Discover why U.S. fluid milk sales and cheese exports are surging despite a decline in production. How is this shift impacting the dairy market? Read more to find out.

Unexpectedly for the U.S. dairy business, fluid milk sales and cheese exports are rising even as milk output steadily declines. Adjusting for the leap year, fluid milk sales jumped by about 100 million pounds in the first four months of the year over the previous year. Cheese exports concurrently reach a record 8.7 percent of total output from February to April, the most ever for any three months or even one month. These unexpected patterns can be attributed to a variety of factors, including changing consumer preferences, global market dynamics, and technological advancements in dairy production. The wider consequences for the dairy industry, such as shifts in market share and potential economic impacts, are also investigated in this paper.

Despite the challenges of falling milk output, the U.S. dairy industry is demonstrating remarkable resilience with the rise in fluid milk and cheese exports. This unexpected trend holds promising implications for producers and consumers, instilling a sense of hope and optimism in the industry.

As the dairy industry negotiates these changes, fast rises in cheese prices have significantly raised the Class III price, underlining the market’s reaction. Examine the elements underlying these patterns and the possible long-term effects on domestic consumption and foreign commerce.

A Surprising Rebound: Fluid Milk Sales Surge Amid Shifting Consumer Preferences

| Month | Fluid Milk Sales (million pounds) |

|---|---|

| May 2022 | 4,500 |

| June 2022 | 4,450 |

| July 2022 | 4,470 |

| August 2022 | 4,480 |

| September 2022 | 4,460 |

| October 2022 | 4,490 |

| November 2022 | 4,500 |

| December 2022 | 4,510 |

| January 2023 | 4,520 |

| February 2023 | 4,530 |

| March 2023 | 4,550 |

| April 2023 | 4,600 |

With a roughly 100 million pound gain and a 0.7 percent leap year-adjusted surge, this unprecedented spike in fluid milk sales highlights a dramatic change in consumer behavior. Rising health awareness and the availability of dairy substitutes have usually been causing fluid milk intake to drop. But this increase might point to changing market dynamics or fresh enthusiasm for milk’s nutritious value.

| Dairy Product | Change in Consumption (Percentage) |

|---|---|

| Fluid Milk | +0.7% |

| American Cheese | -1.2% |

| Yogurt | +2.4% |

| Non-American Cheeses | +1.5% |

| Butter | -0.8% |

| Ice Cream | -1.0% |

The changes in domestic dairy consumption create a complicated scene for the American dairy business. While butter, ice cream, and American cheese consumption have dropped, fluid milk sales may have increased due to changing habits or knowledge of nutritional value. Growing worries about health, animal welfare, and environmental damage define this downturn.

On the other hand, demand for yogurt and non-American cheeses has surged. Yogurt’s probiotics and health advantages attract health-conscious customers. Non-American cheeses benefit from their superior quality, appeal to refined tastes, and clean-label tendencies.

This difference draws attention to shifting customer demands and the need for dairy farmers to adjust. Stakeholders trying to seize market possibilities in a dynamic economic environment must first understand these trends.

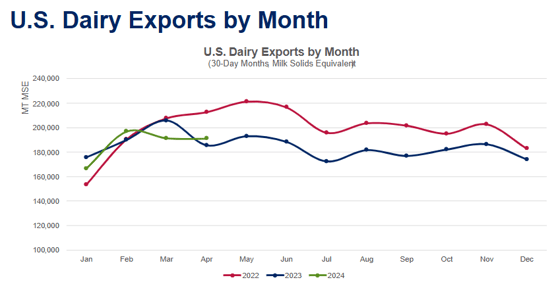

American Cheese Exports Set New Record: A Game-Changer for the U.S. Dairy Market

The U.S. dairy market has witnessed a notable shift in export trends over the past year, which can largely be attributed to evolving global demand and intensified trade relations. Cheese exports, in particular, have set new benchmarks, reflecting both opportunities and challenges in the international marketplace. Below is a detailed table outlining the changes in cheese exports over the past year:

