Feeling the squeeze in the dairy market lately? You’re not alone. Many of us have been watching the Chicago Mercantile Exchange like hawks, and Wednesday’s numbers threw us a curveball, didn’t they? With cash dairy prices mostly down, it’s time to look closely at what’s happening out there.

CME cheese prices took a hit today. Barrels dropped by 12.5 cents to $2.1250 per pound with just one lot traded. Blocks weren’t spared either, falling by 6.5 cents to $2.0750 per pound, also with one load exchanged. Nonfat dry milk (NDM) slid to $1.3050 per pound, shedding a penny with five lots traded. Fourth quarter Class III futures showed mixed results, averaging $21.88 per hundredweight, down by nine cents. Meanwhile, Q4 Class IV futures slipped 15 cents to $22.64 per hundredweight. Grain futures aren’t faring much better. September corn settled at $3.6525 per bushel, down by two cents, while the nearby soybean contract finished at $9.5850 per bushel, losing nine cents.

Let’s break down the numbers:

Dry whey: Down $0.0125, now at $0.5525. We saw five trades between $0.5525 and $0.56 in this range.

Blocks: D by $0.0650, now standing at $2.0750. Only one trade occurred at that price.

Barrels: Dropped $0.1250, coming in at $2.1250 after just one trade.

Butter: Stayed unchanged, holding steady at $3.1975.

Nonfat dry milk: Fell by $0.01 to $1.3050, with five sales in the range of $1.30 to $1.3150.

Daily CME Cash Dairy Product Prices ($/lb.)

Final

Change ¢/lb.

Trades

Bids

Offers

Butter

3.1975

NC

0

0

0

Cheddar Block

2.075

-6.5

1

0

2

Cheddar Barrel

2.125

-12.5

1

2

1

NDM Grade A

1.305

-1

5

2

3

Dry Whey

0.5525

-1.25

5

1

0

Weekly CME Cash Dairy Product Prices ($/lb.)

Mon

Mon

Tue

Wed

Current Avg.

Prior Week Avg.

Weekly Volume

Butter

3.175

3.1975

3.1975

3.19

3.159

16

Cheddar Block

2.14

2.14

2.075

2.1183

2.082

8

Cheddar Barrel

2.25

2.25

2.125

2.2083

2.225

2

NDM Grade A

1.2975

1.315

1.305

1.3058

1.279

32

Dry Whey

0.565

0.565

0.5525

0.5608

0.561

7

CME Futures Settlement Prices

Mon

Tue

Wed

Class III (SEP) $/CWT.

22.54

22.55

22.12

Class IV (SEP) $/CWT.

22.27

22.59

22.59

Cheese (SEP) $/LB.

2.205

2.194

2.155

Blocks (SEP)$/LB.

2.14

2.14

2.14

Dry Whey (SEP) $/LB.

0.54

0.54

0.54

NDM (SEP) $/LB.

1.2775

1.3045

1.2875

Butter (SEP) $/LB.

3.1995

3.2175

3.2175

Corn (SEP) $/BU.

4.24

3.6725

4.2625

Corn (DEC) $/BU.

3.86

3.925

3.905

Soybeans (SEP) $/BU.

9.6075

9.695

9.5925

Soybeans (NOV) $/BU.

9.81

9.8775

9.765

Soybean Meal (SEP) $/TON

312.2

317.3

310.5

Soybean Meal (DEC) $/TON

308.1

312.4

308.3

Live Cattle (OCT) $/CWT.

176.98

179.18

178.68

Trading commodities futures and options entails considerable risk. Investors must carefully balance these risks with their financial status. Although we obtained the material from credible sources, it has not been independently confirmed. This article represents the author’s viewpoint, not necessarily that of The Bullvine, and is meant as a solicitation. Remember that previous performance does not guarantee future outcomes.

Find out how rising milk prices and high butterfat levels are driving up dairy farmers’ profits. Want to know the latest trends and stats? Read our in-depth analysis.

Summary: Have you been keeping an eye on your dairy margins lately? If not, you might be in for a pleasant surprise. August has brought about some noteworthy improvements for dairy farmers, particularly those who have invested wisely in their marketing periods. Profitability has seen a much-needed boost, with milk prices soaring and feed costs holding steady. Curious about the specifics? Let’s dive into the cheese market, where block and barrel prices have hit their highest since October 2022, driven by a drop in cheddar cheese production. This tightening of spot supplies has resulted in firmer prices and unique challenges and opportunities for dairy farmers. And there’s more—while milk production is down, butterfat levels and butter production are smashing records. Cheese production in June dropped 1.4% from the prior year to 1.161 billion pounds, with cheddar production down 9% from 2023 and marking the eighth consecutive monthly decline. This allows dairy producers to capitalize on these quality advances while navigating the challenges of decreased milk quantities. But it’s not just about dairy: changes in crop yields for corn and soybeans also influence feed costs, shaping the broader landscape of your financial well-being. According to the USDA’s August WASDE report, lower soybean meal prices may benefit dairy businesses as feed is a substantial expenditure. In conclusion, higher milk prices and stable feed costs have created an optimistic scenario for dairy margins. The recovery in the cheese market and rising butterfat levels in the face of decreased milk output present complex but attractive options. Dairy producers must be vigilant and respond promptly to changing circumstances, as historically high margins provide ample space for increased profitability.

Dairy margins saw improvement in early August due to higher milk prices and steady feed costs.

Block and barrel cheese prices reached their highest since October 2022, mainly due to reduced cheddar cheese production.

Cheese production in June 2023 fell 1.4% from the previous year, with cheddar production down 9%.

Butterfat levels and butter production are at record highs despite the decline in milk production.

USDA’s August WASDE report indicates lower soybean meal prices, potentially reducing feed costs for dairy farmers.

The current favorable conditions in milk prices and feed costs offer a chance for higher profitability in the dairy industry.

