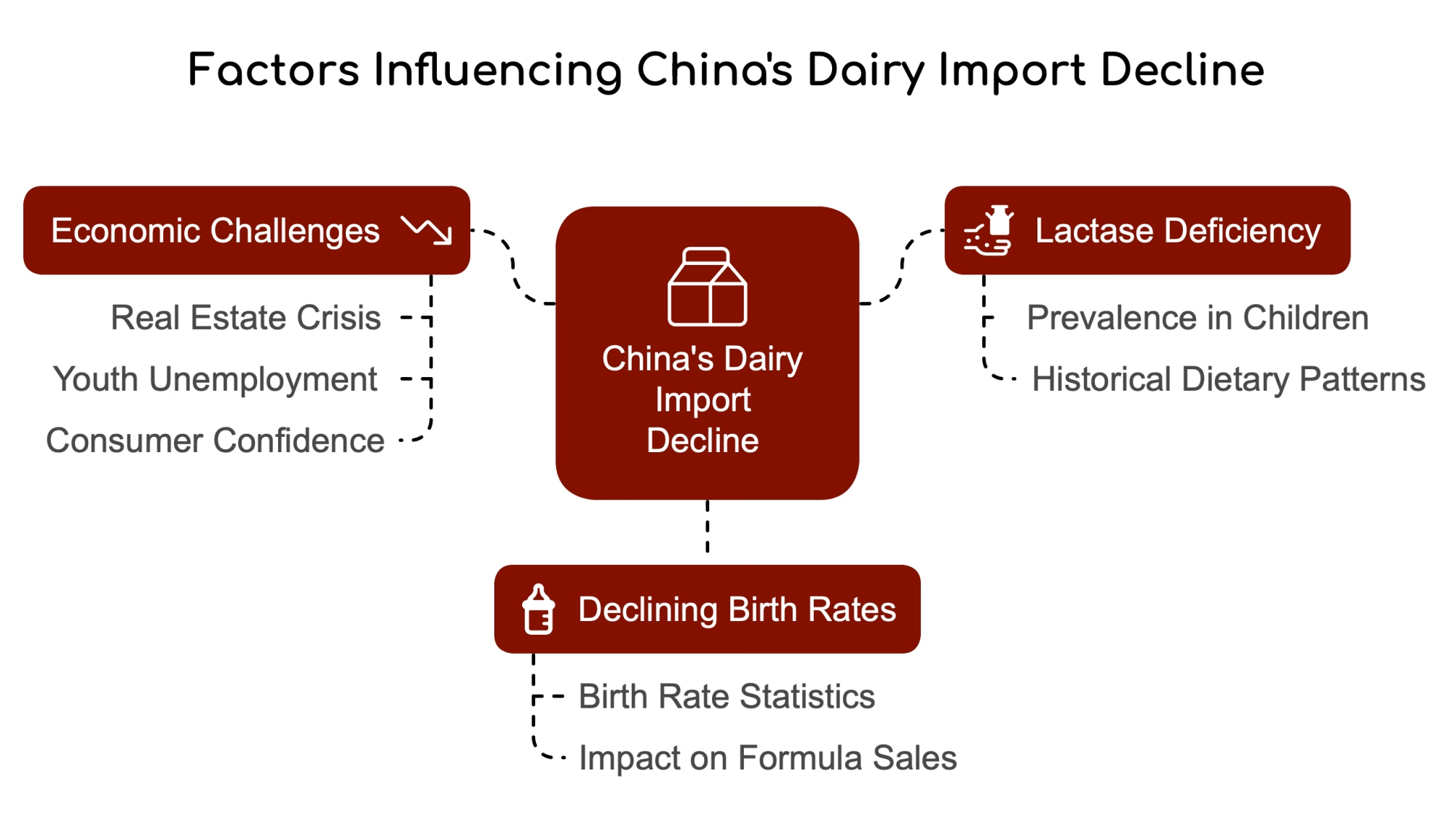

China’s dairy sector is shrinking fast, with milk collections down 9.2% in early 2025 compared to last year. Milk prices have dropped 15%, and skim milk powder production has plummeted by more than 30%. While this might sound like an opportunity for U.S. dairy exports, the reality is much more brutal.

Why China’s Dairy Market is Shrinking

After years of pushing hard to expand its dairy industry, China is now dealing with serious oversupply problems. Between 2018 and 2023, their milk production jumped by 27% (24.7 billion pounds) as part of their national plan to rely less on imports.

“Dairy production has remained stable, and the number of cows has been gradually adjusted,” China’s agriculture ministry stated in December 2024. “While the oversupply of milk will continue in the first half of 2025, it is expected that supply and demand imbalances will ease in the second half of the year.”

The problem? Chinese consumers aren’t drinking enough milk to keep up with all this production. Raw milk prices crashed from 4.38 yuan/kg in 2021 to just 3.14 yuan/kg by September 2024 – a brutal 28% drop forcing many smaller farms out of business.

Why China Isn’t Buying

Trouble Digesting Milk

Let’s face it – many Chinese people simply can’t comfortably digest milk. Studies show that lactase deficiency affects about 38.5% of Chinese children aged 3-5, jumping to a whopping 87% in older kids. This biological reality means milk has never been a staple in Chinese diets.

Declining Birth Rates

China’s birth rate has fallen, dropping from 13.03 births per thousand people in 2013 to just 6.39 in 2023. This hits infant formula sales hard – historically a major driver for dairy imports.

There was a small bump in 2024 during the “Year of the Dragon” (considered lucky in Chinese culture), but that’s a blip in the long-term downward trend.

Economic Challenges

China’s economy struggles with real estate problems, high youth unemployment, and weak consumer confidence. As USDEC notes: “China’s economy continues to be challenged on multiple fronts—a real estate crisis; elevated youth unemployment; underfunded local governments; deflation; and disappointing GDP growth—not to mention potential fallout from trade battles with the U.S.”

When money’s tight, dairy products are often the first thing cut from shopping lists.

The Competitive Landscape: Why New Zealand Wins

New Zealand’s Duty-Free Advantage: As of January 1, 2024, all New Zealand dairy products enter China completely duty-free. This gives Kiwi producers roughly $350 million in annual tariff savings compared to U.S. suppliers.

Dominant Market Position: New Zealand commands a 46% share of China’s dairy import market. Their exports to China jumped significantly in late 2024, especially milk powder, butter, and cheese.

U.S. Export Decline: Meanwhile, U.S. dairy exports to China tanked in 2024, falling to $584 million – the lowest since 2020. Overall volume dropped 9%, according to USDEC.

Bottom Line: New Zealand’s free trade advantage is practically impossible to overcome without significant policy changes. Any import opportunities created by China’s production decline will benefit New Zealand, not U.S. producers.

The Trade War Impact: 84% of Tariffs Close the Door

The trade relationship between U.S. dairy and China has gone from bad to worse. Here’s how quickly things escalated:

Tariff Timeline:

February 1, 2025: U.S. slaps 10% tariff on all Chinese imports

March 3, 2025: U.S. increases tariff to 20%

March 4, 2025: China announces 10% retaliatory tariff on U.S. dairy (effective March 10)

April 2, 2025: U.S. imposes additional 34% “reciprocal” tariff

April 4, 2025: China matches with a 34% retaliatory tariff (effective April 10)

April 9, 2025: U.S. increases reciprocal tariff to 84%

April 9, 2025: China immediately matches with an 84% retaliatory tariff (effective April 10)

“China will impose a 10% tariff on US dairy products starting March 10 as the trade war intensifies,” reported The Bullvine in early March.

As of today (April 9, 2025), the U.S. has just announced an increase of its tariff on China from 34% to 84%, with China immediately matching. Starting tomorrow, virtually all U.S. dairy products entering China will face an additional 84% tariff on top of existing rates – effectively slamming the door shut on exports.

Quick Takeaways for Dairy Farmers

Small Operations: Focus on domestic specialty markets; consider joining cooperatives with diversified export portfolios

Medium Operations: Explore USDA Market Access Program funding for new market development in Southeast Asia and Latin America

Large Operations: Evaluate product mix to target markets less impacted by tariffs; consider joint ventures with partners in FTA countries

Bottom Line for Dairy Producers

The brutal truth? U.S. dairy producers shouldn’t expect any meaningful export opportunities to China shortly. The triple whammy of sky-high tariffs, weak Chinese consumer demand, and competition from duty-free suppliers like New Zealand create a perfect storm that effectively locks us out of the market.

3 Steps for Farmers:

Explore USDA Market Access Program grants for export market development (applications due June 14, 2025)

Contact your co-op or industry association about market diversification strategies

Look beyond China to Mexico, Southeast Asia, and the Middle East/North Africa markets

This trade war highlights why putting all your eggs in one export basket is risky. The most brilliant move now is to diversify your markets and focus on regions where U.S. dairy still has competitive advantages.

