Learn how dairy producers are earning big milk checks and benefiting from low feed costs this summer. Will this profitable trend last despite challenges like heifer shortages?

Dairy farmers are reaping substantial milk checks while benefitting from decreased feed prices. This unusual position provides a tremendous opportunity for everyone in the dairy business, including farmers and analysts. The present very favorable economic climate enables dairy producers to expand their businesses. A boom like this typically results in more milk supply and cheaper pricing. Still, problems like heifer scarcity and external factors limit expansion. Understanding how to handle these moments may help dairy producers achieve immediate and long-term success. The dairy sector environment is reshaped by fundamental market factors, such as decreasing feed prices and increased meat income.

Unprecedented Financial Prosperity: Dairy Producers Enjoy Robust Revenue Streams and Low Feed Costs

| Month | Corn ($/bushel) | Soybeans ($/bushel) | Soybean Meal ($/ton) |

|---|---|---|---|

| April | 4.20 | 11.00 | 325.00 |

| May | 4.10 | 10.75 | 320.00 |

| June | 4.00 | 10.50 | 310.00 |

| July | 3.90 | 10.35 | 307.40 |

The present financial picture for dairy farmers is powerful. Substantial milk checks and increased money from cattle sales have greatly improved the bottom line. Low feed costs boost financial wealth. Beneficial weather in the maize Belt has caused the USDA to rank 68% of maize and soybeans in outstanding condition, providing dairy farmers an ideal opportunity to lock in feed prices at multi-year lows. This attractive mix of high revenues and minimal inputs opens up untapped opportunities for financial stability and future challenge preparedness.

Converging Challenges: Factors Constraining Dairy Production Growth

The present market dynamics in the dairy business are heavily driven by variables that limit milk production growth. The heifer scarcity is a significant barrier, restricting herd growth and driving prices to $3,300 per head. Higher interest rates hamper dairy investment by increasing financing costs. Hot summer temperatures diminish milk output and impair herd health, necessitating extra attention. Furthermore, avian flu disrupts feed supply systems. Despite reduced feed prices, interruptions due to health problems in associated industries increase unpredictability. These issues, taken together, create a harsh climate for dairy farmers. While they provide good profits, their potential to increase milk output is restricted, limiting oversupply and stabilizing milk prices in the near run.

Soaring Heifer Prices Reflect Unprecedented Demand Amid a Heifer Shortage

| Date | Location | Average Price per Heifer | Price Range | Remarks |

|---|---|---|---|---|

| Last Week | Turlock Livestock Auction Yard | $3,075 | $2,850 – $3,300 | Record price range indicating high demand |

| This Week | Pipestone, Minnesota | $3,150 | Top 25 Average | Sustained high prices despite limited supply |

Heifer prices are skyrocketing, indicating a significant demand for dairy farmers to fill their barns. At the Turlock Livestock Auction Yard’s monthly video auction, Holstein springers recently sold for $2,850 to $3,300 each. Similarly, the top 25 springers averaged $3,150 each in the Pipestone, Minnesota auction. These rates reflect the necessity of securing heifers in the face of scarcity.

Concurrently, cull rates have dropped to record lows. In the week ending July 6, dairy cow slaughter fell to 40,189 head, the lowest level since December 2009 and 20.6% lower than the same week in 2023. This reduction suggests that farmers hold on to cows they could have slaughtered because of high heifer prices and replacement issues.

Consequently, dairy cow numbers are expected to grow, possibly boosting milk production. However, integrating lower-producing cows may decrease the average output per cow, making it challenging to optimize milk quality and efficiency.

Uneven Demand and Supply Dynamics Threaten Dairy Market Stability

| Commodity | Average Price (July 2024) | Quantity Traded | 4-Week Trend |

|---|---|---|---|

| Whey | $0.5055 | 2 | Up |

| Cheese Blocks | $1.8630 | 23 | Stable |

| Cheese Barrels | $1.8980 | 22 | Stable |

| Butter | $3.1140 | 69 | Up |

| Non-Fat Dry Milk | $1.1795 | 10 | Down |

The dairy market’s trajectory is finely balanced between demand and supply dynamics. Despite the present affluence, low demand for dairy products poses a considerable concern. Cheese consumption remains high due to local promotions and increased exports based on previous low pricing. However, it is still being determined if this tendency will continue. While spring’s record exports lowered cheese stocks, this activity is projected to slow, possibly raising inventory levels and increasing prices if fresh demand does not materialize.