Have you observed any recent changes to your milk checks? You could be wondering why your earnings have suddenly improved. Well, it’s not all luck. Dairy margins have increased considerably in the first half of August, owing to rising milk prices and record butterfat levels. This increase boosts profitability and provides a much-needed respite from the constant feed expenses. But what is truly driving this favorable shift? Let’s go into the specifics and examine how these changes affect the dairy industry.

Surging Milk Prices and Steady Feed Costs: A Recipe for Improved Dairy Margins

The dairy market is navigating a complicated terrain full of difficulties and opportunities. Dairy margins improved significantly in the first half of August, primarily due to rising milk prices. Due to solid cheese market dynamics, dairy producers are better positioned as CME Class III Milk futures rise. Even though feed prices have stayed consistent, this constancy has been critical in increasing profitability. The rise in milk prices and steady feed costs provide a balanced equation that improves total margins, allowing farmers to run their businesses more successfully despite continued problems.

Have You Noticed What’s Happening in the Cheese Market? It’s Been Quite a Ride Lately.

Have you observed what’s going on in the cheese market? It’s been quite the trip lately. The CME Class III Milk futures have gained dramatically owing to a strong cheese market. Last week, block and barrel prices at the CME reached record highs not seen since October 2022. This increase is primarily due to a decline in cheddar cheese output, which has reduced spot supply and caused prices to rise in recent weeks.

Cheddar output, in particular, has been declining steadily, down 9% since 2023. This is the sixth straight monthly decline. Several variables contribute to this tendency, including high temperatures and persistent herd health difficulties associated with the avian flu pandemic. These factors have produced a perfect storm, drastically reducing cheddar yield.

Consequently, lower output has resulted in tighter spot supply and higher pricing. The drop in cheese output adds another layer of complexity to the market, making it critical for dairy producers to remain knowledgeable and adaptable. Are you ready for these upheavals in the cheese market?

Did You Know? Rising Butterfat Levels Amid Declining Milk Production

Did you know that, although total milk output has decreased, butterfat levels in milk have increased significantly? This may appear paradoxical at first look, yet it is correct. Butterfat percentages have reached all-time highs, regularly outperforming previous year fat tests since June 2020. What drives this phenomenon?

While overall U.S. milk production is down 0.9% year over year through June, the lowest level in four years, the quality of the milk produced is impressive. Butter output in June increased by 2.8% from the previous year to 169.15 million pounds due to rising butterfat content, demonstrating the industry’s flexibility and resilience.

This increase in butterfat levels has given a silver lining among the difficulties. With butterfat percentages at an all-time high, dairy producers may capitalize on these quality advances while navigating the challenges of decreased milk quantities. This potential maximizes profitability and efficiency in processing, guaranteeing that each drop of milk produces the best possible return. The rise in butterfat levels enhances the quality of dairy products and provides an opportunity for dairy producers to adjust their production strategies to maximize profitability.

Ever Considered How Crop Yields Influence Your Feed Costs?

Let’s take a quick look at feed expenses and crop yields. Have you looked at the USDA’s August WASDE report? It’s quite an eye-opener! They have increased yield and production predictions for maize and soybeans. But what does this imply for us in the dairy farming industry?

For openers, predicted corn-ending stockpiles have decreased marginally. This is mainly owing to fewer harvested acres and increased predicted demand. Less maize will be available, which may keep feed prices flat or raise them somewhat.

Conversely, since July, soybean ending stockpiles have risen dramatically by 135 million bushels. This spike has placed downward pressure on soybean meal costs, giving your feed budget some breathing space. Lowering soybean meal prices may be beneficial since feed is a substantial expenditure for dairy businesses. How will you modify your feeding plan in light of these changes?

The Bottom Line

As previously discussed, higher milk prices and stable feed costs have produced an optimistic scenario for dairy margins. The current recovery in the cheese market and rising butterfat levels in the face of decreased milk output present complicated but attractive options. These options include adjusting production strategies to focus on high-butterfat products, optimizing feed plans to take advantage of changing crop yields, and closely monitoring market dynamics to make informed pricing decisions. Furthermore, shifting crop yields influence feed costs, emphasizing the need for strategic planning.

Dairy producers must be watchful and respond promptly to these changing circumstances. With historically high margins, there is plenty of space to strategize for increased profitability. How will you take advantage of these large profit margins? What techniques will you use to optimize your profits? We encourage you to share your strategies and learn from each other, as the answers to these questions guide your dairy operation’s future success.

Find out how rising milk demand is reducing cheese stocks and affecting prices and exports. Will this trend keep changing the dairy market? Learn more here.

The dairy market is changing in a terrain defined by uncertainty. Growing demand for milk here and abroad has resulted in declining cheese supplies.

Over successive months, cheese supplies in cold storage have dropped, leading to a dramatic price rise and difficulties for new exporting companies. Reflecting this, the USDA observes, “Cheese markets are not bullish or bearish, but indecisive.” LaSalle Street shows this feeling with changing spot Cheddar block and barrel pricing.

“Cheese markets are not bullish or bearish, but indecisive.” – USDA

These factors affect home as well as foreign markets. While decreasing mozzarella sales and high prices discourage new export contracts, they show steady domestic demand for cheese. The erratic character of market dynamics points to stormy times ahead for those involved.

Spring Surprises: An Unanticipated Shift in Cheese Production and Inventories

Month

Production Volume (Million Pounds)

Year-over-Year Change (%)

January

1,102

+1.2%

February

1,018

+0.9%

March

1,165

-0.7%

April

1,150

-1.0%

May

1,190

-1.5%

Driven by the ‘spring flush,’ when cows produce more milk, spring often marks a period of higher cheese output in the dairy sector. This surplus of milk leads to more significant, less expensive supplies for cheese makers, which in turn drives more manufacturing and inventory build-up. However, this year, the situation was different due to rising milk costs and growing demand, resulting in a contraction in cheese supplies.

Still, spot milk prices were high this year as cheese’s local and export demand increased. This odd situation resulted in cheese supplies declining from March through May, the lowest May inventories since 2019.

The present situation emphasizes how global demand and price changes may disrupt established dairy industry supply lines.

