Check out November’s mixed results in U.S. dairy exports. Why did cheese exports rise while milk powder and whey exports drop? Find out the reasons and upcoming challenges.

Summary:

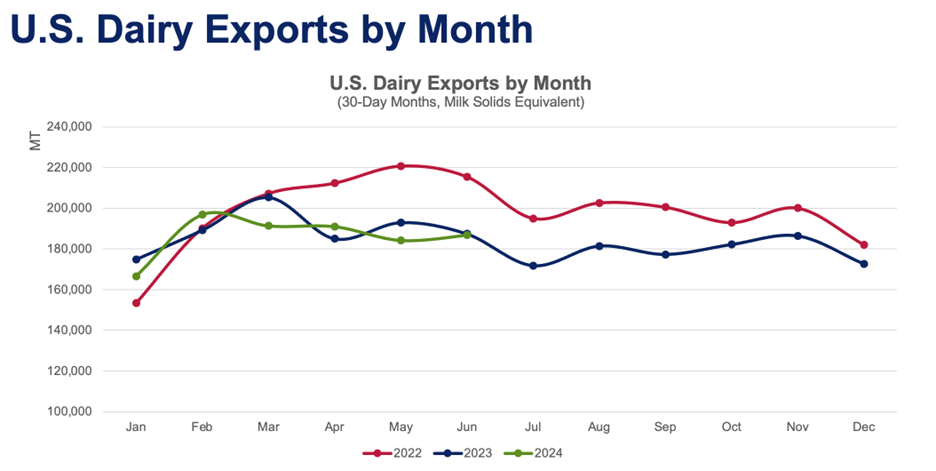

November saw ups and downs for U.S. dairy exports. Cheese was a big hit, especially with Mexico, setting a record with 87 million pounds shipped. That’s a 2.4% increase from the previous year and 17.5% higher overall in 2023. But it wasn’t all rosy. Milk powder and whey products struggled, with exports dropping 20% and 11.4% from the prior year, respectively, due to less production and stiffer competition. This mixed bag of results makes folks in the dairy industry think hard about their plans for 2025, especially with the changing global trade scenes. Mexico’s appetite for U.S. cheese rose 30%, helping to cut into the U.S. cheese stockpile and boosting prices. They also bought a lot more cream—hitting a seven-year high—and the interest in nonfat dry milk dropped by 8.2%. This could mean Mexican consumers change what they buy, affecting how U.S. exporters plan their next moves. There’s a bright spot for those in cream and cheese, but the known dip in milk powder warns to rethink strategies.

Key Takeaways:

- U.S. cheese exports to Mexico rose significantly, contributing positively to overall export numbers.

- Cheese export growth helped reduce U.S. cheese inventory levels, potentially driving up prices.

- Despite strong cheese exports, milk powder exports declined, marking the potential lowest annual volume since 2019.

- Whey exports also fell due to supply constraints, impacting total dairy export volumes.

- International competition and potential tariffs in 2025 present challenges for U.S. dairy exports.

- Mexico’s import dynamics illustrate shifting consumer preferences impacting U.S. dairy exports.

- Global trade complexities offer hurdles and opportunities for adaptation in the U.S. dairy sector.

In November, U.S. cheese exports reached a historic high, shipping 87 million pounds abroad, primarily driven by Mexican demand. This remarkable achievement, however, was not mirrored across all dairy products. Nonfat dry milk exports saw an 8.2% decline from the previous year, and exports of whey products, vital for many producers, dipped by 11.4%. These mixed results highlight the ebb and flow of U.S. dairy exports, leaving stakeholders pondering strategies for 2025. Can the robust demand for cheese compensate for declines in other exports? How will these challenges reshape the industry? These are the questions American dairy farmers grapple with in this evolving landscape.

| Category | November 2024 Volume (lbs) | YoY Change (%) |

|---|---|---|

| Cheese Exports | 87 million | +2.4% |

| Nonfat Dry Milk | 70 million | -8.2% |

| Whey Exports | – | -11.4% |

| Cream Exports to Mexico | 3.9 million | N/A |

U.S. Dairy Exports: Growth in Cheese Amidst Powder Struggles

The U.S. dairy exports in November had highs and lows, reflecting a mixed picture in the world market. Cheese exports were strong, setting month-over-month records with a 2.4% increase from the previous year due mainly to Mexican demand, which rose 30%. Mexico has become a key player, importing large amounts of cheese and cream. However, not all segments did as well. Nonfat dry milk exports dropped by 19.7% compared to November 2023. This decline in milk powder and whey products points to current supply challenges.