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

EXECUTIVE SUMMARY: President Trump’s tariffs have ignited a global trade war with dire consequences for the U.S. dairy industry, risking .6B in farm revenue and triggering retaliatory measures from key markets like China and Canada. Mid-sized farms could lose up to $56K annually, while organic producers face soaring feed costs. Industry leaders remain divided, with some advocating for tariffs as leverage against trade barriers, while farmers scramble to secure contracts and diversify exports. The article outlines actionable survival strategies, including USDA programs and feed efficiency investments, as the sector balances uncertainty with cautious optimism for long-term trade reforms.

KEY TAKEAWAYS:

$16.6B at Risk: Retaliatory tariffs threaten nearly a quarter of U.S. dairy exports, with Mexico and China as top vulnerable markets.

Farm-Level Crisis: Medium-sized operations face income drops up to $56K/year; organic feed costs may spike $1,200/month.

Survival Playbook: Lock pre-tariff contracts, leverage USDA programs, and target emerging Southeast Asian markets.

Industry Divide: Leaders split on tariffs as tools for trade reform vs. immediate economic harm to farmers.

Long Game: Strategic adaptations like feed-efficient breeds and policy engagement could determine sector resilience.

The U.S. dairy industry faces unprecedented challenges as President Trump’s sweeping tariff policies take effect, threatening .2 billion in annual exports and reshaping the global trade landscape. With retaliatory measures from key trading partners looming, dairy farmers and processors must navigate market volatility, rising input costs, and potential long-term disruptions to established export channels.

Tariff Tensions Spark Global Dairy Trade War

President Trump’s announcement of a baseline 10% tariff on all imports, with higher targeted rates for specific countries, has sent shockwaves through the dairy sector. China and Canada, two of America’s top dairy export destinations, have already imposed retaliatory tariffs. China has placed 10% of its duties on some milk products, while Canada’s package includes 25% tariffs on American cheese, butter, and dairy spreads.

The timing couldn’t be more precarious for U.S. dairy, with Mexico, China, and Canada among its top export markets:

Top U.S. Dairy Export Markets (2024)

Volume (Metric Tons)

% of Total Exports

Value (USD Millions)

Mexico

576,000

24.8%

$1,840

Southeast Asia

395,000

17.0%

$1,320

China

311,000

13.4%

$970

Canada

246,000

10.6%

$810

Middle East/North Africa

172,000

7.4%

$580

Dairy Industry Voices: Mixed Reactions to Tariff Strategy

While some industry leaders see potential leverage in the tariffs, others warn of devastating consequences. Gregg Doud, President and CEO of the National Milk Producers Federation, cautiously supports the measures:

“Tariffs can be a useful tool for negotiating fairer terms of trade. To that end, we are glad to see the administration focusing on long-time barriers to trade that the European Union and India have imposed on our exports.”

“We’re facing a double challenge — lower prices and increasing costs. We can’t simply raise our prices at the market because all our expenses are increasing, leaving us in a difficult position.”

Economic Impact: From Farm to Market

The tariffs are expected to have severe economic consequences:

Potential farm-gate revenue losses of up to $16.6 billion due to trade tensions.

A medium-sized farm in Wisconsin with about 250 cattle could decrease income by up to $56,000 per year.

For organic dairy farmers, grain expenses could increase by $1,200 monthly due to tariffs on Canadian imports.

CME dairy futures have already reacted, with milk futures down 12% since February. The USDA has lowered its 2025 milk production forecast to 227.2 billion pounds, down 0.8 billion from previous estimates.

Dairy Survival Checklist: Strategies for Weathering the Storm

Secure pre-tariff contracts where possible to lock in more favorable terms.

Leverage USDA Dairy Margin Coverage programs to protect against price volatility.

Explore emerging markets in Southeast Asia to diversify export destinations.

Conduct a thorough audit of feed inputs and export contracts to stress-test 2025 margins.

Consider investing in feed-efficient breeds to mitigate rising input costs.

Looking Ahead: Uncertainty and Opportunity

While the immediate outlook appears challenging, some industry experts see potential benefits. The National Milk Producers Federation and U.S. Dairy Export Council have expressed hope that targeted tariffs could help address longstanding trade barriers, particularly with the EU and Canada.

Krysta Harden, President and CEO of the U.S. Dairy Export Council, states:

“President Trump’s commitment to addressing certain unfair and harmful trade policies that American dairy farmers and manufacturers have long faced in the global marketplace can yield positive results if the tariffs announced today are used as leverage to remedy the various trade barriers facing our exporters.”

Adaptability and strategic planning will be key as the dairy industry navigates these turbulent waters. Farmers and processors must stay informed, leverage risk management tools, and actively engage with policymakers to ensure their voices are heard in ongoing trade negotiations.

The stakes have never been higher for U.S. dairy. Will these tariffs lead to more equitable global trade or trigger a costly market disruption? Only time will tell, but one thing is sure: American dairy farmers’ resilience and innovation will be tested in the months and years ahead.

How U.S. Farmers Could Benefit from Canada’s Trade Barriers Learn how Trump’s reciprocal tariffs on Canadian dairy could reshape trade dynamics, potentially benefiting U.S. farmers while exposing Canadian producers to increased competition.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Trump’s tariff gamble: Dairy sees trade war leverage while grain fears collapse. Will new tariffs crack EU cheese barriers or spark Chinese retaliation?

EXECUTIVE SUMMARY: President Trump’s new tariffs on major trade partners have divided agriculture, with dairy leaders cautiously supporting the measures as potential leverage against long-standing EU cheese restrictions (blocking $168M in exports) and Canada’s quota system (where U.S. exports fill less than 30% of allowed volumes). However, grain producers warn of permanent market loss to Brazil, citing 2018’s $25B trade war damage. The tariffs target EU GIs, India’s lactose taxes, and China’s retaliatory risks, with dairy advocating for swift negotiations to dismantle barriers. While the strategy could pressure reforms, farmers face uncertainty as implementation begins today.

KEY TAKEAWAYS:

Canada’s dairy paradox: 200%+ tariffs exist but apply only if exports exceed quotas—a scenario that’s never occurred due to systemic barriers.

EU’s $168M cheese blockade: Geographical Indications block U.S. products from using names like “feta,” costing millions annually.

China gamble: 34% tariffs risk retaliation in America’s third-largest dairy export market ($584M), already down 12% YoY.

Sector divide: Dairy backs tariffs as negotiation tools; grain growers fear irreversible market loss, per Purdue’s Ag Barometer.

TRQ reality: Complex tariff-rate quotas govern global dairy trade, with most countries failing to fill allocated volumes.

As President Trump’s newly announced tariffs are set to take effect tomorrow, dairy industry leaders are expressing cautious optimism that these measures could help address longstanding trade barriers that have hindered U.S. dairy exports. The tariff plan, which includes both a baseline 10% duty on all imports and higher targeted rates for specific countries, is being viewed by some dairy representatives as a potential lever to create more equitable trade conditions.