Demand Dynamics: Unpacking the Surge in Milk Consumption and Its Ripple Effects

Time Period

Export Demand (Million Pounds)

Domestic Demand (Million Pounds)

Total Demand (Million Pounds)

Q1 2023

250

1,200

1,450

Q2 2023

300

1,250

1,550

Q3 2023

320

1,280

1,600

Q4 2023 (Projected)

340

1,300

1,640

For several reasons, both domestic and export milk demand has increased. American tastes for dairy goods like unique yogurts and handcrafted cheeses have changed. This shift in consumer preferences is further fueled by the economic recovery after the pandemic, which has increased disposable income and a greater focus on health and nutrition, thereby boosting the demand for dairy products.

Globally, U.S. milk products are much sought after because of their competitive price and superior quality. Rising Asian and Latin American emerging markets are increasingly looking for nutrient-rich diets. Additionally, increasing exports ease trade barriers.

This demand increase has limited milk supplies for cheese manufacture. Usually, the spring flush period sees an excess of inexpensive milk aimed toward cheese manufacturing; however, rising milk costs and growing demand have altered this year and resulted in a contraction in cheese supplies. The increase in milk costs has made cheese production more expensive, leading to a decrease in cheese supplies.

Strong export markets and rising domestic consumption have pressured milk supply, pushing cheese makers to negotiate a limited milk procurement scene. Strong cheese demand and shortage have caused market instability and price rises.

A Season of Scarcity: The Decline in Cheese Stocks Reveals Market Vulnerabilities

Month

2019

2020

2021

2022

2023

2024

January

1.37

1.41

1.48

1.50

1.52

1.46

February

1.35

1.38

1.45

1.47

1.50

1.44

March

1.33

1.35

1.42

1.45

1.47

1.41

April

1.32

1.33

1.41

1.43

1.46

1.38

May

1.31

1.32

1.39

1.41

1.44

1.34

This year’s noteworthy drop in cheese supplies Cheese stockpiles at the end of May amounted to 1.44 billion pounds, a 3.7% decline from May 2023, marking the lowest May total since 2019.

While prices were flat in June as the market battled to draw fresh export business, this inventory loss caused a price spike in April and May. While sales of mozzarella dropped, home demand for other cheeses remained robust. With CME spot Cheddar blocks climbing 6.5ȼ to $1.91 per pound and barrels sliding 4ȼ to $1.88, the USDA labeled the market “indecisive.”

Global Competition Heats: U.S. Cheese Exporters Face Escalating Prices and Adverse Exchange Rates

Month

Cheese Exports (Million lbs)

YoY Change (%)

Export Price ($/lb)

January

60.5

+2.4%

1.75

February

58.2

+3.1%

1.78

March

59.8

+1.8%

1.80

April

61.3

+4.5%

1.85

May

62.0

+3.0%

1.82

Exporters are battling intense worldwide competition and rising cheese costs. Both domestic and export demand has raised prices, so U.S. cheese-less competitiveness abroad has suffered. This has made it difficult—a difficulty that still exists—to get fresh export contracts.

The strong U.S. currency makes American goods more costly for overseas consumers, aggravating the situation. A lower euro helps European producers; they have raised milk output, strengthening their market share. This increase in European production, particularly in Poland, sharpens the competitiveness of American exporters.

Additionally, changing agricultural policy, European nations are slowing down dairy herd declines and boosting cheese production capacity. New EU rules mandating Dutch farmers to distribute manure across more extensive regions might lower cattle numbers but have little effect on total output shortly.

Despite the challenges, U.S. exporters have the opportunity to navigate the high domestic cheese prices, robust overseas market, and the currency’s economic impact. The key to maintaining a strong presence in the global cheese market lies in strategic orientation, creative pricing, and innovative marketing techniques. These strategies can help the industry adapt to the changing landscape and continue to thrive in the worldwide cheese market.

Despite the market’s unpredictability, the robust domestic demand for certain cheese types provides a sense of stability. While mozzarella sales may have dipped, the consistent demand for other cheeses has helped maintain market buoyancy amidst fluctuating prices and inventory levels. The enduring popularity of Cheddar, in particular, has been a boon for local manufacturers. The strong demand for a variety of cheese options is a testament to the industry’s ability to navigate market uncertainty.

Whey Market Dynamics: A Tale of Domestic Resilience and Export Challenges

Product

Domestic Price

Export Price

Trend

Whey Protein Concentrate

$0.45/lb

$0.38/lb

Stable

Whey Powder

$0.49/lb

$0.37/lb

Increasing

Though exports are sluggish, domestic solid demand supports the whey product industry. While export loads are in the mid $0.30s per pound, USDA notes that some load categories are grabbing rates “at and above the $0.45/lb. Mark.” The prices of CME spot whey powder have increased by 2ȼ to a four-month high of 49ȼ by local demand. Although export difficulties still exist, the domestic market demonstrates confidence, which leaves the whey product market in a unique and somewhat dubious state.

Butter Resilience and Emerging Fears: High Inventories Yet Potential Shortages Loom

Month

Butter Stocks (million pounds)

CME Spot Butter Prices ($/lb)

January

360

$2.95

February

370

$3.05

March

375

$3.10

April

378

$3.12

May

380

$3.125

Butter stockpiles rose by 3.4% by the end of May to 380 million pounds, the highest level since 2020 and 1993. Still, worries about a possible shortfall later in the year cloud this increase. Rising milk prices and hot weather have boosted CME spot butter prices to $3.125, up 3.5ȼ this week, illustrating the market’s response to high domestic demand and growing expenses.

Milk Powder Puzzles: Navigating the Setbacks in Global and Domestic Markets

Month

CME Spot Nonfat Dry Milk (Price per lb.)

Notable Market Movements

January

$1.05

Stable with minimal shifts in market dynamics

February

$1.08

Minor increase due to lower production volumes

March

$1.12

Gradual upward trend as export demand briefly rises

April

$1.15

Peak due to supply chain disruptions

May

$1.10

Initial decline after export challenges emerge

June

$1.18

Brief recovery, but long-term outlook remains uncertain

A disappointment at the Global Dairy Trade Pulse auction highlights the declining milk powder industry. CME spot nonfat dry milk is down 2.25ȼ to $1.1825. Soft worldwide demand causes prices to struggle to gather even with minimal U.S. production. Reduced global demand limits price rises even if local output levels fall short of past highs.