Future cheese sales domestically are uncertain. A slowdown may quickly lower prices. The CME spot market shows volatility, with spot Cheddar barrels increasing by 6.25˼ to $1.9125 per pound and Cheddar blocks decreasing by 2.5ͼ to $1.865. These differences highlight cheese demand’s unpredictable nature.

Cheese’s domestic appeal helps to balance the market against shortages. Still, a reduction in demand or underperforming exports might upset this equilibrium. Industry worries are reflected in uneven spot market movements. Elevated pricing and deliberate inventory sell-offs are a balancing act against declining exports and unreliable domestic demand. The dairy industry’s survival depends on managing these uncertainties and reducing risks.

Converging Pressures: Divergent Trends in Whey and Milk Powder Markets Define Dairy Sector’s Future

The whey industry is increasing due to increased domestic demand, especially for high-protein varieties. This demand has limited dry whey production, raising prices. CME spot whey powder gained by 0.75̼ this week, hitting 51.75̼, its highest level since February. The USDA’s Dairy Market News indicates that supplies are limited, with producers selling out monthly.

In contrast, the milk powder market in the United States has recurrent production deficits and poor export prospects. At the most recent Global Dairy Trade (GDT) auction, prices of skim milk powder (SMP) and whole milk powder fell by 1.1% and 1.6%, respectively. CME spot nonfat dry milk (NDM) initially followed this pattern. Still, it rallied late in the week, closing at $1.1975, up 1.75 percent from the previous Friday.

The effect of these changes is noticeable. Strong domestic demand has reduced whey supply and raised costs. Meanwhile, the milk powder market faces restricted supply and sluggish exports, limiting prospective price increases. These opposing developments show the dairy market’s varied pathways.

Heatwave-Induced Strain: Analyzing the Ripple Effects on Butterfat Levels and Cream Pricing Dynamics

The warmer weather has significantly impacted milk output and butterfat levels. Cream prices rose in the East and West but stayed stable in the Central Region. Butter output has decreased due to the bad weather, particularly in the West. Despite this, butter prices dipped this week due to heavy trade in Chicago. The market’s forecast of stable pricing through October promotes fast sales to prevent storage expenses. The CME spot market saw an astonishing 69 cargoes change hands, the most in over a year. Despite the high costs, buyers remain active, fearing future shortages.

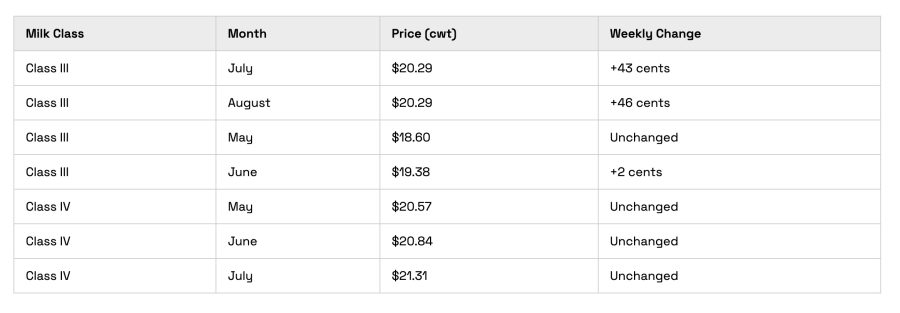

Whey and Cheddar Surge Lifts Class III Futures: Strong Market Dynamics Promise Financial Stability

The healthy whey and cheddar barrel markets have bolstered 2024 Class III futures. The August contract increased by 28 cents to $19.97 per cwt, while the September and October contracts gained roughly 50 cents, finishing in the mid-$20s. Despite Class IV futures holding high at about $21.50, most contracts lost money. This pricing should cover expenditures and allow for debt repayment or future planning.