Breaking Down Trump’s Bold Tariff Strategy for Dairy Markets

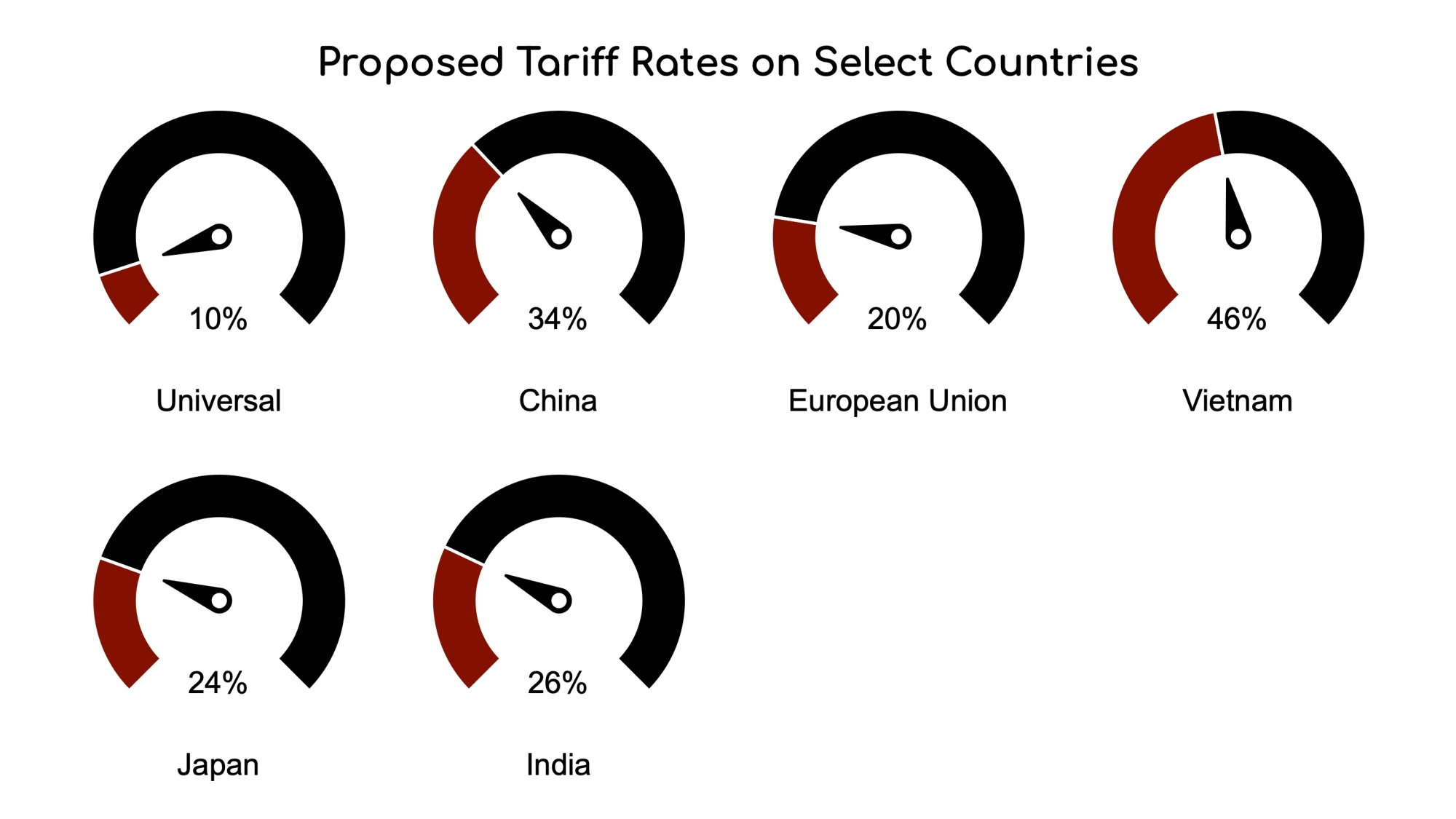

President Donald Trump unveiled his tariff plan during a “Make America Wealthy Again” event at the White House Rose Garden, announcing a universal 10% tariff on all imports beginning April 5, 2025, with additional targeted tariffs on countries with which the U.S. has significant trade deficits starting April 9. The higher rates include 34% for China, 20% for the European Union, and targeted percentages for countries including Vietnam (46%), Japan (24%), and India (26%).

Unlike some agricultural sectors expressing concern, dairy industry leaders offered measured support for the administration’s approach. Gregg Doud, President and CEO of the National Milk Producers Federation (NMPF) framed the tariffs as potentially beneficial for U.S. dairy producers.

“Tariffs can be a useful tool for negotiating fairer terms of trade,” Doud stated. “We are glad to see the administration focusing on long-time barriers to trade that the European Union and India have imposed on our exports.”

Krysta Harden, President and CEO of the U.S. Dairy Export Council (USDEC), echoed this sentiment, emphasizing that a “firm hand and decisive approach” is particularly needed with the European Union and India “to correct their distortive trade policies and mistreatment of American agriculture.”

The USMCA Paradox: How Canada Blocks U.S. Milk Despite “Zero” Tariffs

President Trump has specifically highlighted Canadian dairy policies as problematic, claiming Canada imposes tariffs of 250-270% on U.S. dairy products. While these high rates do exist on paper, the reality is more complex and often misrepresented.

These triple-digit tariffs would only apply if U.S. exports exceeded predetermined quota thresholds established under the United States-Mexico-Canada Agreement (USMCA), which Trump himself negotiated during his first term. Below these quotas, American dairy sales to Canada face zero tariffs.

The critical fact often overlooked is that U.S. dairy exports have never come close to reaching these quota limits. For dairy products subject to a quota year tariff, the average fill rate as of March 2025 was only 21.24%. In practice, this means “these tariffs are not actually paid by anyone,” according to agricultural economists.

“We’ve never hit 50% of our tariff-free milk quota. Canada’s system is designed to look open while keeping U.S. products out.”

Becky Rasdall Vargas, IDFA Senior VP of Trade Policy

Dairy Product

TRQ Year Basis

2024 Fill Rate

March 2025 Fill Rate

Cheese & Curd

Calendar

18%

14%

Skim Milk Powder

Quota (Aug-Jul)

32%

23%

Fluid Milk

Calendar

29%

19%

Butter

Quota (Aug-Jul)

41%

27%

The real issue, according to U.S. dairy representatives, lies in Canada’s implementation of the quota system. Becky Rasdall Vargas, senior vice president of trade and workforce policy at the IDFA, argues that “Canada imposes unfair barriers that make it increasingly difficult for U.S. products to enter the Canadian market”.

“Our complaint is we’re not able to get anywhere near the quota cap, even though we have buyers who tell us they would like to bring in our product,” Rasdall Vargas explained.

USMCA Promised Big Gains for Dairy—But Delivery Falls Short

The USMCA established significant growth in market access for U.S. dairy exports to Canada, with TRQ volumes scheduled to increase substantially over the agreement’s implementation period.

Product Category

Year 1 TRQ

Year 6 TRQ

Year 19 TRQ

Growth Mechanism

Cheese

10,416 MT

15,624 MT

17,860 MT

+25% Y3, +20% Y6, +1% annually

Skim Milk Powder

5,000 MT

7,500 MT

8,575 MT

+50% Y2, +1% annually

Fluid Milk

7,000 MT

10,500 MT

12,005 MT

+33% Y3, +1% annually

Butter

3,000 MT

4,500 MT

5,145 MT

+50% Y2, +1% annually

Under CUSMA (the Canadian term for USMCA), butter TRQs increased by 25% in the 2023/24 dairy year. With an 81.3% fill rate, this year’s rate is lower than last year’s at 97%, indicating some challenges in fully utilizing the expanded market access.

$168 Million Lost: How EU Cheese Rules Block American Exports

The relatively moderate 20% tariff on European Union goods reflects a strategic approach to a complex trade relationship. According to Doud, this rate is “a bargain for the EU considering the highly restrictive tariff and nontariff barriers the EU imposes on our dairy exporters.”

One of the most contentious issues between U.S. and EU dairy trade involves Geographical Indications (GIs), which the EU uses to protect regional food names. These designations prevent U.S. cheesemakers from labeling their products as “feta” or “gorgonzola” when exporting to EU markets, as these terms are reserved for regionally produced cheeses.

The EU’s GI restrictions effectively “erase American products from store shelves overseas,” as Krysta Harden of USDEC has noted, blocking $168 million in potential U.S. cheese exports in 2024 alone.

“If Europe retaliates against the United States, we encourage the administration to respond strongly by raising tariffs on European cheeses and butter,” Doud stated, signaling the industry’s support for a tough stance on this issue.

China’s $584 Million Dairy Market at Risk: Will Retaliation Follow?

The highest targeted tariff rate—34% on Chinese goods—raises significant questions for U.S. dairy exports to what has become America’s third-largest dairy export market, worth $584 million in 2024. U.S. dairy exports to China declined by 12% year-over-year in 2024, reaching their lowest level since 2020, a trend that could be exacerbated by new trade tensions.

China has previously imposed retaliatory tariffs on U.S. dairy imports in response to earlier Trump-era tariffs, with dairy products facing a 10% duty. During the 2018 trade war, these retaliatory measures cost dairy farmers $1.5 billion in lost revenue. With the new 34% U.S. tariff set to take effect April 9, there is concern about potential escalation.

“China will take necessary measures to firmly safeguard its legitimate interests against these WTO-violating tariffs.”

Guo Jiakun, Chinese Foreign Ministry Spokesperson

Chinese officials have already signaled their opposition to the new tariffs. Foreign Ministry Spokesperson Guo Jiakun stated that the measures “seriously violate WTO rules” and promised that “China will resolutely take countermeasures to safeguard its legitimate interests”.

The Trade Barrier Paradox: U.S. Import Quotas Remain Unfilled Too

While much attention focuses on barriers to U.S. exports, it’s worth noting that many countries face challenges accessing the U.S. market as well. Current data shows varying utilization rates for dairy TRQs established under U.S. free trade agreements:

Trade Partner

TRQ Type

2024 Utilization

Key Barrier

Canada

Cheese

1%

Quota allocation complexity

EU

Butter

44%

GI restrictions

Mexico

SMP

8%

Section 232 tariffs

This data from the USDA Dairy Import Circular shows that trade barriers can flow in both directions, with complex quota systems sometimes limiting the effectiveness of market access provisions.