European Dairy Gains Momentum: Navigating Increased Production and Stringent Regulations in a Competitive Export Landscape

Europe’s increasing production capacity stands out as the worldwide dairy industry adjusts to competition and demand. With Europe and the UK producing around 31.5 billion pounds in April, a 0.3% rise from April 2023, European milk production exceeded last year’s levels in February, March, and April. While lousy weather hindered growth in Ireland and the UK, Germany and France reported modest output gains.

Reflecting local agricultural efficiency, Poland saw a 5.4% year-over-year increase. Still, this expansion presents some difficulties. New rules meant to satisfy EU climate pledges fall on European farmers. Though there are expectations for slower legislative changes after recent elections, current rules continue.

The EU Nitrate Directive ends Dutch dairy farmers’ exemption from manure derogation rules, aggravating their logistical problems. A 1.3% decline in Dutch milk output in April resulted from almost 40% of Dutch farmers needing help finding adequate space for manure spreading, reducing their cattle numbers.

Strict rules and this higher output are changing the competitiveness of dairy exports. A significant dollar deficit for American goods gives European manufacturers an advantage and complicates the export scene for American exporters.

Market Outlook: A Complex Interplay of Domestic Growth and International Competition

The market’s state shows a combination of domestic strength and foreign challenges. Domestically, growing expenses have driven strong demand for milk and certain cheeses, driving prices even if sales of mozzarella have slowed down. The recent increase in CME spot whey powder indicates this demand has also bolstered whey product prices.

Globally, when European manufacturers raise their production, more competition and an unfavorable exchange rate pose challenges to U.S. cheese exporters. Further strict environmental rules complicate the supply scene even further.

Futures in Class III and IV mirror industry challenges. While fourth-quarter Class IV contracts climbed somewhat, stabilizing in the mid-$21s per cwt, third-quarter Class III futures decreased; the July contract fell 81ȼ to $19.46 per cwt.

Although dairy farmers face market instability, decreased feed costs and high-class III and IV milk prices provide some hope for alleviation in a convoluted worldwide market.

After USDA’s Acreage and Grain Stocks figures, December corn futures reached a three-year low. Farmers planted 1.5 million more acres of maize than the early spring poll expected—91.5 million acres. Soybean acreage dropped 400,000 acres to 86.1 million.

September corn futures plummeted 32ȼ to $4.085 per bushel from a massive stockpile of corn acres. The December contract dropped 32ȼ as well, to $4.215. Though there is flooding in the Northern Plains, grain is plentiful and helps keep feed prices down.

The Bottom Line

Recently, the dairy market has shown a combination of volatility and resilience. Unlike past patterns, rising demand has reduced cheese supplies, pushing prices higher but not maintaining them. Strong domestic whey demand helps raise spot prices even in lean export markets. Though possible shortages due to weather and higher milk costs loom, butter supplies have risen. European competitiveness and worldwide demand issues are testing the milk powder sector.

Ahead, the dairy market is expected to negotiate challenging terrain. European manufacturing advantages and political demands might affect world commerce, posing difficulties for American manufacturers. Strong domestic dairy demand might help the price, but global economic and environmental issues will always be critical. Stakeholders have always to be vigilant and ready for changes in the industry.

Key Takeaways:

Cheese stocks have decreased significantly, with inventories at their lowest since 2019, influencing price changes.

Domestic milk demand continues to soar, while both domestic and export demands are impacting cheese production and pricing.

The whey product market remains strong domestically, though export challenges persist.

Butter stocks are high but fears of shortages later in the year have driven prices up.

Milk powder market faces setbacks due to soft global demand, despite light U.S. output.

European dairy production is ramping up, creating stiffer competition for U.S. exports amidst regulatory challenges.

Grain market upheaval as USDA reports higher-than-expected corn inventories and planted acreage, leading to a dip in corn futures.

Lower feed costs are anticipated to benefit dairy producers in the face of volatile market conditions.

Summary:

The dairy market is experiencing a shift due to increasing demand for milk both domestically and internationally, leading to declining cheese supplies. This year, the situation was different due to rising milk costs and growing demand, resulting in a contraction in cheese supplies. The USDA has observed that cheese markets are not bullish or bearish, but indecisive. This situation affects both domestic and foreign markets, with decreasing mozzarella sales and high prices discouragering new export contracts. The current situation emphasizes how global demand and price changes may disrupt established dairy industry supply lines. Both domestic and export milk demand have increased due to changing consumer preferences, economic recovery after the pandemic, and rising Asian and Latin American emerging markets seeking nutrient-rich diets. Strong export markets and rising domestic consumption have pressured milk supply, pushing cheese makers to negotiate a limited milk procurement scene. The decline in cheese stocks has revealed market vulnerabilities, with cheese stockpiles at the end of May averaging 1.44 billion pounds, a 3.7% decline from May 2023. The erratic character of market dynamics points to stormy times ahead for those involved in the dairy industry.

Find out the latest trends in Class III milk futures and market movements from the Chicago Mercantile Exchange. How will these changes affect your dairy farming plans?

Today, we observed relatively subdued activity across Class III and IV markets. Class III prices saw a general increase of 10-15 cents, influenced by a mix of spot results. Notably, only one Class IV contract has been traded, with butter and nonfat prices showing a decline. This slow start to the week is particularly noteworthy, given the high anticipation surrounding the recent Milk Production report, which is expected to have a significant impact on the market.

Mixed Movements in Milk Futures: Class III Climbs While Class IV Drags

Contract

Class III Price ($/cwt)

Class IV Price ($/cwt)

July 2024

$19.87

$21.21

August 2024

$20.00

$21.15

September 2024

$20.10

$21.10

The overall market movements for Class III and Class IV milk futures presented a mixed picture. Class III futures showed a moderate growth, increasing by 10-15 cents, which can be seen as a positive response to spot market variations. On the other hand, Class IV futures saw limited activity with predominantly downward trends, including a single contract traded and declines in butter and nonfat milk prices. This mix of movements sets the stage for a cautious start to the week, highlighting the potential risks and opportunities in the market following the recent Milk Production report.