The importance of trade is evident. Dairy exports boost the U.S. economy by supporting the agricultural sector and helping dairy farmers nationwide. The dairy industry is crucial for rural economies and international trade relations.

The mixed results present both a warning and an opportunity. While cheese exports are promising, the lag in milk powder and whey calls for strategic changes. This situation encourages U.S. dairy farmers and stakeholders to tackle global trade challenges and improve their competitive edge in a world where trade deals are crucial. The resilience and adaptability of U.S. dairy farmers in the face of these challenges are genuinely inspiring, offering hope for the industry’s future.

Pepper Jack on the Move: How Mexico’s Cheese Cravings Shape U.S. Exports

The rise in U.S. cheese exports highlights the strong demand from Mexico, reshaping the export scene. Eighty-seven million pounds of cheese went south in November, setting a new monthly record. This demand pushed monthly exports up by 2.4% from November 2023. So, what’s fueling this cheese boom? Mexico’s craving for U.S. cheese, driven by reasonable prices and excellent quality, surged 30% by the end of November compared to 2023. This trade has helped cut down U.S. cheese stocks and supported higher cheese prices at home. Fewer stocks mean prices go up, benefiting producers. This is a clear win for U.S. dairymen, as Mexico’s appetite for cheese plays a big part in export success. The rising demand for cheese offers an excellent chance for ongoing growth in the industry. For U.S. cheese makers, it’s another big success.

Mexico’s Evolving Taste: How Shifts in U.S. Cream and Milk Powder Imports Reflect Consumer Trends

Mexico’s significant demand for U.S. dairy products highlights its pivotal role in U.S. exports. Recently, Mexico imported 1.8 million liters of U.S. cream—a seven-year high in November. This surge in cream imports and a 30% rise in cheese demand suggests a growing market that U.S. sellers are ready to tap into. However, the 8.2% drop in nonfat dry milk shipments, totaling 70 million pounds, could indicate changes in Mexican consumers’ diet preferences or budgets, prompting U.S. exporters to shift their strategies.

For U.S. dairy exporters, these import patterns present both hurdles and opportunities. There’s potential for a more substantial presence in cream and cheese markets, which promise steady revenue. Meanwhile, the decline in nonfat dry milk exports cautions against reconsidering product lines and pricing. For Mexican markets, diverse imports show changing consumer tastes, urging local businesses to innovate. Responding to these shifts is key to boosting U.S. market share in Mexico and Mexicans’ choices.

Struggling with Shifting Sands: Navigating Challenges in U.S. Milk Powder Exports

In recent months, the U.S. dairy industry has struggled to keep up with milk powder exports, which play a vital role in the dairy trade. A significant reason for this drop is the reduced production of milk powder in the U.S. Poor weather affecting feed quality and quantity has led to lower milk production. Additionally, rising costs and labor shortages have further cut production capacity.

Another challenge is increased competition from other dairy producers, like New Zealand and the European Union. These areas have expanded their dairy production, benefiting from favorable trade deals and lower costs. They have captured key markets that once depended on U.S. dairy exports, shrinking American producers’ market share.

The impact of declining milk powder exports could have lasting effects on the U.S. dairy industry. With falling export volumes, producers may struggle to manage inventories, leading to financial difficulties when selling excess supplies in the domestic market. A smaller global presence could hurt the U.S. in future trade talks, diminishing its influence in international dairy standards and policies.

Also, ongoing export declines might force dairy farmers and manufacturers to diversify products or innovate to find new markets. While this offers growth opportunities, it requires investment and involves risks that need careful consideration. These trends underscore the urgent need for strategic changes in the U.S. dairy industry to maintain and enhance its global competitiveness.

Whey-ing the Consequences: Constricted Supply Chains Challenge U.S. Dairy

Whey product exports declined in November mainly due to tight supplies. They dropped 11.4% from last year, primarily due to a 10.1% decrease in whey protein concentrate shipments. These lower exports highlight limited whey product availability, which is linked to production issues. The drop in whey, alongside weak milk powder exports, brought overall U.S. dairy export volumes to their lowest since last January. This dip dims the strong cheese exports, raising questions about whether current strategies can handle supply hiccups.

The impact on the U.S. dairy industry is significant, affecting farmers and producers. While cheese led the way, weak whey exports raised red flags. The industry should consider whether production and supply chains are ready to adapt to changing global demands. Acknowledging the challenges faced by the U.S. dairy industry helps stakeholders feel understood and empathized with, fostering a sense of unity in addressing these issues.

Braving the Shifting Tides: Navigating the Complexities of Global Dairy Trade

The global trade landscape for dairy products is changing quickly, influenced by many factors that can alter export patterns. U.S. exporters face tough competition as other countries, such as the European Union, New Zealand, and Australia, secure new trade deals. These agreements often offer benefits like lower tariffs, making their products more appealing in the market.

Meanwhile, U.S. trade policies, including threats of tariffs on key partners, add uncertainty to the industry. Tariffs can protect local industries but might also lead to retaliatory actions, making U.S. dairy products more expensive abroad.

Future U.S. dairy exports may face challenges. Markets might shrink because of cheaper imports from countries with better trade deals. Tariffs could worsen this issue, reducing demand for U.S. products and pressuring those in the industry to find new markets or adapt their strategies.

As these changes continue, the U.S. dairy sector must stay informed about trade agreements, geopolitical shifts, and tariff discussions. Engaging with policymakers to support favorable trade policies could help U.S. dairy products compete globally. Flexibility and innovative strategies will be key in determining the future path of U.S. dairy exports.

The Global Ripple Effect: How World Economics Shape U.S. Dairy Exports

Now and then, world economics, not just the product, affects U.S. dairy exports. So, let’s explore these broader forces. First, let’s talk numbers—no, not just cheese wheels. Currency exchange rates can seriously change how affordable U.S. dairy products are worldwide. A stronger dollar makes American goods, like cheese and milk powder, more expensive for other countries to import. It’s like watching exchange students paying more for a burger at your local diner just because currency shifts.

Global economic conditions matter, too. Slowdowns in key markets mean customers and businesses tighten budgets, likely choosing local dairy instead. Conversely, buyers are more willing to spend on imports, like U.S. dairy, when economies thrive.

Trade policies are also crucial. Deals and tariffs can open or close doors, sometimes favoring competitors like the EU or New Zealand. The situation shifts when big players make profitable trade deals, making things challenging for U.S. exporters. Domestic policies might add to the mix, with potential tariffs adding uncertainty.

If you’re a dairy farmer in the U.S., these global shifts feel personal, correct? International ups and downs often decide whether your cheese goes abroad or stays here. These challenges can be tricky but offer opportunities to evolve and create solutions.

The Bottom Line

The ups and downs of U.S. dairy exports remind us how important it is to stay informed. Dairy isn’t just about numbers; it mixes economies, tastes, and global connections. Each market change tells a story, and every statistic reflects trends that affect farms’ and creameries’ decisions. By understanding these dynamics, dairy farmers and industry players can face challenges and find new opportunities. Let’s keep the conversation going! Whether you’re a dairy farmer with stories to share or just curious, there’s always more to explore.

Learn more:

- U.S. Dairy Exports Surge in April: Record Cheese Shipments and Whey Boost

- U.S. Dairy Exports Drop 5% in May as Cheese Continues to Shine Amid a Challenging Year

- Is 2024 Shaping Up a Disappointing Year for Dairy Exports and Milk Yields?

Join the Revolution!

Join the Revolution!

Join the Revolution!

Join the Revolution!Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.