“We’re Handing China to Brazil”: Grain Farmers Fear Permanent Market Loss

While dairy industry representatives see potential benefits in Trump’s tariff strategy, grain producers have expressed significant concerns. Chase Dewitz, who operates a large farming operation in North Dakota, worries about permanent market loss.

“We’re handing China to Brazil,” warns Dewitz, reflecting grain growers’ fears of losing export markets. “I think there’s going to be some pain here for a while, and the biggest thing is these export markets.”

During the 2018 trade war with China, U.S. agriculture experienced more than $25 billion in losses. The United States has yet to fully recover its former market share of soybean exports to China, the world’s largest buyer of the commodity.

“Tariffs tear us apart—raising input costs while crushing commodity prices. This isn’t trade policy; it’s economic vivisection.”

Vance Ehmke, Kansas Farmer (6th Generation)

“These tariffs are just absolutely bad news,” said Vance Ehmke from the western Kansas farm his ancestors homesteaded in 1885. “They cause the prices for everything that we buy to go up, and the price for everything that we sell to go down. I mean, it is being economically drawn and quartered”.

Tariff Rate Quotas Explained: Why the “Milk Tank” Analogy Matters

Think of Tariff Rate Quotas (TRQs) like a milk tank—fill it tax-free, but overflow costs steeply. Both the U.S. and Canada use this system for dairy products, allowing a certain number of imports at low or zero tariffs, with significantly higher rates applied to imports exceeding these quotas.

For example, while U.S. dairy exports to Canada face potential tariffs of 241-298.5% if they exceed quota limits, these exports have never reached even 50% of their tariff-free allocation. Similarly, Canadian butter exported to the U.S. faces no tariffs under quota thresholds but would be subject to over-quota tariffs of about 24-39%.

Understanding these mechanisms is crucial for dairy producers navigating international markets and evaluating the potential impact of Trump’s new tariff strategy.

Will Your Dairy Operation Benefit or Suffer Under New Tariffs?

As the April 5 implementation date approaches tomorrow, dairy producers should consider how these tariffs might affect their specific operations. Would a 34% tariff on Chinese imports benefit your bottom line? Or would retaliatory bans on milk powder erase your profits?

The contrasting reactions between dairy and grain sectors highlight the diverse impacts trade policies can have across different agricultural commodities. While dairy organizations see an opportunity to leverage tariffs for negotiations with problematic partners like the EU, India, and Canada, they also emphasize the importance of quickly resolving tensions with constructive trading partners.

“Through productive negotiations, this administration can help achieve a level playing field for U.S. dairy producers by tackling the numerous tariff and nontariff trade barriers that bog down our exports,” Doud stated.

Tariffs as Leverage: Strategic Tool or Economic Self-Harm?

As the dairy industry navigates the complex landscape of international trade, the response to Trump’s tariff announcement reflects a strategic calculation: potential short-term disruption weighed against the possibility of addressing persistent barriers to U.S. dairy exports.

“Every farmer says trade needs fixing—until it affects their bottom line. Well, buckle up: this storm will hit us all.”

James Mintert, Purdue Ag Economist

“Broad and prolonged tariffs on our top trading partners and growing markets will risk undermining our investments, raising costs for American businesses and consumers, and creating uncertainty for American dairy farmers and rural communities,” warns Becky Rasdall Vargas of the IDFA.

The dairy sector appears poised to support targeted use of tariffs while advocating for swift negotiations to expand export opportunities and eliminate both tariff and non-tariff barriers that have limited U.S. dairy’s global competitiveness. As implementation begins tomorrow, the industry will be watching closely to see whether these tariffs serve as effective negotiating tools or trigger costly trade conflicts.

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

American cheese shatters the billion-pound export barrier as global demand surges! With 17% growth pushing exports past 508,000 metric tons and the U.S. crowned the #1 cheese supplier, discover how record-breaking dairy exports reshape farm economics and why the world can’t get enough of what your cows produce.

EXECUTIVE SUMMARY: U.S. dairy exports have reached unprecedented heights, with cheese shipments breaking the billion-pound barrier (508,808 metric tons) and total export values hitting $8.2 billion in 2024 – the second-highest ever. While total export volume dipped slightly (-0.4%), the industry’s strategic shift to higher-value products like cheese has created additional value for producers. With exports representing 18% of U.S. milk production and massive cheese processing expansion underway, American dairy farms producing high-component milk are uniquely positioned to benefit from this global demand surge.

KEY TAKEAWAYS:

U.S. cheese exports smashed records, reaching 508,808 metric tons in 2024 (17% year-over-year growth)

The United States is now the #1 cheese supplier to the world, with exports exceeding the billion-pound mark for the first time

Overall, the value of dairy exports increased by 2% to $8.2 billion despite a slight 0.4% decline in volume.

Mexico remains the top U.S. dairy customer, with exports growing 7% in 2024

More than 450,000 metric tons of new cheese production capacity coming online between 2023-2026

Exports now represent 18% of U.S. milk production, up from previous years

Latin America showed exceptional growth, with record values for Mexico, Central America, and South America

As milk trucks rumble across frost-covered driveways before dawn, the familiar hum of their engines signals not just another local delivery but the beginning of a global journey. The sweet, grassy aroma of fresh milk that filled your bulk tank this morning might soon become cheese savored by families in Mexico City, Tokyo, or Seoul. The first months of 2025 have confirmed what industry insiders call a transformative shift in U.S. dairy’s position on the world stage – with American cheese now dominating international markets at record volumes.

American cheese exports reached 508,808 metric tons in 2024, making the U.S. the world’s leading cheese supplier. Processing plants across the country are working at capacity to meet international demand.

U.S. CHEESE CRUSHES EXPORT RECORDS: FIRST-EVER BILLION-POUND MILESTONE

American cheese has officially conquered global dinner tables in a way that would make our grandfathers’ jaws drop. U.S. cheese exports reached a staggering 508,808 metric tons (1.12 billion pounds) in 2024, a 17% jump from the previous record. The sharp, nutty aroma of aged cheddar and the creamy reliability of American mozzarella are winning international fans at an unprecedented rate.

Think about it this way: if you lined up all the cheese America exported last year, it would stretch from New York to Los Angeles and back – twice. Approximately 45 billion grilled cheese sandwiches worth of dairy protein are feeding families worldwide.

Throughout 2024, the U.S. leveraged competitive pricing, consistent quality, and strong production capacity to position itself as the world’s leading cheese supplier. This global leadership directly translated to more vigorous milk checks for farmers, providing critical revenue streams when input costs for feed, labor, and compliance remained stubbornly high.

“The United States is already the No. 1 cheese supplier to the world, and we know we can strengthen our position in the years ahead,” noted Krysta Harden, president and CEO of the U.S. Dairy Export Council. This statement isn’t just industry optimism – it’s backed by complex numbers showing American cheese consistently winning market share from European and Oceanian competitors.

MASSIVE PROCESSING EXPANSION CREATES NEW MILK MARKETS

The distinctive whine of construction equipment at new cheese plant sites represents music to dairy farmers’ ears. The tang of freshly welded stainless steel and the rhythmic hum of new pasteurizers being tested signal more than industrial development – they represent crucial new markets for your milk.

More than 450,000 metric tons of new U.S. cheese production capacity will come online between 2023 and 2026, creating critical outlets at a time when domestic consumption alone cannot absorb increasing production.

Your dairy operation is increasingly connected to global markets, with exports accounting for 18% of U.S. milk production. Every tanker leaving your farm potentially contributes to America’s export success.

For dairy farms in regions like the Upper Midwest, Southwest, and Idaho, where these plants are growing, the investment signals long-term confidence in American dairy’s future. Manufacturers wouldn’t be pouring millions into stainless steel if they weren’t betting on your ability to supply high-quality milk for decades.

The timing couldn’t be better, as component levels in American milk continue their upward march. Today’s Holstein herds regularly produce milk testing above 4.0% fat and 3.2% protein, which would have seemed impossible twenty years ago. These higher component concentrations translate directly to cheese yield, creating a win-win for processors and the farmers supplying them.

COMPONENT ENHANCEMENT: YOUR STRATEGY FOR EXPORT PROSPERITY

The global cheese boom means your focus on components has never been more valuable. Farms producing milk with above-average butterfat and protein are capturing premium prices as processors compete for milk that yields more cheese per vat.

What practical steps can boost your components and position your operation for export market success?

Nutritionists point to several evidence-based strategies: increasing the forage-to-concentrate ratio (particularly with high-quality corn silage), precisely balancing amino acids, and ensuring adequate, effective fiber to maintain butterfat. Leading herds also make genetic selection decisions heavily weighted toward component traits, recognizing that minor percentage improvements multiply millions of pounds of lifetime production.