Optimism in Class III Milk Futures Amid Mixed Spot Market Results

Class III milk futures showed signs of optimism as prices rose by 10-15 cents across all contracts. This uptick was primarily a reflection of mixed spot market results. Specifically, block cheese prices increased to $1.8900 per pound, likely bolstering confidence among traders. In contrast, barrel cheese prices slightly declined to $1.9150 per pound. The divergence in spot prices seemed to fuel the cautious yet hopeful sentiment observed in the futures market.

Class IV Milk Futures See Limited Activity Amid Sluggish Market

Class IV milk futures were subdued, reflecting the overall sluggish activity in the market today. At the time of writing, only one Class IV contract had been traded, highlighting the lackluster interest in this segment. This cautious trading behavior was mirrored by declines in both butter and nonfat dry milk prices. Butter settled at $3.0650 per pound, giving up $0.0250, and nonfat dry milk followed suit with similar downward adjustments. The dipping prices in essential dairy commodities likely contributed to the softer stance in Class IV futures.

Spot Market Sees Mixed Cheese Prices and Declines in Butter and Nonfat Dry Milk

Product

Price Per Pound

Change

Cheese Blocks

$1.8900

+ $0.0450

Cheese Barrels

$1.9150

– $0.0050

Butter

$3.0650

– $0.0250

Nonfat Dry Milk

$1.19

– $0.0025

The day’s spot market activity saw block cheese prices lift to $1.8900 per pound, marking an increase of $0.0450 per pound with two lots traded. In contrast, barrel cheese prices slipped slightly to $1.9150 per pound, a decrease of $0.0050, with just one load exchanged.

Butter prices also dipped today, settling at $3.0650 per pound, down by $0.0250 per pound with one lot sold. Meanwhile, nonfat dry milk prices decreased by $0.0025 to $1.19, with three sales recorded, ranging from $1.19 to $1.1950 per pound.

This pattern of dipping prices across essential dairy commodities indicates a market cautious at the start of the week, especially following the highly anticipated Milk Production report.

Mixed Futures Activity: Class III Shows Gains, While Class IV and Butter Futures Retreat

In today’s market, July Class III futures rose by 12 cents to $19.87 per hundredweight, indicating positive movement despite mixed spot results. This rise contrasts with the nearby Class IV contract, which saw a decrease, losing 12 cents and settling at $21.21 per hundredweight.

Trends in Q3 “all-cheese” futures were upbeat, ending the day positively at $2.0333 per pound, adding $0.0220. However, the butter futures market mirrored the spot market softness, with July futures coming in at $3.0550 per pound, down $0.0300.

Promising Crop Conditions: Corn and Soybeans Show Strong Potential

Crop

Date

% Planted

% Good to Excellent

Corn

June 23, 2024

98%

69%

Soybeans

June 23, 2024

97%

67%

The latest Crop Progress report sheds light on the current status of crucial feed crops, such as corn and soybeans, which are vital to the dairy industry. As of June 23, 69% of the corn crop was rated good to excellent. This indicates a robust potential for feed quality, directly impacting feed costs and milk production efficiency. Similarly, soybean planting has nearly completed, with 97% of the crop in the ground and 67% rated good to excellent. This positive outlook in crop conditions could lead to stable or reduced feed prices, offering a silver lining for dairy farmers navigating volatile market conditions.

The Bottom Line

The CME dairy report for June 24, 2024, highlights modest growth in Class III futures, with prices rising 10-15 cents. However, Class IV futures were primarily static, with minimal trading activity. Key spot prices for blocks and barrels showed mixed results, indicating a potentially stabilizing market. Additionally, butter futures softened slightly.

For dairy farmers, these market movements suggest a cautiously optimistic outlook. The increase in Class III futures might signal improving dairy margins, especially as feed costs are expected to stabilize with promising crop progress reports. Keeping a close eye on market trends through resources like the CME and Progressive Dairy will be crucial for making informed decisions. Utilizing tools like Dairy Revenue Protection could offer additional security against volatile price swings, ensuring your operations remain resilient in the coming weeks.

Key Takeaways:

Class III milk futures showed modest growth, rising 10-15 cents.

Class IV milk futures experienced minimal trading activity and a decline in prices.

Block cheese prices increased, while barrel cheese prices fell slightly.

Butter prices and futures saw a decrease, with minimal trading activity.

Corn crop progress remains strong, with 69% rated good to excellent.

Soybean planting is nearly complete, with a 67% good to excellent rating.

Dairy margins are projected to improve for the rest of the year due to stronger milk prices and lower feed costs.

Summary:

The dairy market has seen a mixed start to the week, with Class III and IV milk futures showing moderate growth and a cautious outlook. Class III prices increased by 10-15 cents overall, driven by mixed spot results. However, Class IV futures saw limited activity with predominantly downward trends, including a single contract traded and declines in butter and nonfat milk prices. This mix of movements sets the stage for a cautious start to the week, highlighting potential risks and opportunities in the market following the recent Milk Production report. Block cheese prices increased to $1.8900 per pound, while barrel cheese prices slightly declined to $1.9150 per pound. July Class III futures rose by 12 cents to $19.87 per hundredweight, indicating positive movement despite mixed spot results. Q3 “all-cheese” futures ended the day positively at $2.0333 per pound.

Irish farmers demand higher milk prices to combat rising costs and market pressures. Can increased prices ensure the future of Ireland’s dairy sector?

Amidst the relentless financial pressures and unpredictable markets, Irish dairy farmers , with their unwavering determination, call for higher milk prices. Rising input costs, poor weather, and strict nitrates regulations have heavily burdened these farmers, reducing margins and threatening sustainability.