| Month | Cheese Exports (Million Pounds) | Year-over-Year Change (%) |

|---|---|---|

| January 2023 | 60 | 5.2% |

| February 2023 | 58 | 4.9% |

| March 2023 | 65 | 7.5% |

| April 2023 | 70 | 9.8% |

| May 2023 | 72 | 11.1% |

| June 2023 | 68 | 8.3% |

| July 2023 | 75 | 10.7% |

| August 2023 | 80 | 12.5% |

| September 2023 | 78 | 11.4% |

| October 2023 | 82 | 13.2% |

| November 2023 | 85 | 14.1% |

| December 2023 | 88 | 15.3% |

- Key Export Markets: Japan, Mexico, South Korea

- Emerging Opportunities: Southeast Asia, Middle East

- Challenges: Trade policies, supply chain disruptions

With 8.7% of total output moving abroad, the United States saw an increase in cheese exports between February and April. This fantastic number emphasizes the increasing worldwide market for American cheese. The milestone points to a change in the strategic emphasis of the U.S. dairy sector as producers show their capacity to meet and surpass the demands of foreign markets, therefore implying a future in which exports will be more important economically.

Milk Production Plunge: Unpacking the Multifaceted Decline in the U.S. Dairy Sector

In examining the shifting landscape of the U.S. dairy market, it’s imperative to consider the nuances in milk productiontrends that have unfolded over the past year. These trends highlight the recent downturn in production and provide a lens through which we can better understand the broader dynamics at play.

| Month | Milk Production (billion pounds) | % Change (Year-over-Year) |

|---|---|---|

| April 2022 | 18.1 | -0.4% |

| March 2022 | 17.9 | -0.5% |

| February 2022 | 16.0 | -0.6% |

| January 2022 | 17.5 | -0.7% |

| December 2021 | 17.7 | -0.8% |

| November 2021 | 16.8 | -0.9% |

| October 2021 | 16.9 | -1.0% |

| September 2021 | 16.0 | -1.1% |

| August 2021 | 18.0 | -1.2% |

| July 2021 | 18.2 | -1.3% |

| June 2021 | 17.8 | -1.4% |

| May 2021 | 18.1 | -1.5% |

Adjusting for the leap year, the continuous reduction in U.S. milk production—0.4 percent in April—has lasted 10 months. For the dairy sector, this development begs serious questions.

Many factors are driving this slump. First, dairy farmers have been under pressure from changing consumer tastes that influence demand. Growing demand for plant-based and dairy substitutes is reshaping the market share controlled initially by cow’s milk. Furthermore, changing customer behavior and ethical and environmental issues influence production levels.

The low cow count raises yet another critical question. Modern and conventional dairy states have battled dwindling or stagnating cow numbers. Growth patterns in cow counts have slowed dramatically in contemporary dairy states since 2008; some years even show reductions. This has lowered milk availability, together with a volatile macroeconomic backdrop.

Dairy farmers also face many operational difficulties, such as supply chain interruptions, personnel shortages, and the need for fresh technologies. These problems tax the industry’s ability to sustain past output levels even as manufacturers seek creative ideas.

Dealing with these entwined problems would help to stop the drop in output and guarantee the resilience and sustainability of the American dairy market against changing consumer tastes and financial uncertainty.

Turbulent Trends: How Consumer Values and Supply Chain Challenges Propelled Cheese Prices Skyward

The past year has witnessed significant fluctuations in the dairy market, with particular emphasis on cheese prices, which have experienced rapid increases. This section breaks down the price trends over the past year to provide a comprehensive understanding of the market dynamics.

| Month | Class III Milk Price (per cwt) | Cheese Price (per lb) | Butter Price (per lb) |