John Wilson, a third-generation Wisconsin dairy farmer, implemented these strategies and saw dramatic results. “We increased our components by focusing on cow comfort, forage quality, and genetics. Over three years, our fat test increased from 3.8% to 4.2%, and we’re capturing a premium of almost per hundredweight,” Wilson explains as he walks through his milking parlor where the rhythmic pulse of vacuum pumps provides a steady backbeat to his morning routine. “With exports driving cheese demand, these components are our ticket to staying profitable.”

While cheese export growth dominates headlines, the overall dairy export landscape shows a more complex picture directly impacting your bottom line. Total U.S. dairy exports slipped by 0.4% in milk solids equivalent terms during 2024, primarily due to weakness in nonfat dry milk/skim milk powder (NFDM/SMP) markets.

NFDM/SMP exports faced significant challenges, with December 2024 volumes plunging 23% (14,992 metric tons) to 49,565 metric tons – the first time monthly sales fell below 50,000 since July 2019. This powder performance dip meant milk could have found international homes instead of pressured domestic markets.

U.S. NFDM/SMP exports declined 8% for the entire year, mainly due to reduced U.S. production, limited available supply, and pricing issues that favored competitors. The contrast between thriving cheese exports and struggling powder markets highlights why diversified export strategies matter for industry stability.

Despite the volume dip, the value of U.S. dairy exports reached $8.2 billion in 2024 – a 2% increase ($202 million) and the second-highest total ever, trailing only 2022’s $9.7 billion. This value growth reflects the industry’s strategic shift toward higher-value products like cheese, creating more dollars per hundredweight for producers.

Product Category

Volume (Metric Tons)

Year-over-Year Change

Cheese

508,808

+17%

NFDM/SMP

Year total not specified

-8%

Total Dairy Exports (MSE)

Not specified

-0.4%

Total Export Value

$8.2 billion

+2% ($202M)

Source: U.S. Dairy Export Council, 2025

MEXICO & LATIN AMERICA: THE MARKETS DRIVING YOUR MILK CHECK

When you watch tank trucks pull away from your farm, the diesel exhaust mingling with the sweet scent of fresh milk, you might not realize how many are ultimately bound for Mexican dinner tables. Latin America has emerged as the foundation of American dairy export success, with Mexico alone purchasing $2.47 billion in U.S. dairy products in 2024.

As you sip your morning coffee, farmers across Mexico are incorporating U.S. cheese into breakfast dishes – the sizzle of melting cheese in quesadillas and the stretch of mozzarella in countless dishes, driving a 7% increase in exports to our southern neighbor last year. This growth isn’t just happening in Mexico – U.S. dairy export volume gained across South America (+6%) and Central America, with countries like Costa Rica, Guatemala, and El Salvador all setting new import records.

Mexico’s growing appetite for U.S. dairy drove $2.47 billion in exports in 2024, supporting milk prices for American farmers. The popularity of cheese-based dishes throughout Latin America creates steady demand for U.S. dairy products.

What is the significance of your operation? This regional strength creates crucial outlets for American milk production that would otherwise depress domestic prices. Every semi-truck of cheese crossing the southern border represents milk that doesn’t weigh down your local market.

“I’ve completely changed how I think about our market,” says Maria Hernandez, whose 850-cow operation in California produces high-component milk primarily destined for export markets. Standing in her feed alley as the distinctive sound of mixer wagons and the earthy scent of TMR fill the air, she continues, “We’re essentially feeding families in Mexico City and Lima now, not just our domestic market. That global connection has made me more focused on consistency and quality than ever.”

Market

Export Value (2024)

Mexico

$2.47 Billion

Canada

$1.14 Billion

Total Value to All Markets

$8.2 Billion

Source: International Dairy Foods Association, 2025

NAVIGATING EXPORT HEADWINDS: TRADE TENSIONS AND MARKET VOLATILITY

The road to export growth isn’t without potholes that could jolt your operation’s planning. U.S. dairy exporters faced significant headwinds in 2024, including Chinese demand contraction for the third straight year and intensified competition from New Zealand and European suppliers aggressively targeting traditional U.S. export destinations.

U.S. dairy exports to China reached their lowest annual total since 2020, a troubling trend given China’s critical market for American whey products used in its massive pork industry. Meanwhile, Oceanian suppliers have reworked their product mix to target Latin American and Southeast Asian markets, driving margin compression in regions where U.S. dairy previously enjoyed more substantial positions.

Trade policy uncertainty adds another layer of complexity to your farm planning. In early 2025, President Donald Trump agreed to a 30-day pause on tariff threats against Canada and Mexico. Since these nations represent more than 40% of U.S. dairy exports, any tariff implementation could trigger retaliatory measures that disproportionately target agricultural products – potentially stranding significant milk volumes in domestic markets and pressuring prices.

How should your farm navigate these uncertainties? Financial advisors recommend maintaining higher cash reserves than historical norms, carefully evaluating major capital expenditures, and considering risk management tools like forward contracting and futures markets to lock in profitability during favorable windows.

YOUR FARM’S STAKE IN THE EXPORT BOOM: POSITIONING FOR PROFIT

As morning fog lifts from your pastures and the first rays of sunlight catch the steam rising from cows’ breath in the cool morning air, the international connections of your operation become increasingly apparent. Approximately one day’s milk produced on America’s dairy farms each week is exported – roughly 18% of all production. Your contribution to feeding the world has never been more direct or economically significant.

Expanding processing capacity proves that your future is increasingly tied to global markets. New cheese plants online between 2023 and 2026 represent massive bets on American dairy’s international competitiveness. These facilities wouldn’t exist without confidence in your production capacity and the world’s appetite for what your cows produce.

For forward-thinking producers, this export-driven future demands strategic decisions. Component enhancement provides immediate returns, but other factors increasingly influence your competitiveness in export-focused processing:

Milk with superior microbiological quality enjoys longer shelf-life in international transport

Consistent component levels throughout the year (avoiding seasonal swings) create processing efficiencies

Sustainability credentials increasingly influence purchasing decisions, particularly in premium markets

On-farm practices that minimize heat-sensitive protein damage produce superior yields in high-heat cheese applications typical in export markets.

“We’ve shifted our management to focus on what I call ‘exportable milk quality,'” explains Thomas Johnson, whose 450-cow Michigan dairy consistently earns quality premiums. The crisp smell of sanitizer and the gentle whoosh of automatic detachers provide the backdrop as he monitors the milking process. “Beyond basic components, we’ve reduced our somatic cell count below 100,000, implemented cooling that gets milk below 38°F within 30 minutes of harvest, and documented our carbon footprint reduction. These steps directly translate to premiums from processors serving export markets.”

Metric

Value

Total U.S. Dairy Export Value (2024)

$8.2 Billion

Year-over-Year Value Increase

$202-223 Million

Percentage of U.S. Milk Production Exported

18%

Jobs Supported by U.S. Dairy Industry

3.2 Million

Economic Contribution to U.S. Economy

$800 Billion

Sources: U.S. Dairy Export Council, International Dairy Foods Association, 2025

THE FUTURE IS GLOBAL: WHY EXPORTS MATTER MORE THAN EVER

The billion-pound cheese milestone represents more than just a number – it symbolizes American dairy’s transformation from a domestic industry to a global powerhouse. This global connection provides crucial stability for your operation as domestic consumption patterns evolve and production efficiency continues improving.

As you walk through your barn today, the familiar sounds of cows crunching feed and the rhythmic pulse of milking equipment serve as the backdrop to an increasingly global enterprise. The milk your cows produce increasingly travels to dinner tables your grandparents couldn’t have imagined reaching. From Mexican pizza toppings to Japanese cheese boards, American dairy products have become essential ingredients in global cuisine.

“Our industry is poised to become the world’s leading supplier of dairy products thanks to the resilience and innovation of the American dairy industry,” said Michael Dykes, president and CEO of the International Dairy Foods Association. “Overall, U.S. dairy exports are performing well, but we can do more. With new trade agreements that remove obstacles and increase market access, we wouldn’t just break records – we would redefine the global dairy landscape for decades to come.”

The path forward requires both individual farm adaptation and collective industry action. Your focus on components, quality, and sustainability positions your operation for success while industry organizations work to secure favorable trade terms and develop new markets. This partnership between progressive producers and forward-thinking processors has transformed American dairy from a regional industry into a global powerhouse – with your farm playing a crucial role in feeding a hungry world.

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

A 19-year tariff phaseout has unlocked Central America’s dairy market, but melting ice cream and EU rivals threaten gains. Will farmers seize the moment or stall?