The dairy industry , a cornerstone of Ireland’s economy, supports rural livelihoods and contributes significantly to the national economy through exports and jobs. Organizations like the Irish Farmers Association (IFA) and the Irish Creamery Milk Suppliers Association (ICMSA) are advocating for fair milk prices, recognizing the industry’s vital role.

“We are at a critical juncture,” warned a representative from the IFA. “The current base milk prices are pushing us to the brink, especially with the surge in feed, fertilizer, and energy expenses. We need immediate relief.”

If these pressing issues are not promptly addressed, the dairy sector, a pillar of Ireland’s economy, could suffer a severe blow, forcing many farmers out of business. Addressing these challenges is not just important; it’s a matter of survival for Ireland’s dairy farmers.

As Irish dairy farmers grapple with the multifaceted challenges shaking their sector, one cannot overlook the stark figures that illustrate their plight. From declining production levels to stagnant milk prices, the data paints a clear picture of the adversities faced by those who form the backbone of Ireland’s dairy industry.

Year

Total Milk Production (million liters)

Base Milk Price (€/liter)

Input Costs (€/liter)

2018

7700

0.34

0.25

2019

7600

0.32

0.26

2020

7500

0.31

0.27

2021

7400

0.30

0.29

2022

7300

0.29

0.30

The figures above starkly demonstrate the mounting financial pressure on Irish dairy farmers, who are facing higher input costs without a corresponding increase in milk prices, leading to a vicious cycle of dwindling margins and decreased production.

The Multifaceted Challenge Facing Irish Dairy Farmers: Navigating Declining Production and Stagnant Prices

Irish dairy farmers face a significant challenge due to declining milk production and stagnant prices. Data from the Central Statistics Office (CSO) shows that milk volumes lag behind 2023 levels, creating pressure on farmers’ livelihoods.

The Irish Creamery Milk Suppliers Association (ICMSA) is leading the charge for change. Despite a slight improvement in the Global Dairy Trade (GDT) index and the Ornua Purchase Price Index (PPI), current prices still need to be improved. The ICMSA calls for a base milk price of 45c/L to restore sector confidence. High input costs and adverse weather conditions compound this need.

Stagnant prices and reduced production erode farmers’ margins, leading to tighter cash flows and difficulty managing costs. Stringent nitrate regulations and unpredictable weather patterns worsen this situation.

Higher milk prices are essential for the long-term viability of the sector. Addressing these challenges can restore confidence, stabilize the market, and ensure future growth.

The Escalating Costs Squeezing Ireland’s Dairy Sector: A Perfect Storm of Financial Pressures

Parameter

2022

2023 (Projected)

Average Milk Price (per liter)

€0.37

€0.34

Total Milk Production (million liters)

8,000

7,800

Input Costs Increase (%)

15%

10%

Weather Impact on Yield

Moderate

Severe

Nitrates Pressures Compliance Cost

€50 million

€60 million

Rising input costs are a significant burden on Irish dairy farmers. The feed cost has surged due to global supply chain disruptions and local shortages. Similarly, fertilizer prices have increased due to high demand and supply constraints. Additionally, fluctuating oil and gas prices have caused energy costs to soar, impacting transportation and machinery expenses. Rising labor costs, influenced by higher minimum wages and labor shortages, add further financial pressure.

These escalating costs erode farmers’ slim margins, resulting in severe cash flow difficulties. Increased spending on essential inputs leaves farmers less financial flexibility for operational needs or investments in sustainability. Moreover, adverse weather conditions and strict nitrates regulations further strain their finances, threatening the viability of dairy farming in Ireland.

A Clarion Call for Financial Sustainability: Irish Dairy Farmers Advocate for Essential Base Milk Price Increase

Irish dairy farmers are demanding an increase in the base milk price to at least 45 cents per liter, as the Irish Creamery Milk Suppliers Association (ICMSA) advocates. This increase is essential for several reasons. Rising input costs, volatile weather, and strict nitrates regulations have tightened farmers’ margins. Without a price hike, many face unsustainable cashflows and further declines in milk production.

The call is more than a temporary plea; it’s crucial for restoring confidence in the sector. A higher base price would boost cash flow, allowing farmers to invest in resources and cover expenses adequately. Improved margins would help farmers withstand market pressures, ensuring a stable milk supply and fostering long-term growth and sustainability.

Increasing the base milk price also benefits the broader dairy market. Returning the value realized from market improvements—such as the recent 1.7% rise in the Global Dairy Trade and the 1.1 cents per liter increase in the Ornua Purchase Price Index—to farmers, the entire supply chain gains. Enhanced farmer profitability strengthens rural economies and the dairy supply chain, benefiting processors, retailers, and consumers. Thus, increasing the base milk price is vital for fortifying Ireland’s dairy sector.

Complexities and Constraints: The Role of Milk Processors in Pricing Dynamics

Month

Global Dairy Trade Index (GDT)

Ornua Purchase Price Index (PPI)

January

1,080

108.9

February

1,085

109.5

March

1,090

110.1

April

1,095

110.7

May

1,080

108.4

June

1,075

107.8

Milk processors influence milk pricing by acting as intermediaries between dairy farmers and the market. They determine the base milk price, factoring in global market trends, domestic supply, and costs. Their pricing decisions significantly impact farmers’ incomes.

Setting prices involves balancing market conditions indicated by the Global Dairy Trade (GDT) and the Ornua Purchase Price Index (PPI). The PPI recently showed a slight increase, reflecting a modest improvement. However, these gains do not always lead to higher payouts for farmers, as processors face financial pressures, including processing and distribution costs.

The Irish Creamery Milk Suppliers Association (ICMSA) has called for a milk price of 45c/L to restore confidence in the sector, stressing the tension between farmers’ needs and processors’ financial stability.

Although the Ornua PPI indicated an increase to 39.6c/L for May, this falls short of what farmers need. Processors argue that price increases must be sustainable in the market context and reflect real improvements in dairy product prices.

Based on transparent market understanding, practical changes in milk pricing require coordinated efforts between farmers and processors.

The Ripple Effect of Higher Milk Prices: Balancing Immediate Relief with Long-Term Market Dynamics

Increasing milk prices would offer immediate relief to dairy farmers, stabilizing cash flows and covering rising input costs. This support is crucial for maintaining production levels and preventing further declines in milk volumes.

However, higher prices may reduce consumer demand for dairy products, as price-sensitive consumers might turn to cheaper alternatives. This could cause an initial oversupply, impacting processors and retailers.

Higher milk prices encourage farmers to invest in advanced production technologies long-term, boosting efficiency and output. Consistent pricing could also attract new entrants, strengthening the supply base.

Internationally, Ireland’s dairy competitiveness could be affected. Higher costs might make Irish products less competitive. Still, improved quality and supply could capture niche markets willing to pay premium prices.

In conclusion, while a price increase is crucial for farmers, its broader impacts on supply, demand, and global market positioning must be carefully managed for long-term sustainability.

The Bottom Line

The Irish dairy sector faces several challenges, including declining milk production and stagnant prices, compounded by rising costs and environmental pressures. A key issue is the gap between what farmers earn for their milk and the increasing costs they face. It’s crucial for processors to fairly distribute market gains back to farmers to ease cash flow pressures faced by dairy producers.

Increasing the base milk price to at least 45c/L, as suggested by the Irish Creamery Milk Suppliers Association (ICMSA), is essential to restore confidence among producers. Transparency and timely price adjustments by milk processors, in line with market trends like those shown by the Ornua Purchase Price Index (PPI) and Global Dairy Trade (GDT), are also critical.

Tackling these issues calls for collaboration among processors, associations, and policymakers to support farmers. This would provide immediate financial relief and ensure the dairy industry’s resilient and prosperous future.

Key Takeaways:

Financial Strain: Irish dairy farmers are under considerable financial strain due to declining milk prices and rising input costs.

Production Decline: There is a tangible decline in milk production, impacting the overall market and supply chain.

Advocacy for Fair Pricing: Industry bodies like the Irish Farmers Association and the Irish Creamery Milk Suppliers Association are advocating for a base milk price increase to support farmers.

Regulatory Pressures: Stringent nitrate regulations and unpredictable weather patterns add to the challenges faced by dairy farmers.

Call for Sustainable Practices: Ensuring financial sustainability through fair pricing can enable farmers to invest in better resources and practices, ultimately benefiting the broader agricultural sector.

Summary: Irish dairy farmers are grappling with financial pressures and unpredictable markets, resulting in dwindling margins and decreased production. The dairy industry, a vital part of Ireland’s economy, supports rural livelihoods and contributes significantly to the national economy through exports and jobs. Organizations like the Irish Farmers Association and the Irish Creamery Milk Suppliers Association are advocating for fair milk prices to restore sector confidence. High input costs and adverse weather conditions further exacerbate the situation, with milk volumes lagging behind 2023 levels. Stringent nitrate regulations and unpredictable weather patterns exacerbate the situation. To restore confidence, the dairy sector is advocating for an increase in the base milk price to at least 45 cents per liter. This would boost cash flow, enable farmers to invest in resources, and ensure stable milk supply. The broader dairy market benefits from increased farmer profitability, strengthening rural economies and the dairy supply chain. However, the broader impacts on supply, demand, and global market positioning must be carefully managed for long-term sustainability.

Find out why cheese prices are climbing. Learn how milk market issues and local disruptions are affecting your favorite dairy products. Get the details here.

Another day of positive growth in the cheese market. Higher CME spot prices have led to a significant increase in block values, reaching the highest level since August 2023. With futures finishing 6.4 cents higher at $2.1390 a pound, it has driven the August all-cheese price to fresh life-of-contract highs. While milk output is a concern in certain cheese-making areas, the overall market is showing promising signs.

Commodity

Current Price

Change

Highest Price Since

Block Cheese

$2.1390 per pound

+6.4 cents

August 2023

Spot Blocks

$1.9825 per pound

+$0.0450

–

Barrel Cheese

$2.0225 per pound

+$0.0125

–

Butter

$3.0900 per pound

-$0.0150

–

Leading Chicago’s dairy market activity today:

With four shipments sold, spot blocks increased to $1.9825 per pound, gaining $0.0450.

Barrels likewise rose to $2.0225 per pound, earning $0.0125.

The lone red on the board was butter, which slid to $3.0900, down $0.0150.

Stability in the dairy market is evident as Class III futures improved, with contracts for third quarters concluding at $21.28 per hundredweight, up $0.45 for the day. Simultaneously, adjacent Class IV contracts remained steady at $21.35, indicating a balanced market.

Though steady from last week, Midwest spot milk prices this week averaged—$1.50, significantly above last year’s price of—$7.75 and the five-year average of—$2.73. Cow comfort still presents difficulties in many areas of the United States, resulting in limited supply.

Summary: The cheese market has seen positive growth, with higher CME spot prices leading to a significant increase in block values, reaching the highest level since August 2023. Futures finished 6.4 cents higher at $2.1390 a pound, driving the August all-cheese price to fresh life-of-contract highs. Despite concerns about milk output in certain cheese-making areas, the overall market is showing promising signs. Chicago’s dairy market activity saw spot blocks increase to $1.9825 per pound and barrels to $2.0225 per pound. Class III futures improved, with contracts for third quarters ending at $21.28 per hundredweight, up $0.45. Midwest spot milk prices averaged $1.50, significantly above last year’s price and the five-year average of $2.73.

Learn how milk futures suggest better prices ahead despite market volatility and rising demand. Will tighter supplies and more exports lift dairy markets?

Understanding the market dynamics, especially the recent trends in Class III futures, is crucial. It can equip you with the knowledge to navigate through these uncertain waters. Stay informed and be prepared for fluctuations that could significantly impact your bottom line.

Month

Class III Futures Price ($ per cwt)

Class IV Futures Price ($ per cwt)

January

21.35

23.50

February

22.10

24.30

March

20.85

23.00

April

19.60

22.10

May

18.50

21.00

June

19.20

22.40

Milk Futures Signal a Brighter Horizon for Dairy Farmers

The potential for a brighter horizon for dairy farmers this year is signaled by milk futures. If spot prices hold, milk prices could surpass last year’s levels. This optimistic outlook is driven by several factors, including increased demand and supply constraints, which could further boost prices.