|---|---|---|---|

| May 2022 | $25.21 | $2.29 | $2.68 |

| June 2022 | $24.33 | $2.21 | $2.65 |

| July 2022 | $22.52 | $2.00 | $2.61 |

| August 2022 | $20.10 | $1.95 | $2.50 |

| September 2022 | $21.86 | $2.10 | $2.55 |

| October 2022 | $21.15 | $2.03 | $2.53 |

| November 2022 | $20.72 | $2.01 | $2.60 |

| December 2022 | $21.55 | $2.05 | $2.58 |

| January 2023 | $20.25 | $1.98 | $2.55 |

| February 2023 | $18.67 | $1.85 | $2.50 |

| March 2023 | $19.97 | $1.92 | $2.55 |

| April 2023 | $20.25 | $2.01 | $2.52 |

| May 2023 | $23.30 | $2.35 | $2.70 |

Many complex elements reflecting more significant market dynamics drove the increase in cheese prices throughout May. The dairy sector has seen a paradigm change as consumer tastes center on health, environmental issues, and animal welfare more and more. These higher ethical standards call for more rigorous behavior, which drives manufacturing costs. A turbulent macroeconomic climate, ongoing supply chain interruptions, and workforce difficulties further limit cheese supplies. Cheese prices skyrocketed as demand for premium dairy products continued locally and abroad, and supply ran low.

The May Class III price, which rose by $3.05/cwt from the previous month, was substantially affected by this price increase. Primarily representing the worth of milk used for cheese manufacture, the Class III price is a benchmark for the larger dairy market. This sharp rise emphasizes how sensitive commodity prices are to quick changes in specific sectors, stressing the cheese market’s importance in the national dairy economy. Dairy farmers must balance growing expenses with remaining profitable while meeting changing customer expectations.

The Bottom Line

The surprising surge in fluid milk sales and record-breaking cheese exports within the changing terrain of the U.S. dairy industry contrasts sharply with the continuous drop in milk output. The 0.7 percent rise in milk sales points to a change in consumer behavior, motivated by a fresh enthusiasm for classic dairy products. On the other hand, American cheese’s demand internationally has skyrocketed; 8.7% of output is exported, suggesting great worldwide demand and a possible new income source for home producers.

Adjusting for the leap year, the consistently declining milk output—now at ten straight months of year-over-year decline—showcases important production sector issues probably related to feed price volatility and long-term changes in dairy farming techniques. Reflecting these supply restrictions and shifting market dynamics, the substantial rise in cheese prices fuels a significant increase in the May Class III price.

These entwined tendencies point to both possibilities and challenges for American dairy farmers, implying a tricky balancing act between satisfying home demand, profiting from foreign markets, and negotiating manufacturing efficiency and cost control.

Key Takeaways:

In an evolving landscape marked by shifting consumer preferences and unprecedented export achievements, the U.S. dairy market has experienced stark contrasts in its fluid milk sales, cheese exports, and milk production. Below are the key takeaways from these recent developments:

- U.S. fluid milk sales rose by nearly 100 million pounds, or 0.7% on a leap year-adjusted basis, during the first four months of this year.

- While domestic consumption of most major dairy products decreased, yogurt and non-American types of cheese saw increased domestic demand.

- A record 8.7% of total U.S. cheese production was exported between February and April, marking an all-time high for this period.

- April 2023 witnessed a 0.4% decline in U.S. milk production compared to April 2022, continuing a ten-month trend of lower year-on-year production figures.

- Cheese prices surged in May, driving the May Class III price up by $3.05 per hundredweight from the previous month.

Summary:

The U.S. dairy industry has experienced a significant increase in fluid milk sales and cheese exports, despite declining milk output. Fluid milk sales jumped by about 100 million pounds in the first four months of the year, while cheese exports reached a record 8.7% of total output from February to April. This unexpected trend can be attributed to changing consumer preferences, global market dynamics, and technological advancements in dairy production. The wider consequences for the dairy industry include shifts in market share and potential economic impacts. Despite these challenges, the U.S. dairy industry is demonstrating remarkable resilience with the rise in fluid milk and cheese exports. This trend holds promising implications for producers and consumers, instilling a sense of hope and optimism in the industry. However, as the dairy industry negotiates these changes, fast rises in cheese prices have significantly raised the Class III price, underlining the market’s reaction. American cheese exports set a new record for the U.S. dairy market, reflecting both opportunities and challenges in the international marketplace. Addressing these entwined problems would help prevent the drop in output and guarantee the resilience and sustainability of the American dairy market against changing consumer tastes and financial uncertainty.

Learn More:

For further insights into this evolving landscape, consider exploring the following articles: