Global cheese exports hit a record-breaking milestone, surpassing 1 billion pounds for the first time. As demand soars and new markets emerge, dairy farmers face unprecedented opportunities and challenges. Discover how shifting consumer trends, environmental concerns, and market dynamics reshape the industry’s future.

Summary:

The global cheese market is experiencing unprecedented growth, with U.S. exports surpassing 1 billion pounds in 2024. This surge reflects a worldwide trend, with Mexico leading as a key importer. While presenting significant opportunities for dairy farmers, the boom also brings challenges. Volatile prices, environmental concerns, and changing consumer preferences reshape the industry. New production facilities worth $4 billion are coming online to meet demand, but farmers must navigate sustainability issues and adapt to evolving market dynamics. Balancing increased production with environmental stewardship remains a critical challenge as the industry expands. Despite these hurdles, the overall outlook for the cheese market remains positive, offering potential for growth and innovation in the dairy sector.

Key Takeaways:

U.S. cheese exports achieved a historic high, exceeding 1.028 billion pounds by November 2024, signaling strong global demand.

Competitive pricing, despite fluctuations, offers opportunities for U.S. cheese in the international market. Cheddar Block prices are $1.8900 per pound.

Investments in cheese production are rising, with $4 billion directed towards new plants in the U.S., expanding global production capabilities.

Consumer trends favor premium, sustainable, and convenient cheese options, offering fertile ground for product diversification.

Sustainable practices are becoming essential due to environmental pressures, requiring investment in inefficient systems and renewable energy.

The global cheese market is experiencing unprecedented growth, with U.S. exports surpassing 1 billion pounds for the first time in history in November 2024. This milestone signals robust international demand for cheese products and presents significant opportunities for dairy farmers worldwide. Understanding these trends is paramount for farmers aiming to capitalize on expanding markets and ensure long-term sustainability in 2025.

Record-Breaking Exports and Market Dynamics

In November 2024, U.S. cheese exports reached an impressive 1.028 billion pounds, marking a historic high. However, this surge in exports is not isolated to the U.S. market. The global cheese trade has consistently grown, with the total world cheese trade from all major suppliers increasing for 10 consecutive months through July 2024.

Mexico remains a powerhouse consumer, accounting for 38% of all U.S. cheese exports. Mexico’s increasing demand for cheese products is evident from a 32% year-over-year purchase rise. Predictions suggest that Mexican cheese imports could reach 18,000 tons by 2025, indicating a probable continuation of this trend.

“The boom in cheese demand is exciting, but we’re also concerned about the long-term sustainability of our operations. Balancing production increases with environmental stewardship is our biggest challenge in the future.” – A dairy farmer from Wisconsin.

Global Market Trends and Pricing

Region

Average Cheese Price (per pound) in 2024

Year-over-Year Change

The U.S.

$1.89

+10-12%

EU

€4.49 ($5.39)

+32.7%

Australia

AUD 6.20 ($4.65)

+23%

2025, the cheese market will be characterized by strong demand and competitive pricing. In 2024, the average price for 40-pound blocks of Cheddar cheese in the U.S. was $1.82 per pound, making American cheese attractive in the global market. However, prices have been volatile in 2025, indicating market fluctuations.

The price of Cheddar Blocks rose to $1.8900 per pound on January 28, 2025.

By early 2025, cheese prices had increased by 10-12% compared to the previous year.These price fluctuations reflect a complex interplay of supply and demand factors, including increased production capacity and growing consumer interest.

Production Capacity and Industry Investment

Significant investments are being made in cheese production capacity within the dairy industry. Several new cheese plants are coming online through 2027, representing a $4 billion investment in the U.S. alone. This expansion is not limited to the U.S.; the EU is also forecasting increased cheese production:

EU27 cheese production is projected to increase to 10.8 million metric tons in 2025, a 0.6% rise from 2024, despite a decrease in milk availability. Rising demand is driving the increase in global production capacity, which presents both opportunities and challenges for dairy farmers.

Consumer Trends Shaping the Market

Country

Projected Avg Cheese Consumption per Capita 2024 (kg/year)

Premiumization: Consumers are increasingly willing to pay more for high-quality, innovative, artisanal cheeses.

Health and Sustainability: There’s a growing demand for natural, organic, and clean-label cheeses.

Convenience: Pre-sliced and ready-to-eat formats are gaining popularity.

Global Flavors: Interest in international and specialty cheeses drives a “global cheese renaissance.”

These trends present new opportunities for dairy farmers to diversify their product offerings and access premium markets.

Environmental Considerations

The expansion of cheese production raises critical environmental concerns. Dairy farming contributes significantly to greenhouse gas emissions, mainly methane. With the industry’s growth, there is a growing pressure to implement sustainable practices:

Implementing efficient systems for manure management

Exploring alternative feed options to reduce methane emissions

Investing in renewable energy sources on farms

Rod Hogan, an innovation leader at Sargento, notes, “It’s common to see ‘Under Construction’ signs in many of our facilities, emphasizing the industry’s rapid growth. ” This highlights the industry’s rapid growth and the need for sustainable expansion.

Challenges and Farmer Perspectives

Despite the generally positive outlook for the cheese market, dairy farmers encounter several challenges:

Price Volatility: Fluctuating cheese prices can make financial planning difficult for farmers.

Environmental Regulations: Stricter environmental policies may require additional investments in sustainable practices.

Competition: Increased global production could lead to market saturation and price pressures.

An anonymous Wisconsin dairy farmer expressed concerns about operations’ long-term sustainability, highlighting the challenge of balancing production growth with environmental stewardship.

The Bottom Line

The growth of the global cheese market offers significant opportunities for dairy farmers but also presents challenges that must be addressed. As we move into 2025, farmers will need to navigate price volatility, environmental concerns, and changing consumer preferences. To succeed in this dynamic environment, dairy farmers should stay updated on market trends, prioritize investments in sustainable practices, and be responsive to consumer demands.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Discover key trends as CME cheese and butter prices rise. Understand how U.S. production growth could affect your dairy strategies.

Summary:

The latest CME market report showcases a rally in Class III and cheese prices, driven by renewed buyer aggression and U.S. production gains, with the USDA’s October report detailing a 1% increase in cheese output and a 3.1% rise in butter production year-over-year. Market complexities like technical resistance levels and fluctuating whey prices prompt producers to reassess strategies, especially as U.S. cheese prices lag behind those in New Zealand and the EU. Dairy markets show bullish momentum, with block cheese at $1.70 per pound and butter prices increasing, paving the way for potential profit expansions. However, strategic hedging is necessary to balance pricing strategies and profit margins amid rising cheese prices, strong market dynamics, and holiday season-driven demand for butter now priced at $2.54.

Key Takeaways:

Class III cheese and block cheese markets experience steady gains, indicating bullish sentiment despite seasonal demand fluctuations.

The U.S. continues to produce more cheese and butter than previous years, driving domestic market prices up while still remaining competitive globally.

Butter futures have risen significantly, with current market conditions suggesting a sustained demand around the $2.50 per pound mark.

The USDA’s October Dairy Products report highlights an increase in overall cheese and butter output compared to last year, despite some sector-specific declines.

Whey prices impact Class III contracts significantly, necessitating careful monitoring by producers, especially as the first quarter of 2025 approaches.

The NFDM market faces challenges as global demand appears to stabilize, emphasizing the need for strategic positioning in the current pricing environment.

U.S. dairy pricing remains more favorable compared to New Zealand and EU counterparts, providing competitive leverage in international markets.

Dairy markets are currently experiencing a bullish momentum, with cheese and butter prices on the rise. This unexpected pre-holiday market rally has certainly stirred things up. Block cheese has advanced to $1.70 per pound, and butter prices have also seen a significant increase. This rally presents both risks and opportunities, affecting pricing strategies, profit margins, supply chain decisions, and market forecasts. As these forces behind the numbers capture industry attention, it’s crucial to start strategizing for 2025, ensuring preparedness and proactivity in the face of these market dynamics.

Product

Current Price (per pound)

Weekly Change

Comparison Index

Block Cheese

$1.70

+3 cents

+7 cents week-to-date

Barrel Cheese

$1.6675

+1.75 cents

+7 cents week-to-date

Spot Butter

$2.5400

+1.75 cents

+5.5 cents from last week’s low

NDM

$1.3700

-0.50 cent

Sideways price action

Riding the Wave: CME Cheese and Butter Prices Climb Amid U.S. Production Surge

The recent pricing trends at CME exhibit a clear upward trajectory in cheese and butter, driven primarily by U.S. production dynamics and international market comparisons. Cheese markets are showing a continuous rally, with block cheese advancing to $1.70 per pound and barrel cheese climbing to $1.6675 per pound. Notably, both categories reflect a 7-cent increase this week, contributing to bullish sentiments in futures markets. This movement is juxtaposed against U.S. cheese prices, which are significantly lower than New Zealand and EU figures, priced at $2.13 and $2.28 per pound, respectively.

Butter pricing follows a similar ascent, now reaching $2.54 per pound, influenced by a robust production backdrop. The USDA’s recent dairy report indicates a 3.1% annual increase in butter output, revealing a comparative advantage over European and New Zealand markets, where butter prices are notably higher. These variances highlight the U.S.’s relative positioning in global markets, as the domestic increase in production aligns strategically with international price disparities, offering competitive advantages that bolster market resilience.

The Cheese Surge: Navigating Gains and Strategic Opportunities

The cheese market is currently undergoing significant shifts, particularly within the block and barrel cheese categories. Block cheese has climbed to $1.70 per pound, witnessing a 3-cent rise through multiple trades, while barrel cheese saw a 1.75-cent increase, settling at $1.6675. These seemingly modest increments have amplified the momentum in the futures market, particularly impacting Class III futures. Over recent sessions, January Class III futures have surged by $1.00/cwt, reflecting investor optimism fueled by these incremental gains. This surge in the cheese market presents a promising outlook, potentially leading to better returns for dairy producers.

These market shifts bear significant implications for dairy producers. The rising price of cheese indicates stronger market dynamics and potentially better returns. However, these gains bring with them the need for strategic hedging as there’s a delicate balance to maintain. For producers under-covered for the first quarter of 2025, the current rise offers an opportunity to secure favorable pricing floors. It’s crucial, however, to remain vigilant about whey prices, as any decline in whey, which plays a critical role in Class III pricing, could erode these advantages. Each penny drop in whey could translate to a 6-cent impact on Class III prices, underscoring the importance of monitoring these interconnected market components. While the present trajectory offers positive signals, producers must navigate these waters with a keen eye on volatility and fundamentals.

Butter Bounces Back: Market Dynamics and Growth Deceleration

The recent upswing in butter market prices reflects a nuanced amalgam of supply and demand dynamics. With spot butter rising 1.75 cents to close at $2.54, it is noteworthy that the butter futures have also shown appreciable gains, advancing 0.50 to 2.00 cents across contracts through July 2025. This upward movement suggests a robust reaction following some expected technical oversold conditions seen before Thanksgiving.

The driving force behind this price increase is the persistent demand during the holiday season, combined with a steady supply of cream, facilitating ample butter production. What’s compelling is the notable deceleration in butter output growth, shifting from a staggering 15.1% increase in August to a more moderate rise of 3.1% compared to last year. Despite this slowdown, the current production levels are sufficient to meet prevailing demand while maintaining price stability.

The second half of 2025 appears promising for a balanced trade, given the confidence in production capacity supported by available cream supplies. Yet, the market also benefits from targeted consumer interest around the $2.50 price point, adding a layer of demand elasticity that continues to underpin market strength.

USDA’s October Dairy Report: Navigating Production Shifts and Market Resilience

The USDA’s October Dairy Products report provides a comprehensive overview of the trends in cheese and butter production in the United States, revealing pivotal insights into market dynamics. Notably, total cheese production witnessed an incremental rise, reaching 1.226 billion pounds, marking a 1.0% increase compared to last year. This modest increase suggests a more robust output relative to the stagnation observed in September, signaling potential stabilization in demand despite underlying challenges.

Conversely, the production of U.S. Cheddar remains tepid, showing a 3.1% decline against the figures recorded in October 2023. This downturn in Cheddar production underscores a potential shift in consumer preference or market demand, challenging producers to optimize production levels without incurring surplus. Such strategic restraint aligns with maintaining balanced inventories amidst fluctuating demand.

In the butter sector, production expanded by 3.1%, totaling 167.5 million pounds. While this growth is a marked deceleration from the double-digit increases noted in August and September, it reflects the market’s ability to calibrate outputs effectively to avoid oversupply, thus supporting price levels. The deceleration suggests some caution among producers, yet the upward trend in butter production reinforces its consistent demand in the domestic market.

These production insights, grounded in the October Dairy Products report, highlight shifts in year-over-year production patterns and underline dairy producers’ nuanced adjustments to navigate current market demands and price signals. As the industry maneuvers through these fluctuations, strategic production decisions will be crucial in shaping future market resilience and pricing stability.

Strategic Advantage: U.S. Dairy’s Path to Global Leadership through Competitive Pricing

The current price of cheese in the U.S. is $1.67 per pound, significantly lower than in international markets such as New Zealand and the EU, where cheese fetches $2.13 and $2.28 per pound, respectively. This disparity presents a strategic opportunity for U.S. producers to expand their export reach. The more competitive pricing could make U.S. cheese an attractive option for international buyers seeking cost-effective imports.

Similarly, U.S. butter, priced at $2.52 per pound, is also competitively positioned in the global market compared to New Zealand’s $2.96 per pound and Europe’s far higher price of $3.80 per pound. Such pricing differentials present promising export prospects for U.S. butter producers, who can capitalize on these price advantages to penetrate foreign markets.

Lower U.S. price levels relative to international markets are beneficial for exports and could also influence domestic market dynamics. This pricing competitive edge may stimulate increased production as domestic suppliers aim to meet potential heightened demand at home and abroad. It may also lead to adjusting domestic supply chains to better cater to the export-oriented production strategy. For U.S. dairy farmers, aligning production with global pricing trends is crucial for sustaining competitiveness and leveraging new markets.

Whey and NFDM: Essential Components in Dairy Market Dynamics

The intricate web of the global dairy market is significantly influenced by the roles of whey and nonfat dry milk (NFDM). Recently, whey has shown resilience, maintaining its position above 70 cents despite a minor slip, a testament to its critical role in the Class III pricing structure. Given that every penny moves in whey correlates to a six-cent adjustment in Class III milk prices, its stability underpins the robustness seen in this sector despite broader market fluctuations.

On the production front, the October Dairy Products report indicated a notable downturn in dry whey production—down 12.3% from the previous year. This significant reduction in output, paired with a 33.1% decline in stocks from 2023, has likely contributed to the observed stability in whey pricing, supporting its market relevance even as other products like cheese advance [USDA Dairy Products report].

Conversely, NFDM’s market performance appears more precarious. Despite weaker production figures and growing inventories, NFDM prices remain around $1.40. Recently, the spot market saw NFDM edge down half a cent as supply pockets permeated the CME market, testing this price ceiling. Analysts suggest that the lack of aggressive global demand, amplified by global price competitiveness, may prevent NFDM from capitalizing on current price points [source].

The implications of these trends are profound for the dairy market. The robust price amidst constrained production indicates strong demand fundamentals for whey, offering producers a buffer against volatility in other dairy categories. Meanwhile, NFDM’s plateau suggests potential opportunities or risks contingent upon global demand or supply dynamics shifts. Therefore, Market participants must navigate these evolving landscapes strategically, balancing production with emerging market cues to effectively leverage these critical commodities.

Technical Terrain: Navigating Peaks and Valleys in Cheese and Butter Markets

The current landscape in the CME cheese and butter markets reveals key technical considerations that can significantly impact future price movements and trading strategies. Notably, the current market is facing resistance levels just above prevailing prices. This suggests that while a continued upward trajectory is possible, traders should exercise caution as price action could encounter difficulty sustaining momentum beyond these thresholds.

Technical patterns indicate the potential for a weekly reversal in nearby contracts, a development usually perceived as bullish despite lackluster current demand narratives. Such a reversal suggests that underlying strength supports current price rebounds. It could attract more buying interest if confirmed, further fueling upward price momentum.

Traders should watch these resistance points closely. Breaking through them could initiate a new price leg higher, indicating robust demand or supply dynamics that could alter market perceptions. On the other hand, failure to surpass these resistance levels could result in consolidation phases where prices stabilize, allowing for strategic reassessment.

Regarding trading strategies, prudent market participants might consider short-term positions to capitalize on these potential reversals and longer-term hedges to mitigate risk should prices reverse again or encounter sustained pressure. This multifaceted approach allows for flexibility, ensuring traders can efficiently adapt to evolving market dynamics.

The Bottom Line

The current landscape of the CME market indicates the rebound of cheese and butter prices and the intricate web of production dynamics influencing these shifts. As the U.S. continues to ramp up cheese and butter production, the pivotal role of strategic pricing relative to international markets cannot be overstated. Navigating the complexities of whey and NFDM further underscores the need for dairy professionals to remain vigilant and proactive in their market strategies.

Dairy farmers and industry stakeholders must monitor emerging market trends and assess how these could affect their operations. What strategies can you adopt to leverage this knowledge and navigate fluctuating market conditions? Can you implement innovative approaches to stay ahead of the competition despite shifting demand and production levels?

Engage with these questions, adapt your business strategies, and harness the insights from ongoing market reports. Staying informed with reports like these will ensure you are well-equipped to make informed decisions, enhancing your resilience and competitive edge in this dynamic industry.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Learn how beef-on-dairy is shaping beef production. Will it significantly impact the market? Find out in our expert analysis.

Summary: The beef-on-dairy trend is reshaping the dairy industry but making only a modest dent in U.S. beef production. In 2022, beef-on-dairy cattle comprised 7% of cattle slaughter, or 2.6 million head, with projections suggesting this could rise to 15% by 2026. However, this doesn’t increase the total cattle count but changes the composition, as more beef-on-dairy cattle replace traditional dairy-fed ones. While dairy farmers adopt beef semen to boost calf value, the overall beef production impact remains negligible. The adoption of beef-on-dairy has surged, reaching 7.9 million units in 2023 due to cost differences and breeding technology advances. Customer perception, market demand, and credibility from sources like branded beef programs will be critical to this trend’s longevity.

Beef-on-dairy is growing, making up 7% of cattle slaughter in 2022, potentially rising to 15% by 2026.

The trend doesn’t increase the total cattle count but changes the composition, replacing traditional dairy-fed cattle with beef-on-dairy cattle.

Dairy farmers are adopting beef semen to enhance calf value, yet the overall impact on beef production is minimal.

Adoption of beef-on-dairy reached 7.9 million units in 2023, driven by cost differences and breeding technology advances.

Consumer perception, market demand, and credibility from branded beef programs will be crucial for the trend’s sustainability

Are you wondering about the latest buzz over beef-on-dairy? It’s no wonder that this movement is gaining traction. Dairy producers increasingly use beef semen in their herds to generate calves more suited for meat production. Understanding this trend is vital for dairy farmers and industry experts, as it directly affects calf value and beef output quality, potentially changing market dynamics. This crossbreeding approach uses existing dairy resources to increase profitability, has consequences for beef quality and production standards, and may impact market supply and demand for beef and dairy products. By delving into this concept, you’ll learn how it’s gaining traction, what it means for the overall beef production market, and why its impact may be less significant than some believe, giving you a better understanding of how this trend may shape the future of both the dairy and beef industries.

Why Beef-On-Dairy Is Gaining Ground: Key Figures and Future Projections

Beef-on-dairy adoption has expanded significantly, with Lauber et al. (2023) reporting that it climbed from 18% or 738 thousand head in 2019 to 26% or 1.12 million head by 2021. In 2023, the National Association of Animal Breeders reported that beef semen sales to the dairy sector reached 7.9 million units, accounting for 31% of overall semen sales to dairy farmers, which included sexed, conventional, and beef semen sales (NAAB, 2023).

Several variables are influencing this tendency. One advantage of utilizing beef semen in dairy cows is that the cost difference is minor. As a dairy farmer, you can look forward to the potential boost in calf value since crossbred cattle command higher market prices. Furthermore, advances in breeding technology and genetics make this an attractive alternative for many people, offering a promising future for the industry.

Experts expect beef on dairy will account for 15% of cow slaughter by 2026. Given the dairy industry’s ongoing acceptance, these estimates seem reasonable. So, what is the takeaway? Beef-on-dairy is here to stay and will undoubtedly expand. Still, its total influence on beef output will be minimal. Does this seem like a good opportunity for your farm?

The Historical Roots: Why Beef-On-Dairy Became the Go-To Strategy

Understanding beef-on-dairy’s origins helps explain why this technique has gained popularity in recent years. Historically, dairy farms concentrated entirely on milk production, which resulted in lower-value male calves from dairy breeds. These calves did not match the quality criteria of typical beef cattle, resulting in reduced market pricing. However, the successful introduction of beef-on-dairy in the mid-twentieth century changed this narrative, paving the way for its popularity.

The idea of beef-on-dairy has been introduced previously. Its origins may be traced back to the practical farming practices of the mid-twentieth century when farmers experimented with crossbreeding dairy cows with beef bulls to boost the marketability of their herd’s progeny. However, the introduction of modern reproductive technologies such as artificial insemination and sexed sperm in the late twentieth and early twenty-first century completely transformed this practice.

By the early 2000s, technology had improved enough to enable dairy producers to selectively breed their herds with beef traits, resulting in much higher calf quality. The result? More healthy beef-like calves grew quicker and sold for more incredible prices.

The tipping moment occurred in 2015. As market dynamics changed and dairy producers were under pressure from changing milk prices, many sought other cash sources. Beef-on-dairy methods offered a feasible alternative, providing higher financial returns without significantly modifying current operating structures. This shift was a response to the changing economic landscape of the dairy industry, where traditional revenue streams were no longer as reliable.

The approach gained traction as statistics revealed the economic advantages of raising a calf that might flourish in the meat market. This was not simply theoretical; real-world data, such as market prices for crossbred calves compared to purebred dairy calves, indicated significant increases in calf value owing to improved genetics from beef breeds.

Knowing this history helps us understand why beef-on-dairy has been a popular approach for many dairy companies. It is not enough to follow a trend; one must also make educated selections based on decades of development and technical breakthroughs. This understanding can give us confidence in the future of the industry and its ability to meet market demands.

The Evolution of Cattle: Breaking Down Beef-On-Dairy’s Impact on Production

Let’s look at how beef-on-dairy impacts total beef output. While the quantity of calves born to dairy cows stays constant, the types of cattle that enter the beef production system vary. We are considering a trade-off between conventional-fed dairy cattle and beef-on-dairy cattle.

Thus, beef-on-dairy gradually increases the number of animals entering the beef production chain. It alters the makeup of the cattle population. Instead of typical dairy breeds in the beef industry, you will see more beef-dairy crossbreeds.

What exactly does this imply for you? When conventional-fed dairy cattle are substituted with beef-on-dairy cattle, the kind of beef produced changes. Beef-on-dairy cattle exhibit features of both their dairy and beef parents, which may improve meat quality and output. This transition is mostly a reallocation of the beef supply chain, not an addition.

What was the result? While the total amount of beef produced may only increase somewhat, quality and market dynamics may change significantly. This adjustment mirrors a more significant industry trend, suggesting a continuing development in successfully balancing dairy and beef production to satisfy market demands. This trend indicates a shift towards a more integrated approach to cattle farming, where both dairy and beef production are considered in tandem to optimize market outcomes.

The Quality Over Quantity Paradigm: Exploring Beef-On-Dairy’s Market Impact

While beef-on-dairy does not increase the overall quantity of cattle, it does influence the kind of beef available on the market. With more beef genes in the mix, the meat quality may vary. Beef-on-dairy calves may have different live weights, dressing percentages, and carcass weights than conventional dairy cattle.

Let’s break it down. Traditional-fed dairy cattle weigh around 1,400 pounds, with an average dressed weight of 800 pounds. What happens when we go from beef to dairy? According to experts, beef semen may have a slightly lower live weight but a more significant dressing percentage. This implies that, although the original live weight is lower, the dressed weight may be more critical owing to increased meat output.

Assuming a moderate 3% increase in dressed weight for beef-on-dairy cattle, carcass weights might rise by around 24 pounds. If all non-replacement dairy calves were beef-on-dairy in 2023, it would result in around 3.84 billion pounds of beef, compared to 3.73 billion from standard-fed dairy cattle. This 0.42% increase may seem minor, but it is significant in an industry where every pound matters.

Another factor to examine is the percentage of beef-on-dairy calves that are steers, which often have higher dressed weights. Suppose a more significant proportion of beef-on-dairy calves are steers. In that case, beef quality and volume might be more influenced. The difference may not be substantial, but these tiny changes assist in refining the beef supply entering the market.

So, even if beef-on-dairy may not significantly increase total beef output, it does promise to enhance the quality and potential economic worth of the beef produced. This shift has potential for both the dairy and cattle industries.

Economic Considerations for Dairy Farmers: The Game-Changing Potential of Beef-On-Dairy

Let’s look at the economic implications for dairy producers. Could beef-on-dairy make dairy heifers more valuable than beef cattle? There is a solid argument for this. With cattle genetics, dairy calves may be transformed into higher-value beef animals. This move might result in increased cash flow from the same number of calves.

Consider this: if dairy farmers can earn more per head for beef-on-dairy calves, that would be a game changer. It might pay additional operating expenses or perhaps support agricultural upgrades. More money in farmers’ purses equals more profitability for dairy enterprises.

Now, how does this affect dairy herd expansion? Higher calf prices may make dairy production more profitable. If revenues grow, some dairy producers may decide to enlarge their herds. More cows may produce more milk and beef-on-dairy calves, resulting in a growth cycle and increased profitability.

So, although beef-on-dairy may have little influence on overall beef output, the ramifications for dairy producers’ bottom lines are significantly more severe. That is why it is critical to monitor this development attentively. It has great potential to shape the future of dairy operations.

Consumer Perception and Market Demand: What’s the Buzz on Beef-On-Dairy?

How do customers perceive beef-on-dairy products, and is there increasing market demand? This issue is crucial to determining the trend’s long-term durability. It’s a topic worth discussing, particularly for those involved in the dairy and meat sectors.

Interestingly, customer opinion is typically influenced by several elements, including quality, taste, ethical issues, and pricing. According to recent research, most customers are unfamiliar with the intricacies of beef-on-dairy products. Still, they are willing to test them provided they fulfill quality and flavor standards. Credibility from reliable sources, such as branded beef programs, might have a substantial impact on these impressions.

In terms of commercial demand, millennials and Generation Z are especially interested in food that is produced sustainably and ethically. These populations are likelier to embrace beef-on-dairy crossbreeds because of their perceived efficiency and low environmental effects. This tendency is consistent with the increased demand for higher-quality beef without a substantial environmental cost.

Furthermore, the change to premium and branded beef programs would increase customer trust. Programs that guarantee beef-on-dairy products’ quality and ethical standards might help increase market acceptability and demand. By emphasizing quality over quantity, you may establish beef-on-dairy products as a premium option.

However, market expansion will not occur suddenly. A concentrated marketing and educational campaign will be required to increase consumer awareness. If successful, beef-on-dairy might become a regular in grocery store meat departments and on high-end restaurant menus.

Consumer opinions are cautiously optimistic, and there is growing market demand, especially among younger, ecologically concerned customers. For dairy producers, this implies that beef-on-dairy might be the game changer in balancing profitability and sustainability.

Marketing and Branding: Will Beef-On-Dairy Raise the Bar or Rock the Boat?

Regarding marketing and branding, the emergence of beef on dairy has the potential to change things. Imagine a future in which your beef products meet or surpass quality requirements. Beef-on-dairy calves often inherit the marbling of their beef sires, which may lead to better ratings such as USDA Choice or Prime. This immediately contributes to branded beef campaigns that depend on superior quality. Consider Certified Angus Beef and other specialist marks that attract high rates. With beef-on-dairy, these programs may see an increase in eligible cattle, broadening the product offering.

However, the issue remains: will these quality premiums stay stable or endure volatility? Because beef-on-dairy strives to combine the most significant aspects of both worlds—beef and dairy—most signals point to sustained pricing. Consumers are continuously prepared to pay for quality. As long as beef-on-dairy production meets high standards, premiums should remain stable. The versatility of branded programs may also help to mitigate any transitory implications. As long as these programs can include beef-on-dairy cattle without violating their demanding standards, the marketing of U.S. beef products is expected to improve rather than deteriorate.

The Bottom Line

In terms of marketing and branding, the emergence of beef on dairy has the potential to change things. Imagine a future in which your beef products meet or surpass quality requirements. Beef-on-dairy calves often inherit the marbling of their beef sires, which may lead to better ratings such as USDA Choice or Prime. This immediately contributes to branded beef campaigns that depend on superior quality. Consider Certified Angus Beef and other specialist marks that attract high rates. With beef-on-dairy, these programs may see an increase in eligible cattle, broadening the product offering.

However, the issue remains: will these quality premiums stay stable or experience volatility? Because beef-on-dairy strives to combine the most significant aspects of both worlds—beef and dairy—most signals point to sustained pricing. Consumers are continuously prepared to pay for quality. As long as beef-on-dairy production meets high standards, premiums should remain stable. The versatility of branded programs may also help to mitigate any transitory implications. As long as these programs can include beef-on-dairy cattle without violating their demanding standards, the marketing of U.S. beef products is expected to improve rather than deteriorate.

Are you eager to discover the benefits of integrating beef genetics into your dairy herd? “The Ultimate Dairy Breeders Guide to Beef on Dairy Integration” is your key to enhancing productivity and profitability. This guide is explicitly designed for progressive dairy breeders, from choosing the best beef breeds for dairy integration to advanced genetic selection tips. Get practical management practices to elevate your breeding program. Understand the use of proven beef sires, from selection to offspring performance. Gain actionable insights through expert advice and real-world case studies. Learn about marketing, financial planning, and market assessment to maximize profitability. Dive into the world of beef-on-dairy integration. Leverage the latest genetic tools and technologies to enhance your livestock quality. By the end of this guide, you’ll make informed decisions, boost farm efficiency, and effectively diversify your business. Embark on this journey with us and unlock the full potential of your dairy herd with beef-on-dairy integration. Get Started!

Explore how U.S. dairy exports are breaking records and surpassing last year’s numbers. How will these trends impact your dairy business? Learn more now.

Summary: This year has been nothing short of impressive for U.S. dairy exports. Despite fluctuations in some categories, overall growth remains strong, with cheese, whey, and nonfat dry milk all showing significant year-over-year increases. Cheese exports reached 88.7 million pounds in July, marking a new monthly high for the sixth time in 2024. Whey exports saw a 22.4% increase driven by Chinese demand, and nonfat dry milk exports hit a 14-month high, bolstered by record shipments to Mexico and an 80% surge to the Philippines. The sustained growth in these areas signals the U.S. dairy industry’s strength and presents promising opportunities for development and investment. However, the outlook for milk powder exports remains uncertain due to rising global prices and fluctuating U.S. output.

U.S. dairy exports vigorously grow across several categories, including cheese, whey, and nonfat dry milk.

Cheese exports hit 88.7 million pounds in July 2024, setting new monthly highs multiple times this year.

Whey exports increased by 22.4%, mainly due to rising demand from China.

Nonfat dry milk exports experienced a 14-month high with significant growth in markets like Mexico and the Philippines.

The U.S. dairy industry demonstrates robust potential for investment and expansion, offering promising opportunities for growth and development. This optimistic outlook is sure to inspire hope and confidence in the industry’s stakeholders.

Despite the overall positive trends, it’s important to note that milk powder export forecasts remain clouded by rising global prices and inconsistent U.S. production levels. This cautionary information is crucial for stakeholders to be aware of potential risks and make informed decisions.

By 2024, dairy exports aren’t just staying afloat—thriving. Month after month, U.S. dairy exports are making headlines and surpassing new benchmarks despite market ups and downs. This resilience underscores the strength of the U.S. dairy sector and should inspire confidence among all stakeholders. Diving into recent trends in dairy exports, mainly focusing on cheese, whey, and nonfat dry milk, we’ll explore why this matters. Understanding these patterns will help you make informed business decisions and possibly tap into emerging markets. In July, the U.S. shipped 88.7 million pounds of cheese abroad, marking a 9.4% increase from the previous year, according to USDA’s Global Agricultural Trade Systems. Keep reading to discover how this surge in dairy exports could impact your business and shape the global path for U.S. dairy products.

Export Category

July 2023

July 2024

% Change

Cheese (million lbs)

81.1

88.7

9.4%

Whey (million lbs)

33.2

40.6

22.4%

Nonfat Dry Milk (million lbs)

118.5

130.3

10%

Dairy Export Trends: 2024 Marks a Year of Remarkable Growth

With relation to dairy exports, 2024 looks to be a historic year. The most recent USDA Global Agricultural Trade Systems numbers show startling expansion in some dairy product categories.

July 2024 saw a significant milestone in U.S. dairy exports, with 88.7 million pounds of cheese being sent overseas, marking a 9.4% rise over the previous year. This increase, setting new monthly records for the sixth time this year, is a clear indicator of the growing demand for U.S. dairy products in the global market and a testament to the potential of the U.S. dairy industry.

In July, exports also saw a remarkable increase, rising by 22.4% yearly. The dramatic 34% increase in exports to China was a significant contributor to this spike, highlighting the increasing demand in Asian markets. This surge in exports to China clearly reflects the growing global demand for U.S. dairy products.

Notfat dry milk (NDM) also grew noticeably. In July, exports reached a 14-month high, surpassing last year’s level by 10%). Notably, sales to Mexico established a monthly record, up 20% from July 2023; exports to the Philippines jumped by an impressive 80%.

The vitality in these numbers emphasizes the worldwide performance of American dairy products, reflecting their quality. Cheese continues its strong performance, whey has mostly recovered, and NDM is still a necessary export good with great potential for expansion.

Sustained Growth in Cheese Exports: A Harbinger of Industry Strength

Regarding cheese exports in 2024, we see a challenging trend to overlook. Comparatively to July 2023, July alone witnessed a startling 88.7 million pounds of U.S. cheese transported overseas—a 9.4% rise. These statistics represent the strength and resiliency of the U.S. dairy industry, not simply data on a chart.

More impressive, perhaps, is that, particularly to vital markets south of the border, this represents the 14th straight month of record-breaking exports. This steady rise emphasizes the growing worldwide demand for U.S. cheese and the sensible tactics American producers have used to satisfy it. Setting a new high every month shows U.S. cheese’s volume, quality, and dependability, which consumers all across like.

These figures should also be a sign of hope for dairy farming specialists. The rising trend presents opportunities for development and investment, opening doors to new markets. The regularity of these record-breaking months also points to a strong basis and implies that this trend is sustainable. As you review your company strategy, take advantage of this increase in cheese exports. How do you see this? Please let others know about your observations and experiences. This potential for business expansion and investment should inspire optimism and motivate industry professionals to seize these opportunities.

U.S. Whey Exports: 2024 Highlighting a Robust Recovery

Considering the low 2023 standards, U.S. whey exports in 2024 have improved. The July exports jumped by 22.4% year over year. The 34% rise in exports to China is a notable engine of this expansion. This increase points to a noteworthy comeback and rising demand from one of the most significant worldwide marketplaces.

Export figures in 2021 and 2022 still fall short of those peak years. Still, the path of recovery shows a good change in 2024. Many elements probably help to explain this increase. First, whey is vital as high-quality protein products are increasingly sought after worldwide. Furthermore, the deliberate efforts of the U.S. dairy sector to improve traceability and quality have made U.S. whey a premium commodity.

This development has consequences beyond current sales numbers. First, it increases industrial confidence in reaching the Asian markets. Moreover, a steady increase in whey exports might open the path for more consistent pricing and help offset home supply changes. Professionals in dairy farming and related businesses should track these developments to modify their plans and seize the growing market prospects.

U.S. Nonfat Dry Milk Exports: A Rising Tide in the Global Market

A notable increase in U.S. nonfat dry milk (NDM) exports has created ripples in dairy worldwide. With a 10% increase above the previous year’s volumes, July was a 14-month high in NDM exports. This represents the increasing demand for U.S. dairy goods and strategic orientation in critical global markets, not just a statistic. This increasing demand for U.S. dairy products should make all industry professionals proud and accomplished.

Mexico is still great; July exports show an all-time high—a stunning 20% rise from the previous year. This significant increase emphasizes solid trade ties and the demand for superior American dairy products.

The Philippines is another vital market with an 80% increase in NDM imports from the United States. This significant increase can be attributed to the expanding taste for American dairy products in Southeast Asia, indicating a growing market for U.S. NDM in the region.

Examining more general patterns, the U.S. NDM has a more significant advantage worldwide. Rising global pricing and China’s increasing purchases at recent Global Dairy Trade (GDT) auctions point to a decrease in milk powder stockpiles among important exporters and importers. This offers a unique opportunity for American goods to close the gap more clearly.

Still, there are some obstacles just waiting here. Reduced U.S. milk powder production might have restrictions; another element to watch is the recent rise in spot NDM pricing. U.S. milk powder pricing for German skim milk powder (SMP) and GDT SMP stayed throughout last year about 10ȼ below benchmark levels. However, recent rises in spot NDM rates have closed this difference and heightened the competitiveness for new businesses.

Stakeholders have to be alert even if chances for ongoing development abound. Quickly using these benefits and negotiating challenges will depend on closely observing market dynamics and world developments.

Mixed Signals in U.S. Milk Powder Export Forecast

U.S. milk powder exports show mixed possibilities and difficulties in their projection. Rising worldwide pricing and higher Chinese buys at recent worldwide Dairy Trade (GDT) auctions point, on the one hand, to declining milk powder supplies of essential players. Under this situation, U.S. exporters could have fresh opportunities to fill the void.

The road ahead isn’t apparent, however. U.S. milk powder production has been somewhat poor, and the rise may hamper future sales in spot pricing for nonfat dry milk (NDM). U.S. milk powder costs were around 10ȼ below those for German skim milk powder (SMP) and GDT SMP for a good period—between September 2023 and July 2024—which gave it a competitive advantage. But that margin has dropped because of a late-summer surge in spot NDM prices.

This price rise compromises the competitive pricing edge, which makes it more difficult for American companies to get new contracts in a market growing competitive. Therefore, even if there are chances, especially with declining global stocks, U.S. exporters must carefully negotiate through these possible hazards. Strategic planning is thus essential for maximizing these trends without running into the related hazards.

The Bottom Line

When we consider the critical 2024 data points, it is evident that the U.S. dairy export industry is seeing excellent expansion in many different sectors. Cheese exports are setting records, indicating worldwide strong demand. However, whey sales to China and significant rises in nonfat dry milk exports to Mexico and the Philippines suggest other growing markets.

However, the milk powder export projection is still up for debate. While declining global stock and increasing prices should provide advantageous circumstances, changing U.S. production and competitive pressures could create difficulties.

What does all this mean for experts in the dairy business and farmers? There are chances for development and possible obstacles to negotiating in a developing export market. Leveraging these changes will depend primarily on being informed and flexible.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

EU dairy farmers boost milk production, but Dutch farmers see a decline. What does this mean for milk prices and your farm’s future?

Summary: As we delve into the first half of 2024, the landscape of milk production within the European Union reveals a complex mix of growth and decline. Overall, the EU’s dairy farmers have produced 1.0 percent more milk than last year’s last year, with Poland and France leading the charge. Conversely, countries like Ireland and the Netherlands are experiencing notable decreases in milk output, mirroring trends in other global dairy markets such as Argentina and Uruguay. Dutch farmers experienced a 3% drop in milk output in July, and the total milk volume is 1.6% lower over the first seven months of 2024, affecting milk pricing and market dynamics. Meanwhile, European milk prices surged 8 percent in July 2024, reflecting a volatile yet dynamic market environment. This multifaceted scenario prompts us to examine the intricacies behind these regional fluctuations and their broader implications for dairy farmers worldwide. Australia stands out in this global context, with a notable 3% increase in milk production, further influencing market dynamics.

EU dairy farmers produced 1.0% more milk in the first half of 2024 compared to 2023.

Poland and France significantly contributed to the increase in EU milk production.

Ireland and the Netherlands saw notable declines in milk output.

Global milk production trends show declines in Argentina, Uruguay, and the US, contrasting with growth in Australia.

Dutch milk output decreased by 3% in July and is 1.6% lower over the first seven months of 2024 than last year.

European milk prices rose 8% in July 2024, indicating a volatile market environment.

The fluctuations in milk production across regions have broader implications for global dairy markets and farmers.

Why are European dairy farmers increasing output while Dutch farmers are declining? In the first six months of 2024, EU dairy farmers produced 1% more milk than the previous year, with Poland and France leading the growth. In contrast, Dutch farmers face a 3% drop in milk output in July. Understanding these conflicting patterns is critical for anybody working in the dairy business since they directly influence milk pricing and overall market dynamics. This disparity may affect anything from pricing tactics to export potential. Staying ahead requires manufacturers to comprehend the larger market, locally and worldwide, and keep up with their production. So, what is driving these developments, and how can you remain competitive in such a turbulent market?

The Dynamic Landscape of EU Dairy Production: Comparing Growth and Decline

In the intricate fabric of European Union dairy output, the first half of 2024 has woven a story of moderate but significant rise. The collective efforts of dairy farmers throughout the EU have resulted in a 1% rise in milk production compared to last year, showcasing a region-wide resilience to enhance milk supply despite various local challenges.

Poland has performed remarkably in this trend, contributing significantly to the EU’s total results. In June alone, Polish dairy producers increased output by an astonishing 4%, considerably increasing the EU’s total results. France also played a key role, with its production increasing substantially in June. Germany, a dairy production powerhouse, reported a tiny but encouraging increase compared to June 2023, adding to the total growth.

However, the success story is not universal throughout the continent. Ireland’s dairy industry has faced challenges, with June output falling by 1%. These challenges could be attributed to [specific factors such as weather conditions, feed expenses, or government policies]. Though this reduction is an improvement over prior months’ steeper declines, it contrasts sharply with improvements witnessed in other important dairy-producing countries.

Global Milk Production: A Story of Interconnected Declines and Surprising Growth

Milk production in the Netherlands is declining significantly, mirroring regional and worldwide trends. Dutch dairy producers witnessed a 3% decrease in July compared to the previous year. Over the first seven months of 2024, total milk volume is 1.6 percent lower.

This declining tendency isn’t limited to the Netherlands. Several major dairy-exporting nations throughout the world are facing similar issues. For example, Argentina’s milk production dropped 7% in June, while Uruguay’s plummeted 13%. The United States likewise recorded a 2% reduction in milk output over the same time.

In contrast, Australia is an anomaly, with a 3% increase in milk output, breaking the global declining trend. Such variances illustrate the many variables influencing dairy output across locations, emphasizing the significance of resilience and adaptation in the dairy farming business.

Rising Milk Prices: An Industry in Flux and What It Means for You

Milk production changes are significantly influencing milk prices across the European Union. The 8% rise in milk prices in July 2024 over the same month in 2023 is strong evidence of this trend. When milk production declines, like in the Netherlands and Ireland, supply tightens, resulting in higher prices. This price rise is also influenced by [specific factors such as market demand or government policies].

Furthermore, the comparison of EDF and ZuivelNL milk pricing demonstrates this tendency. In July, most firms saw a rise in milk prices, with just a handful holding prices steady and one reporting a decrease. This reflects a more significant, industry-wide trend toward higher milk pricing, mainly owing to changing production levels.

Understanding these patterns can help dairy producers negotiate the market more effectively. Are you ready to adjust to the changes? Whether aiming to increase output or save expenses, remaining aware and agile will be critical in these uncertain times.

What’s Behind the Fluctuations in Regional Milk Production?

Have you ever wondered why certain places see a surge in milk production while others lag? When studying these different patterns, several variables come into play. Weather conditions are a crucial factor. Unfavorable weather may disrupt feed supplies and cow health, affecting milk output. On the other hand, favorable weather conditions might increase output rates. Have you recently faced any weather-related issues on your farm?

Feed expenses are also an important consideration. Rising feed costs discourage farmers from retaining big herds, reducing milk yield. Have you seen any swings in feed prices, and how have they impacted your operations?

Government policies also have a huge impact. Regulations governing environmental standards, animal welfare, and trade regulations might result in higher expenses or operational adjustments that may help or impede milk production. Have recent legislative changes in your nation affected your farm?

Market demand plays a pivotal role in shaping manufacturing decisions. Farmers are more likely to optimize productivity when milk prices are high. Conversely, low pricing might inhibit output, leading to reductions. Understanding and adapting to current market demand can empower your manufacturing strategy.

The Intricate Dance of Milk Production Trends: Balancing Opportunities and Challenges

Dairy producers face both possibilities and problems as milk production patterns shift throughout the EU and worldwide. Higher milk prices, such as the 8% rise in July 2024, may significantly improve a farmer’s bottom line. This price rise offers a cushion to withstand rising manufacturing costs, and promises improved profitability. But remember the other side: sustaining or increasing output levels amidst variable supply is no simple task.

For many farmers, effectively managing their farms is critical to navigating these changes. Given the reported decreases in areas such as the Netherlands and Ireland, the focus should be on improving herd health and milk output. Regular veterinarian checkups, adequate diet, and stress-free cow habitats are essential. Adopting technology to improve herd management may simplify many of these operations.

Consider using data to track cow performance and anticipate any health concerns before they worsen. Automated milking systems, precise feeding methods, and real-time data analytics may all provide significant information. This proactive strategy not only assures consistent output but also improves the general health of your cattle.

Innovation in feed quality should be considered. Climate change impacts grazing conditions and feed quality; thus, diversifying feed sources to include nutrient-dense choices will assist in sustaining milk production levels. Collaborate with agronomists to investigate alternate fodder or forage systems tolerant to shifting weather patterns.

Finally, developing a supportive community around dairy farming is critical. Networking with other farmers via local and regional dairy groups, attending industry conferences, and participating in cooperative ventures may provide emotional and practical assistance. Sharing information and resources contributes to developing a resilient and adaptable agricultural community that meets current and future problems.

Although increasing milk prices provides a glimpse of optimism and possible profit, the route to steady and expanded output requires planning and competent management. Dairy producers can successfully navigate these turbulent seas and secure a sustainable future for their farms by concentrating on herd health, adopting technology, optimizing feed techniques, and developing communities.

The Bottom Line

As we’ve negotiated the changing terrain of EU dairy production, it’s become evident that regional discrepancies are distinctively influencing the business. The extreme disparities between nations such as Poland, which is increasing, and the Netherlands, which is declining, underscore the global dairy market’s complexity and interdependence. Furthermore, although some areas are suffering a slump, others, such as Australia, are seeing growth that defies global trends. European milk prices have risen during these developments, creating both possibilities and problems for dairy producers.

Today’s challenge is adjusting to the dairy industry’s altering trends. Staying informed and active with industry changes is critical for navigating this volatile market. As trends shift, your ability to adapt proactively will decide your success. Maintain industry awareness, embrace change, and prosper in uncertainty.

Discover how modest gains and strategic shifts are shaping the dairy industry’s future. Read more.

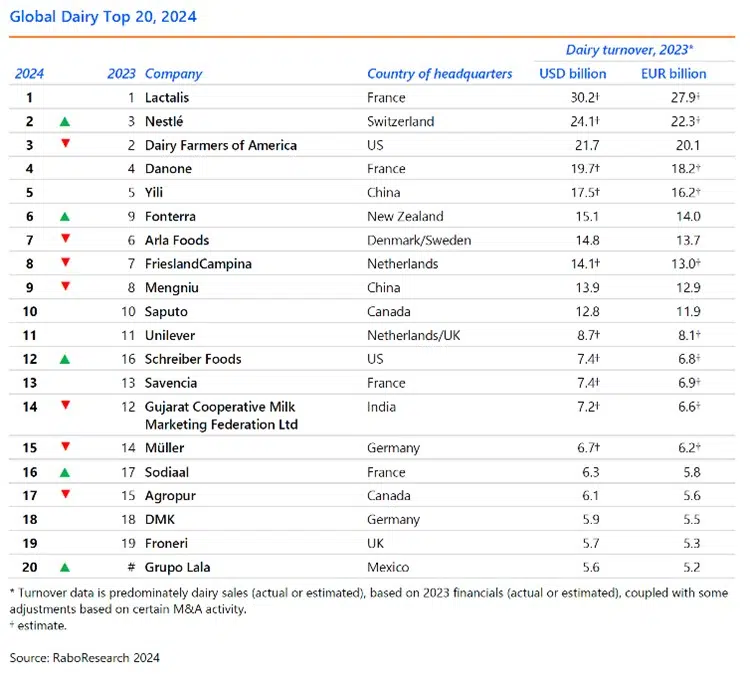

Summary: Are you curious about the latest trends in the global dairy industry? RaboResearch’s annual Global Dairy Top 20 report reveals a year marked by modest gains and strategic shifts among the world’s leading dairy companies, with a 0.3% increase in combined turnover in US dollar terms, a significant drop from the previous year’s 8.1% growth. Lactalis continues to dominate, while Nestlé has leapfrogged Dairy Farmers of America due to fluctuating milk prices. Due to favorable foreign exchange changes, Mexico’s Grupo Lala debuted in the top 20. The report also highlights limited M&A activity, with upcoming deals poised to reshape the industry’s landscape. The dairy industry continues to experience limited merger and acquisition (M&A) activity, with Danone’s divestment of Russian business and the shedding of its Horizon Organic and Wallaby brands being notable exceptions. Insights into these strategic shifts and modest gains offer essential information for any dairy industry stakeholder.

Global Dairy Top 20 report shows a 0.3% increase in combined turnover for leading dairy companies in US dollar terms.

Lactalis remains the number one dairy company for the third year.

Nestlé climbs to second place, surpassing Dairy Farmers of America due to weaker milk prices.

Grupo Lala makes its debut in the top 20, driven by strong organic growth and favorable foreign exchange rates.

Mergers and acquisitions activity remains limited, with notable exceptions like Danone’s divestments.

Upcoming deals, including Unilever’s ice cream business divestment, suggest potential industry rankings changes.

How do the leading dairy sector firms handle these difficult times? The RaboResearch Global Dairy Top 20 study is now out, providing an intimate look at the highs and lows of the world’s biggest dairy firms. This yearly study focuses on the financial health, strategy developments, and market dynamics affecting the sector.

This year’s figures, while reflecting the present environment, also underscore the dairy industry’s resilience. Despite a modest 0.3% increase in combined turnover, a sharp contrast to the previous year’s 8.1% rise, the industry continues to navigate challenges. From fluctuating foreign exchange rates to developing mergers and acquisitions (M&A) activity, these insights are critical for anybody involved in dairy production and sales.

Here are some essential highlights you should not miss:

Lactalis has kept the top rank for the third consecutive year with record revenue.

Grupo Lala entered the Top 20, boosted by positive FX developments.

M&A activity remains muted but strategic, with several important anticipated transactions.

Dairy firms in the United States prioritize internal development, with more than USD 7 billion set aside for new facility building and expansion.

“The Global Dairy Top 20 report is an invaluable resource for understanding the broader trends impacting the dairy sector worldwide,” according to an analyst at RaboResearch.

Stay with us as we investigate what these results indicate for your company and how you may adjust to the industry’s changing environment.

Global Dairy Industry: Modest Gains and Strategic Shifts Highlighted in 2023 Report

RaboResearch’s annual Global Dairy Top 20 study indicates a year of moderate advances and strategic moves in the dairy industry. The total sales of the world’s biggest dairy firms increased by 0.3% in US dollars, a dramatic contrast to the previous year’s 8.1% gain. While reduced milk prices in 2023 significantly slowed revenue growth, the industry’s potential for growth remains high. This slump mainly impacted European cooperatives, with seven firms globally reporting reduced sales in their currencies.

Furthermore, the year saw little merger and acquisition (M&A) activity, contributing to moderate growth. Compared to past years, when strategic acquisitions often supported growth, 2023 saw fewer. The limited M&A activity mirrored a more significant industry trend in which corporations refocused on core activities rather than extending their portfolios. This strategic recalibration offers a comprehensive picture of the industry’s current state and its cautious confidence about the future.

Lactalis Leads the Pack

Lactalis did it again! For the third year, the French dairy behemoth tops the Global Dairy Top 20 list. How did they do this? By exceeding USD 30 billion in yearly dairy-related income, a record for any dairy firm.

Lactalis’ success is based on two fundamental pillars: organic expansion and intelligent acquisitions. They’ve extended their footprint in developed and developing regions, capitalizing on global demand for dairy products. This technique has increased revenue and strengthened their market position.

In addition to its organic solid development, Lactalis has successfully negotiated the acquisition environment. Over the years, they’ve made significant acquisitions to expand its product line and geographical reach. Their strategic acquisitions have increased value, allowing them to retain a solid competitive advantage.

So, what lessons can other firms take from Lactalis? Focus on developing your core competencies while open to smart acquisitions that provide long-term advantages. Lactalis has perfected the delicate balance required to remain ahead of the curve.

Nestlé Climbs, DFA Slides: The FX Factor

While Lactalis remained at the top, Nestlé and Dairy Farmers of America saw significant rank shifts. Nestlé, for example, rose to second position, mainly aided by lower milk costs. Dairy Farmers of America, on the other hand, dropped to third place, indicating the same financial challenges.

But what triggered these changes? The shifting foreign currency (FX) rates had a significant effect. The value of the US dollar fluctuated, affecting the income of these worldwide titans. For Nestlé, good FX movements mitigated the impact of reduced milk prices, allowing them to retain excellent sales in USD. Dairy Farmers of America were not as lucky since lower domestic milk prices hurt hard, and any prospective FX advantages were insufficient to preserve their former position.

The complicated interaction between milk prices and foreign exchange rates explains how global variables may impact localized results. Keeping an eye on these developments is more important than ever to be competitive in the worldwide dairy industry.