Summary:

The CAFTA-DR trade deal, finalized after nearly 20 years, boosted U.S. dairy exports from $40 million pre-2006 to $441 million by 2025, thanks to the complete removal of tariffs. This expansion has made Central America an essential market for American dairy, particularly in cheese, milk powders, and whey. However, exporters still face non-tariff challenges like high port fees in Nicaragua, approval delays in El Salvador, and competition from the EU and New Zealand. As U.S. dairy farmers adapt to these hurdles, they must invest in technology and forge co-op partnerships to stay competitive.

Key Takeaways:

U.S. dairy exports surged to $441 million following the full implementation of the CAFTA-DR trade deal.

Cheese exports dominate the CAFTA-DR dairy trade, leading with over half of the market share.

While tariffs have been eliminated, non-tariff barriers such as high port fees and lengthy approval processes remain challenges.

The CAFTA-DR region is now the third-largest market for U.S. dairy exports, emphasizing its significance.

Global competition is intensifying, with rival trade deals potentially impacting U.S. market share.

Dairy farmers must adapt strategies based on farm size to leverage export opportunities and remain competitive.

Future growth will depend on expanding into new markets, adopting technology, and strategic policy negotiations.

Small and medium farms may rely on cooperative agreements to achieve export success.

The demand for advanced technology, such as blockchain for product tracking, may pose financial challenges for smaller farms.

Six CAFTA-DR countries fueled a 1,117% surge in U.S. dairy exports since 2006. Central America now ranks as the third-largest market for American milk, cheese, and whey

At midnight on January 1, 2025, U.S. dairy tariffs vanished across Central America under the fully implemented CAFTA-DR trade deal, capping a 19-year phaseout that supercharged exports from $40 million pre-2006 to $441 million today. Cheese shipments charge $238 million annually, with milk powders ($120M) and whey ($35M) rounding out a market critical to absorbing America’s growing milk surplus.

Category

2006 Exports

2023 Exports

2025 Projections

Growth (%)

Cheese

$34m

$238m

$264m

+595%

Milk powders

$3.2m

$120m

$135m

+3,650%

Whey products

$2.8m

$35m

$48m

+1,150%

Total

$40m

$441m

$527m

+1,217%

How CAFTA-DR Reshaped Dairy Trade

The agreement, negotiated by the National Milk Producers Federation (NMPF) and the U.S. Dairy Export Council (USDEC), began lowering tariffs in 2006. This slow-but-steady approach allowed farmers to adapt:

Cheese exports surged by 595%, representing 54% of the CAFTA-DR dairy trade.

Milk powders supported Guatemala’s $2.1B bakery industry growth.

Whey became a staple in 72% of regional animal feed mixes

Jaime Castaneda from NMPF highlighted that the patience invested in CAFTA-DR led to a tenfold increase in dairy exports over the 19 years. “But tariffs alone aren’t magic—trust took 7,000 farm visits and 19 years of problem-solving.”

The payoff? Central America now ranks as the third-largest U.S. dairy export market, trailing only Mexico and Canada.

Zero Tariffs ≠ Smooth Sailing

Country

Tariff Status

Key Non-Tariff Barrier

Avg. Delay/Cost

El Salvador

0% since 2025

Facility registrations

72 days

Nicaragua

0% since 2025

Port inspection fees

+$42k/shipment

Guatemala

0% since 2025

Labeling disputes

21% rejections

Dominican Republic

0% since 2025

Quota administration

+$15k/compliance

However, despite the achievement, exporters now face new challenges:

Nicaragua’s 33% port fees increased shipment costs by $42,000 per shipment in 2024.

El Salvador’s 72-day approvals: Delays tripled since 2023

Canada’s retaliatory 25% border tax puts $578 million in annual U.S. dairy sales at risk due to Canada’s retaliatory 25% border tax.

“My ice cream melted in Costa Rican customs last month—$12,000 gone because paperwork ‘wasn’t shiny enough,’” says Idaho farmer Kaitlyn Voeller. USDEC’s Sarah Schmidt notes progress: “We’ve resolved 14 non-tariff barriers since July 2024, but it’s Whac-A-Mole. For every successful resolution, three new issues arise, creating a continuous cycle of challenges.”

Global Rivals Race Ahead

While U.S. farmers celebrate CAFTA-DR, competitors gain ground:

Competitor

Recent Trade Deal

U.S. Dairy Risk

EU

Japan FTA (87k-ton cheese quota)

\$1.3B loss by 2030

New Zealand

Vietnam 45% tariff cuts

Whey share ↓ 8%

Canada

Retaliatory 25% border tax

\$578M at risk

Sarah Schmidt warns that the EU is making agreements while the U.S. is still in discussions. “If we delay discussions with Kenya and Indonesia, we risk losing a generation of farms.”

Farm Size Dictates Strategy

With U.S. milk production hitting 227.2B pounds in 2025 (USDA), survival hinges on exports:

Small farms (50–500 cows): Pool through co-ops like Dairy Farmers of America’s new Guatemala contracts

Mid-sized (500–5K cows): Target niches like Honduras’ 340% rise in artisanal cheese demand

Large operations (5K+ cows): Invest in dedicated plants, e.g., Lupino Farms’ $220M Texas facility

Ben Strauss, an Ohio dairy farmer with 180 cows, credits his farm’s survival to the strategic decision to sell 40% of his milk to CAFTA-bound gouda cheese products. “But for $3,000 per heifer, margins vanish faster than morning fog for dairy farmers.”

Navigating the Future: The Crucial Decade for Milk’s Survival

The USDA aims to target new middle-class consumers in Asia by 2030 and capture a share of the 2.1 billion potential customers in CAFTA-adjacent markets like Colombia.

Tech Upgrades: Costa Rican buyers now require Blockchain shelf-life tracking systems, which cost $15K each. However, 83% of small farms cannot afford this upgrade.

Policy conflicts are escalating, with battles over Canada’s border tax, the EU’s Philippines dairy pact, and ongoing negotiations with Kenya and Indonesia.

Castaneda emphasizes that while CAFTA-DR marks a significant milestone, the crucial task now is to shape the future to prevent being overtaken by competitors proactively.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Explore the record-breaking highs of U.S. dairy exports in September and what this means for the future. How will global price surges impact farmers?

Summary:

In September, U.S. dairy exports experienced significant growth, reaching $707 million, marking a six-month peak, as global demand for American dairy products surged. Cheese exports set a record with 86.3 million pounds, mainly due to a 19.4% increase in shipments to Mexico compared to the previous year. While nonfat dry milk and whey exports increased year-on-year, they fell short of the exceptional volumes in 2022. These trends have stabilized domestic markets by preventing oversupply and have driven up prices. Simultaneously, global dairy markets have strengthened, as evidenced by rising prices at the Global Dairy Trade auction, with most products, except lactose, hitting two-year highs. The U.S.’s position as a foremost dairy exporter reinforces its role as a critical player in the international dairy sector, distinguished by its products’ high quality and safety standards.

Key Takeaways:

U.S. dairy exports reached a six-month high in terms of value in September, driven by robust cheese shipments and significant sales growth to Mexico.

Despite some declines compared to previous years, nonfat dry milk and whey exports remain strong, helping manage U.S. inventory levels.

Market dynamics show increasing prices across dairy products at the Global Dairy Trade auction, except for lactose, which declined.

The boost in U.S. dairy exports positions the country as a competitive player in the global dairy market amid evolving trade patterns.

Industry stakeholders face opportunities and challenges as they adapt their strategies to leverage export growth while managing market volatility.

U.S. dairy exports, demonstrating remarkable resilience and strategic acumen, surged to an impressive $707 million in September, reaching the peak of the past six months. This remarkable milestone highlights the growing global demand for American dairy products and instills confidence in the strategic capabilities of the U.S. dairy industry. As the industry revels in this resurgence, a significant question emerges: What implications does this hold for the future trajectory of the U.S. dairy sector? As demand trends shift and markets continue to evolve, the impacts of this growth are extensive, encouraging a thorough examination of the long-term sustainability and adaptability of this upward trend. The record-setting statistics from September mark a crucial juncture for U.S. dairy, with extensive consequences that could redefine its global standing.

Riding the Wave: The U.S. Emerges as a Dairy Superpower

The global dairy market has been experiencing a significant uptrend characterized by rising prices and burgeoning demand. Several factors drive this escalation, including increased consumer desire for dairy products in emerging markets and the growing appetite for protein-rich foods. According to recent statistics, worldwide dairy consumption has surged, reflecting a 20% increase over the past five years, with a notable demand spike in Asia and Africa.

The USDA’s Global Agricultural Trade Systems (GATS) is pivotal in this dynamic landscape. GATS meticulously gathers data on U.S. agricultural exports, providing critical insights into trade volumes, destination markets, and price movements. This information is essential for stakeholders across the dairy supply chain, allowing them to make informed decisions and anticipate market shifts. GATS essentially serves as a compass, guiding the industry through the ever-changing currents of the global dairy market.

The United States stands out as a formidable force in the global dairy arena, not only as a leading producer but also as a significant exporter. U.S. dairy products, renowned for their quality and safety standards, are in high demand globally, with exports expanding by more than 31% over the last decade. American dairy exports have been instrumental in meeting the growing global demand, making the U.S. an indispensable player in the international dairy sector and a benchmark for other countries engaged in dairy trade.

From Farm to Fiesta: U.S. Cheese Exports to Mexico Surge

In September, the cheese export narrative took a robust turn. The United States marked a paradigm shift by dispatching an impressive 86.3 million pounds of cheese beyond its borders. This figure represents the highest September cheese export volume on record and a 6.8% increase compared to last year. This data, sourced from the USDA’s Global Agricultural Trade Systems, underscores the growing international demand for U.S. cheese, further propelled by strategic market maneuvers such as targeted marketing campaigns and competitive pricing strategies.

Mexico, a perennial powerhouse in U.S. cheese exports, continues to play a pivotal role, reflecting its burgeoning appetite for American dairy products. Shipments to this key partner surged by an extraordinary 19.4% from the preceding year, cementing Mexico’s status as a crucial market destination and showcasing its economic symbiosis with the U.S. dairy sector.

This uptick is manifold, effectively offsetting the deceleration in cheese sales to certain Asian territories. It exemplifies dynamic adaptability within export strategies focused on bolstering relationships with proximate neighbors. Such strategic targeting cultivates closer economic ties and supports broader trade balances amidst fluctuating global conditions.

Nonfat Dry Milk and Whey: Balancing Act for Market Equilibrium

The export performance of nonfat dry milk (NDM) and whey is multifaceted, presenting both hurdles and growth opportunities. Notably, exports of NDM surged by 15.6% compared to the previous year, breaking a new September record for shipments to Mexico. However, it is critical to highlight that current figures still lag behind those achieved in 2022 and 2021, reflecting a tapering off from earlier highs.

In contrast, whey product exports also exhibited a robust performance, marking a 15.3% increase over the September 2023 numbers. Despite this growth, these figures fell short of the unparalleled pace set in 2022. The deviation showcases the ebb and flow characteristic of international demand and market dynamics, directly affecting inventory management practices. However, the robust performance of whey product exports reassures the audience about the industry’s adaptability to market dynamics.

These export volumes have weighed heavily on U.S. milk powder and whey powder stockpiles. The industry successfully regulates inventory levels by maintaining a healthy outflow of products, preventing oversaturation. This capacity to keep stocks aligned with market demand is pivotal, as it directly influences commodity prices.

Ultimately, the positive uptick in exports helps rein in inventories, reflecting an agile response to fluctuating market conditions. As the CME spot market prices for whey and NDM edge close to their 2024 peaks, it becomes evident that balancing production output with export activities is critical to sustaining favorable price thresholds.

Market Momentum: Riding the Bullish Waves in Dairy Trading

The upward trajectory in market responses has been a significant focal point for analysts and dairy farmers alike. In September, the CME spot market and the Global Dairy Trade (GDT) auction reflected bullish tendencies. Whey and nonfat dry milk (NDM) prices rallied within a whisker of their 2024 highs on the CME spot market, showcasing remarkable resilience. This price strengthening indicates robust market demand, buoyed by substantial export volumes that have helped keep domestic inventories from ballooning.

The GDT auction provided another bullish narrative worldwide, with the GDT Index reaching its highest point since July 2022. This resurgence was echoed in the elevated prices for a spectrum of products, including anhydrous milkfat, which achieved its highest price since it started trading on the platform in January 2018. The price rallies for cheddar, whole milk powder, skim milk powder, and buttermilk powder underscore a market willing to pay a premium for these commodities, reflecting improved purchasing power and demand from international buyers.

For U.S. dairy farmers, these price trends are more than just a welcome reprieve; they signify a potential shift in economic conditions that could spur increased profitability. Farmers adept in adjusting their production strategies in response to such market signals stand to benefit significantly. As the market volatility continues to unfold, the ability of U.S. producers to adapt to these trends will be crucial in sustaining their competitive edge in the global dairy landscape.

The Bottom Line

U.S. dairy exports reached new heights in September, with cheese, nonfat dry milk, and whey setting notable records. This upward trajectory boosts the nation’s standing in global markets. It signifies a robust demand that could influence supply chains and inventory management. The impressive figures point to strong international relationships, particularly with Mexico, which are testaments to the expanding markets for American dairy products. As dairy farmers and industry stakeholders, pondering these. developments and their long-term implications is essential. How might these changes shape your business strategies? Could this surge affect domestic prices or inventory levels down the line? These trends are more than just statistics; they are indicators of potential shifts in the market that warrant close attention and strategic response. The challenge lies in adapting to and capitalizing on these dynamic market conditions to foster sustained growth and competitiveness in the global arena.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Unpack August’s dairy boom and export shifts. How is bird flu in California shaping the market? Find critical insights for dairy pros.

Summary:

August’s dairy market showcased opportunities and challenges as U.S. milk equivalent exports rose by 2.6%, driven by significant increases in cheese and butter production at 1.7% and 14.5%, respectively. However, Nonfat Dry Milk (NFDM) production dipped 10.1%, reflecting potential shifts in the market. The surge in Milk Protein Concentrate (MPC) with a remarkable 77.8% rise opens doors for diversified applications, yet complexities arise with abundant cream supplies affecting butter prices. Meanwhile, the troubling bird flu outbreak in California looms over future production, as the need to decipher spot and future pricing becomes essential for farmers to remain competitive amidst this evolving landscape.

Key Takeaways:

August showcased significant growth in dairy product production, notably with cheese and butter seeing double-digit increases.

Global cheese export trends provide U.S. dairy farmers a lucrative opportunity despite recent price declines.

The dairy market experienced divergent prices, with spot prices lowering and futures prices remaining robust.

California’s dairy sector is grappling with a bird flu outbreak, potentially impacting state and national milk production figures.

Abundant cream supply has led to a notable rise in butter production, yet prices continue to fall due to surplus.

NFDM production dropped, while domestic consumption declined steeply, contributing to inventory buildup.

Dairy professionals must remain vigilant and adapt to capitalize on emerging market opportunities and challenges.

In August, the dairy industry saw a surprising jump in production, going against what everyone expected and breaking new ground. Cheese production increased by 1.7%, and butter had a massive jump of 14.5%. This rise, though, comes with its challenges. The bird flu situation in California is getting serious, with almost 100 confirmed cases on dairy farms. It raises a fundamental question: how are these dynamics influencing the dairy market?

August was a testament to the dairy industry’s resilience, showcasing both growth and challenges. Understanding and adapting to the dairy scene has become more critical than ever amid these dynamics. Balancing production peaks with potential threats is a complex situation that could redefine the industry. Let’s explore how these forces reshape the market and the inspiring opportunities they present for everyone involved.

August’s Production Surge: A Double-Edged Sword for Dairy Farmers

August’s dairy production numbers show a surprising jump that has grabbed the interest of many folks in the industry. Essential dairy items like cheese, butter, yogurt, and ice cream saw some solid gains compared to what was expected. Cheese production increased by 1.7%, and butter took off with a 14.5% jump. So, yogurt and ice cream got a nice little boost, with yogurt up 7.7% and ice cream up 5.9%. This spike raises questions about what’s behind it. It could be due to increased demand, improved production techniques, other factors, and what it means for dairy farmers and others involved.

Milk Protein Concentrate (MPC) Takes the Spotlight

One of the top performers, Milk Protein Concentrate, saw a fantastic growth of 77.8%. This boom could open up more chances for producers to get creative and expand their use of MPC in different food products. More and more people are looking for high-protein ingredients, which is excellent news for MPC to thrive.

On the flip side, nonfat dry milk dropped by 10.1%, which could mean some changes in the market are happening. This downturn and the drop in domestic disappearance we’ve seen lately bring some challenges we must tackle. Farmers who depend on NFDM must roll with the punches and might want to check out different production methods or mix things up with what they offer.

What Does This Mean for the Industry?

These production changes present a myriad of opportunities and challenges for dairy farmers. The increased output in popular products like MPC could pave the way for better markets. Simultaneously, other sectors, especially NFDM, might require some innovative changes. The industry’s ability to adapt, manage higher production levels while meeting market demands, and monitor inventory is essential. By doing so, farmers and companies can maintain stability and foster growth in this ever-evolving field.