Weather-Induced Prosperity: Dairy Producers Benefit from Ideal Crop Conditions Driving Down Feed Costs

The present level of feed prices provides a significant relief for dairy farmers, owing to the healthy condition of the maize and soybean harvests. Favorable weather in the Corn Belt has resulted in extraordinary crop growth, with the USDA rating 68% of corn and soybeans as good to excellent. Cooler-than-normal temperatures have helped maize during its crucial pollination season, resulting in record-high yields. Feed prices have dropped further, with September corn futures reaching $3 and the December contract ending at $4.055 per bushel, a 9 percent decrease from last Friday.

Similarly, increased confidence in soybean supply has pulled November soybean prices down by 30 to $10.355 per bushel, while December soybean meal futures have declined by $6.70 to $307.40 per ton. These patterns enable dairy farmers to lock in feed prices at multi-year lows, allowing them to profit on historically strong dairy margins.

Crafting a Comprehensive Risk Management Strategy for Dairy Producers

Dairy farmers need effective risk management to navigate fluctuating market situations. Locking down feed prices at current lows is an appealing approach. Producers that secure feed contracts today may stabilize input costs, reducing future price concerns and assuring more predictable financial planning. This foresight ensures profitability even if feed markets rise suddenly.

Furthermore, the Dairy Income Protection (DRP) scheme provides a strong safety net, protecting against quarterly milk sales income declines based on pricing and production levels. This protects farmers from market changes and ensures revenue stability. Futures and options also help to control price risk. Hedging future milk sales or feed purchases allows producers to lock in advantageous pricing while reducing market vulnerability. This guarantees that manufacturers may maintain lucrative margins by taking advantage of rising pricing.

Locking low feed costs, participating in the DRP program, and leveraging futures and options contribute to a holistic risk management plan. It enables dairy farmers to control expenses, protect income, and take advantage of favorable market circumstances, resulting in a more predictable and profitable financial future.

The Bottom Line

Dairy farmers face an environment characterized by high milk check income and low feeding expenses. Celebrating their financial success, they also confront a unique set of obstacles and possibilities. High heifer prices, low slaughter rates, and robust demand all point to continued profitability. However, low demand, export uncertainty, and weather changes need a deliberate strategy. Dairy farmers must lock in low feed prices, use risk management techniques such as Dairy Revenue Protection (DRP), and keep alert to market trends. To achieve long-term success, be educated and nimble. Now is the moment to use the economic recovery to increase your farm’s resilience and sustainability.

Key Takeaways:

- Producers are experiencing significant financial gains, with high milk checks and additional revenue from beef sales.

- Feed costs are at multi-year lows, providing an opportunity for dairy producers to secure favorable financial terms.

- Efforts to increase milk production are hampered by a shortage of heifers, along with elevated interest rates, high summer temperatures, and the bird flu.

- Heifer prices have surged, reflecting heightened demand against a backdrop of scarce supply.

- Despite reduced cull rates, milk yields may decline as producers hold onto lower-production cows due to heifer shortages.

- Cheese and whey markets show variable trends, with strong domestic demand driving prices upward, while export volumes appear poised to decrease.

- The combination of high temperatures and decreased butterfat levels has led to fluctuating butter and cream prices.

- Class III futures are buoyed by strong whey and Cheddar prices, promising financial stability for dairy producers.

- Ideal weather conditions in the Corn Belt are contributing to low feed costs, enhancing economic prospects for dairy producers.

Summary:

Dairy farmers are experiencing financial prosperity due to increased milk checks and decreased feed prices, allowing them to expand their businesses and increase milk supply and cheaper pricing. However, problems like heifer scarcity and external factors limit expansion, such as higher interest rates, hot summer temperatures, and avian flu. Heifer scarcity restricts herd growth, driving prices to $3,300 per head. Cull rates have dropped to record lows, and dairy cow slaughter has fallen to 40,189 head, the lowest level since December 2009. Uneven demand and supply dynamics threaten dairy market stability. The dairy industry faces challenges such as increasing domestic demand for high-protein varieties, limited dry whey production, and fluctuating market dynamics. Weather-induced prosperity has provided ideal crop conditions, driving down feed costs. Effective risk management strategies are needed to navigate fluctuating market situations, such as locking down feed prices at current lows and using futures and options to control price risk.