Grupo Lala Joins the Global Elite: A Triumph of Strategy and Strength

Grupo Lala of Mexico has made its maiden appearance in the Global Dairy Top 20, a significant achievement. What propelled them to this top list? A mix of favorable foreign currency (FX) developments and organic solid revenue growth. The Mexican peso’s 11.8% increase versus the US dollar significantly impacted this situation. Grupo Lala had a 6% increase in organic sales growth in Mexican pesos, propelling their performance and ousting Ireland’s Glanbia off the list. This result emphasizes the value of local market strength and careful budget management. Are you intrigued by the tactics they used? It’s an enthralling account of negotiating the intricate global dairy market.

Refocusing for the Future: A Strategic Shift in Dairy M&A Activities

The dairy business continues to see modest merger and acquisition (M&A) activity. Danone’s recent divestiture of its Russian operations and discontinuation of its Horizon Organic and Wallaby brands are significant instances. Why is there this restraint? It is part of a more important trend in which corporations concentrate on their core activities, striving for more simplified processes and better efficiency.

For example, Danone is not alone in its strategy adjustment. Many dairy companies are returning to basics, eliminating less lucrative or non-core sectors. This tendency indicates a desire to focus on what they do best: producing high-quality milk, cheese, and other dairy products. It represents a shift towards sustainability and long-term development.

While this may result in fewer dramatic headlines about industry-changing acquisitions, it indicates a thoughtful recalibration geared at long-term performance rather than fast benefits. Understanding this transformation enables dairy farmers and industry stakeholders to integrate with more extensive market plans and capitalize on new prospects for development and stability.

Ready for Some Industry Shake-Ups?

Consider impending transactions that might significantly alter the Global Dairy Top 20 standings:

Unilever’s Ice Cream Exit

Unilever is one of the big players making headlines. They intend to offload their ice cream company, which might have far-reaching consequences. Consider the scaling prospects for an acquired firm! This change underscores Unilever’s approach of focusing on its core capabilities, possibly opening up more market space for current and new dairy giants.

Fonterra’s Core Focus

Then there’s Fonterra, which is planning to exit its consumer business. They’re getting back to basics and focusing on their core activities. This strategic choice reflects a broader industry trend: businesses are narrowing their focus to create more excellent value and adapt to changing market circumstances.

Sustainability and Strategic Pivots

These developments point to a broader narrative: an industry realigning itself. Sustainability has become more critical in these strategic pivots. As Unilever and Fonterra alter their sails, they navigate market movements and an increasing need for sustainable operations.

What does this mean to you? Maintain a watchful eye on the industry scene. These transitions might lead to new collaborations, inventions, and market positioning possibilities. Who will come out on top next? Only time will tell.

US Dairy Industry’s Interior Makeover: Is Bigger Always Better?

When it comes to US dairy firms, they are altering gears. Instead of pursuing acquisitions, they’re focusing their efforts internally. Consider this a primary home renovation job. With more than $7 billion set aside for new plant development and expansions from 2023 to 2026, the emphasis is squarely on increasing production capacity, particularly in cheese. This internal growth strategy demonstrates a commitment to improving operations and responding to market needs.

The Bottom Line

This year’s Global Dairy Top 20 study highlights moderate improvements and smart reorganizations. Lower milk prices and little M&A activity have led many businesses to prioritize internal development and core operations. Significant firms like Lactalis and Nestlé dominate, while newcomers like Grupo Lala make noteworthy debuts. Upcoming transactions and strategic pivots indicate that the dairy landscape may soon evolve.

Dairy farmers must remain aware of these developments. Strategic adjustments, particularly those involving mergers and acquisitions, have the potential to alter market dynamics drastically. Are you prepared to adapt and prosper amid these changing trends? The dairy industry’s future will provide problems and possibilities; you’re ready to seize them.

Find out how the 5.5% jump in the GDT index affects your farm’s profits and planning. Why is it important? Keep reading to learn more.

Summary: The Global Dairy Trade (GDT) index experienced a significant 5.5% increase, marking its third consecutive rise following a sharp decline in July. The recent GDT auction saw 181 bidders participating, resulting in an average winning price of $3,920 per metric tonne. Despite a slight drop in cheddar prices, other dairy products like whole milk powder, mozzarella, and anhydrous milk fat saw notable price increases. This price surge comes amid global milk supply challenges, with forecasts indicating only a marginal increase in the coming months. Dairy processors like Dairygold and Tirlán have responded by encouraging suppliers to maximize milk production to meet rising demand.

The GDT index has increased for the third consecutive time, recovering from a significant drop in July.

The latest auction saw active participation with 181 bidders, leading to an average winning price of $3,920 per metric tonne.

Most dairy products saw price increases, except for a slight decrease in cheddar prices.

Global milk supply faces challenges with only a marginal increase expected in the near term.

Dairy processors like Dairygold and Tirlán are urging suppliers to boost milk production due to rising demand.

The Global Dairy Trade (GDT) pricing index rose an impressive 5.5%, marking the third consecutive gain. You are not alone if you’re scratching your head and wondering what this implies for your dairy farm. This surge may have far-reaching consequences for your business. How will this impact your bottom line? What tactics should you use to optimize your gains? Let’s examine these questions to guarantee you don’t fall behind in this fast-changing industry.

Market Springs Back: GDT Index Climbs 5.5%, Signals Strong Recovery

The Global Dairy Trade (GDT) pricing index is up 5.5%, indicating the third straight gain in recent trading activities. This significant increase comes after minor gains on July 16 and August 6, indicating a steady recovery. It’s worth noting that the index fell over 7% on July 2, so this new rally strongly reflects market resilience and confidence.

Bidding Frenzy: 181 Players Compete for Nearly 35,000MT of Dairy Products

The latest GDT trading event showcased an impressive level of activity and competition. One hundred eighty-one bidders participated in the auction, which spanned 18 bidding rounds and lasted almost three hours. By the end of the event, 34,916 metric tonnes (MT) of dairy products were sold to 112 winning bidders. The average winning price reached $3,920 per metric tonne (MT), reflecting a notable increase of 6.5% compared to the previous auction on August 6. This uptick signals a promising trend for dairy farmers looking to maximize their returns in forthcoming auctions.

Resilient Comeback: GDT Index Bounces Back Following July’s Sharp Decline

The GDT index has recovered well after a severe plunge of over 7% on July 2. Since then, the index has made consistent, if tiny, advances in the two successive auctions conducted on July 16 and August 6. These little rises pave the way for a massive jump in the most recent trading event. Specifically, the small increases in July and early August established the groundwork for recovery, indicating market steadiness and increased trader confidence. This gradual progress culminated in a robust 5.5% increase, indicating a good recovery trajectory for the GDT index. Resilience in dairy markets may indicate a steady prognosis in the coming months.

Navigating the Price Surge

The recent increase in the GDT price index is more than just a number; it represents an opportunity for dairy producers. After months of instability, a 5.5% gain indicates a market rebound that every farmer should pay attention to. But what does this imply on the ground?

For starters, higher pricing implies more financial rewards for your milk. This allows you to invest in your business by updating equipment or boosting feed quality. Tirlán chair John Murphy notes the issue: “Butter and cream prices have risen significantly in recent weeks due to scarcity.”

The global milk supply is expected to grow, mainly due to the southern hemisphere’s forthcoming seasonal production boom. However, the total supply is predicted to be consistent with the prior year. Given the existing scenario, the main message for dairy producers is to improve production methods and continuously monitor component levels. The market is primed for growth, and taking early actions might help you optimize your gains during this optimistic moment.

Global Milk Supply: Modest Uptick Amid Challenges and Opportunities

Looking forward, the global milk supply projection shows a slight increase in output. However, the growth is projected to be small. Weather fluctuation, feed quality, and economic demands remain significant issues. In Europe, severe weather and feeding circumstances have influenced milk component levels, notably butterfat.

Seasonal production ramp-ups in the southern hemisphere, particularly in New Zealand and Australia, will significantly impact market dynamics. Historically, this era witnessed a boom in milk production, which might substantially impact global supply systems. According to industry analysts, this increase in supply may sustain present prices or apply downward pressure if supply increases faster than demand.