Riding the Global Cheese Wave: An Unmissable Opportunity for U.S. Dairy Farmers

In August, U.S. milk equivalent exports increased by 2.6%. This rise isn’t just a number; it shows how much the world wants U.S. dairy products. But the real standout was cheese, with exports jumping 15.2% compared to last year. These numbers are a nudge for U.S. dairy farmers to seize new opportunities.

What’s up with the massive demand for U.S. cheese overseas? You can find the answer in the incredible variety and quality of products that American dairy farmers are famous for. As people worldwide get bolder with their food choices, the fantastic range of U.S. cheese hits the mark and goes beyond what they want. Mix that with solid trade deals and lower tariffs; you have an excellent recipe for boosting international sales.

These trends are shaking things up in the U.S. dairy market. Better export numbers show that American farmers are more than aren’t depending on local sales, which can be a bit hit or miss. They have a presence in international markets where people might shop differently. Dairy farmers can mix things up with their income and protect themselves from the ups and downs of the local market.

The robust cheese export numbers should catalyze dairy farmers to diversify and expand their product offerings. It’s crucial to continue riding this global demand wave by exploring new markets and niche segments. Farmers can also enhance their herd management and milk production processes. Establishing robust supply chains that can cater to local and global needs is paramount. This is an exciting time for the dairy industry, with ample opportunities for growth and innovation.

The U.S. dairy market has challenges, but tapping into the current global demand boom could shake things up for the industry. Dairy farmers must develop innovative strategies to stay competitive in this growing export market.

It is diverging Paths: Spot and Futures Prices in the Dairy Market.

Understanding how spot and futures prices relate is critical in any market, especially in the dairy world. Spot prices tell you the prices for cheese and butter, while futures contracts lock in prices for future delivery. The newest information shows that spot prices stay the same or go down while futures prices hold steady or climb up. That’s a pretty cool situation! What’s up with this?

Could this difference mean a shift in how the market vibes are on the way? When futures prices are above spot prices, it often suggests that the market feels optimistic about future price increases. The market crowd thinks there might be less supply or some more robust demand on the horizon. Since spot prices aren’t showing this now, we should consider what’s happening.

So, regarding cheese and butter, are we dealing with a short-term thing or something that could hang around for a bit? For now, the cream supply and solid butter production might hold off any price hikes. For now, the futures market could be watching some changes that aren’t obvious in the current supply situation. These tips can help dairy farmers deal with price fluctuations more smoothly.

Checking out these price changes can help producers and market analysts understand and prepare for what’s ahead in the market. History has shown that these differences can open up opportunities for strategy or highlight risks we should keep an eye on. It’s an excellent opportunity—maybe a brief—to consider adjusting business strategies to take advantage of these shifting market vibes.

California’s Dairy Industry Faces a New Threat: Bird Flu Outbreak Raises Concerns

California’s dairy scene is dealing with a surprise issue: almost 100 confirmed cases of bird flu. This outbreak could shake up the state’s milk production in October, potentially decreasing the broader U.S. dairy market. California has always been a big player in milk production, significantly impacting the national total. But right now, the health crisis will likely change things up, causing U.S. milk production to dip by about 0.5% after a steady year-on-year run.

How the market reacts to this situation shows a pretty exciting gap. Even though there’s a drop in output coming up, it seems like no one is really worried or freaking out about it right now. Traders and industry folks don’t seem too worried because there’s already a surplus of cream and butter that could soften the short-term supply hit. But if the bird flu situation worsens, the long-term effects could be severe. Dairy farmers and industry pros must stay sharp and plan competent to handle the current disruptions and prepare for future impacts. Is this a chance or a challenge to rethink how we do production?

Cheese Market: Navigating a Tempest or Skimming Uncharted Waters?

The U.S. and EU cheese market is experiencing some significant changes this season. In August, U.S. cheese production exceeded expectations, showing a tremendous increase of 1.7% compared to last year. Production went up simultaneously, and exports shot up by 15.2% compared to last year. Cheese consumption at home held firm, with a decent disappearance rate of 1.1%.

But as we roll into September and October, the market is figuring things out in some unknown territory. Cheese prices in the U.S. and EU have been decreasing lately, thanks to changes in production and maybe shifts in what consumers want or competition from abroad. Last week, CME blocks got a bit of support, but overall, the market vibe is feeling bearish. What’s this all about for dairy farmers and those involved? Are we seeing the start of a longer-term price stabilization or just a short-term bump?

With solid August numbers giving us some breathing room, the next step is to get a grip on how things are changing for the rest of the year. It’ll be interesting to see if these trends stick around or change, depending on how people spend their money, chances for exports, and any unexpected shifts in the global market. If you’re in the industry, keeping up with all the changes is critical to making the most of your investments and handling risks like a pro.

Butter Market Conundrum: The Surprising Effects of a Cream Surplus

Is it any surprise that with so much cream around, U.S. butter production jumped by a whopping 14.5% in August compared to last year? This spike has changed the butter market scene. So, why aren’t butter prices going up, too? The answer is all about the basic economic principles of supply and demand, which are at odds.

With all this cream around, butter production is kicking into high gear as processors take advantage of the extra raw materials. But here’s the thing: the market’s already packed with butter. There’s a lot of extra supply out there, pushing prices down since producers have to sell their stuff at lower prices to get people to buy more. This situation is different from how markets usually react when there’s a significant boost in production.

Butter prices have been slow lately and, in some cases, even dropping, which is strange given that production is doing so well. Too many products in the market can water down their value, making the perks of high production levels less noticeable. This situation has many folks in the industry feeling puzzled as they try to figure things out in these tricky times. Having less of something doesn’t just lead to lower prices; it also creates issues with storage and logistics, making things even trickier.

We must also consider what this cream oversupply might mean for the long haul. It might look like a bump in the road, but it could lead to better pricing and help U.S. butter reach more markets worldwide. This trend highlights how important it is to plan and think strategically when dealing with production booms, turning today’s challenges into opportunities for the future. Are producers ready to take on the challenge? We’ll have to wait and see.

Navigating the NFDM Labyrinth: Balancing Production and Demand in a Complex Market

The NFDM market has been on a pretty interesting path, with prices staying steady despite a noticeable production drop of 10.7% compared to last year in August. Usually, when production drops, prices go up, but that’s not happening here, which shows things are a bit complicated in the market. One big thing to note is the drop in domestic disappearance in July and August, with declines of 80.1% and 37.7%, respectively. The drop in demand caused a buildup of inventory, which helped keep the market stable and avoided price increases.

So, what’s the deal with the powder market going forward? The current inventory is building up, so the supply should handle sudden demand jumps pretty well, keeping prices steady. Producers should reconsider their game plan if the domestic disappearance trend continues. Does this mean we see a push for more exports or a rethink of production to match what people want right now? We’ll have to wait and see. Dairy farmers and industry folks need to keep an eye on these changes because even a tiny shift in how the market feels can mean significant changes in their game plan.

The Bottom Line

Looking at what’s happening, we see that the dairy industry is at a turning point with impressive production boosts and big market challenges. The significant increase in cheese and butter production is excellent. Still, it also shows how tricky it can be to handle supply when demand changes—something every savvy dairy farmer gets. California’s bird flu situation and the ups and downs of unpredictable futures markets make things even more complicated in an already shaky situation.

Even with the hurdles, it’s clear that there’s an excellent chance for clever positioning right now. The gap between spot and futures pricing could hint that market players should look past the short-term challenges and consider what’s coming down the road. With the world craving more cheese, U.S. dairy farmers can take advantage of excellent international chances if they play their cards right.

So, it’s not just about getting through the tough stuff but also making the most of what’s happening right now. Is the butter surplus pushing us to develop fresh ideas to boost demand, or will we keep dealing with this extra stock without a plan? Finding the right mix of uncertainty and opportunity makes us rethink our game plans, keeping the dairy industry strong and looking ahead.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

How did USMCA boost U.S. dairy exports to Mexico by 59%? What does this mean for dairy farmers? Discover key insights and future opportunities.

Summary:

Have you ever wondered why Mexico has become such a crucial market for U.S. dairy producers? The answer lies in trade policies, particularly the United States-Mexico-Canada Agreement (USMCA). From 2014 to 2023, U.S. dairy exports to Mexico surged by an impressive 59%, thanks to strategic agreements like the USMCA, which replaced NAFTA. These policies develop new markets and increase demand for U.S. dairy products. Mexico’s proximity and favorable trade conditions have significantly contributed to this growth. However, the future outlook faces challenges due to the recent depreciation of the Mexican peso. This could reduce Mexico’s buying power and make U.S. dairy products more costly and less competitive.

Key Takeaways:

USMCA replaced NAFTA, significantly increasing U.S. dairy exports to Mexico.

From 2014 to 2023, U.S. dairy exports to Mexico surged by 59%.