Firstly, increased demand plays a significant role. Both domestic and international markets show a heightened appetite for dairy products, especially cheese and butterfat.

Secondly, supply constraints could further boost prices. Cheese inventories haven’t exceeded last year’s levels. If demand continues to rise, the supply may struggle to keep pace, pushing prices upward.

It’s also worth noting that volatility in recent milk markets could become more pronounced as summer progresses. The indicators point positively toward better milk prices compared to last year.

Month

Cheese Exports (Metric Tons)

Butterfat Exports (Metric Tons)

January

24,000

6,500

February

22,500

6,200

March

26,000

6,800

April

28,500

8,000

May

27,000

7,500

The Stability in Cheese Inventory: A Beacon for Dairy Farmers

The stability in cheese inventory signals good news for dairy farmers. With international demand rising, especially in quicker-rebounding markets, you can expect further price gains. High cheese exports will likely continue, cushioning against domestic shortages.

Butterfat exports surged 23% in April, hinting at record butter prices. If domestic consumption follows suit, the dairy sector could have a profitable year. Watch these trends closely as they shape market dynamics.

The crop outlook remains strong despite planting delays. With 75% of corn rated good/excellent, a bountiful harvest is expected. This could lower feed costs and boost profits. While some input costs are high, stable grain prices and improving milk futures suggest a better income over feed margin.

As summer progresses, a proactive approach is essential. The market’s volatility demands your attention. Monitor both local and international trends to navigate the ups and downs, maximizing gains and minimizing setbacks.

Record Cheese Exports: A Promising Outlook for Dairy Farmers

International cheese demand has surged, with record-high cheese exports in March and April. This increase has provided strong market support. More domestic cheese is being sold internationally, reducing inventory levels and potentially tightening supplies.

The impact on future prices could be significant. Continued strong demand and tighter supplies may boost cheese prices. As global market dynamics favor U.S. cheese, this could mean better margins and a more stable income for dairy farmers.

The Butter Market: Rising Exports Foreshadow Potential Records

The butter market is showing robust signs. In particular, April witnessed a substantial increase in butterfat exports, soaring by 23%. This upward trend in exports is not just a fleeting moment; it sets a solid foundation for potentially record-high butter prices this year. As both domestic and international demand for butter continues to rise, the market outlook becomes increasingly favorable. This spike in demand, coupled with the surge in butterfat shipments, could very well propel butter prices to new heights, instilling confidence in dairy farmers about the market’s potential.

April’s Income Over Feed Margin: A Glimpse of Dairy Farming Resilience

April’s income over feed price was $9.60 per cwt, marking the second month without Dairy Margin Coverage payments. This positive signal for dairy farmers shows profitable conditions without government support.

Looking ahead, the stability of grain prices and the positive trend in milk futures should inspire optimism. Despite planting delays, grain prices remain steady, and 75% of the corn crop is rated good to excellent. A strong crop could mean lower grain prices and feed costs, potentially boosting income over feed margins and improving profitability. This promising outlook could reduce reliance on Dairy Margin Coverage payments, offering a brighter future for dairy farmers.

With steady or falling grain prices and positive milk futures, dairy farmers might see continued profitability, reducing reliance on Dairy Margin Coverage payments. This outlook benefits farmers navigating market volatility.

Grain Market Conditions: A Silver Lining for Dairy Farmers

Let’s shift focus to the grain market. Planting delays have yet to affect grain prices significantly. The early corn condition looks very positive, with 75% rated as good to excellent. That sets the stage for a robust harvest.

If this trend holds, expect a large corn crop, likely lowering corn prices. This means reduced feed costs for dairy farmers, leading to better income over feed margins and improved profitability despite volatile milk market conditions.

The Bottom Line

The dairy market is experiencing significant volatility, especially in Class III futures. However, current trends suggest milk prices could improve. Cheese inventory is stable, hinting at tighter supplies if demand rises. Meanwhile, cheese and butterfat exports have surged, boosting market confidence.

In April, income over feed margins was resilient, with stable grain prices suggesting favorable conditions for dairy farmers. Despite some planting delays, strong crop conditions for corn indicate ample supply and potentially lower feed costs. These factors contribute to a positive milk price outlook if spot prices hold and demand grows.

Key Takeaways:

Milk futures suggest better prices compared to last year if current spot prices hold.

Demand dynamics: Improved international cheese demand boosts market optimism.

April saw a 23% increase in butterfat exports, hinting at possible record-high butter prices.

Grain market: Initial crop conditions are favorable, potentially leading to lower grain prices.

No further Dairy Margin Coverage program payments expected due to improved income over feed conditions.

Summary: The dairy market is experiencing significant volatility, especially in Class III futures, and this turbulence is expected to persist and escalate as summer approaches. Milk futures indicate a brighter horizon for dairy farmers this year, with spot prices holding and milk prices potentially surpassing last year’s levels. Increased demand for dairy products, particularly cheese and butterfat, is driving optimism. Supply constraints could further boost prices, as cheese inventories haven’t exceeded last year’s levels. Stability in cheese inventory signals good news for dairy farmers, as international demand is rising, especially in quicker-rebounding markets. High cheese exports will likely continue, cushioning against domestic shortages. The butter market is showing robust signs, with record-high cheese exports in March and April providing strong market support. More domestic cheese is being sold internationally, reducing inventory levels and potentially tightening supplies.

Uncover the surge of bullish trends on LaSalle Street pushing Class III & IV futures to record highs. Will the dairy markets keep climbing? Delve into the latest insights today.

The bulls are back on LaSalle Street, setting fresh records in dairy futures. Class III and some Class IV futures hit life-of-contract highs this week, making waves in the dairy markets. While some Class III contracts dipped slightly by week’s end, Class IV futures rose about 30ȼ. Third-quarter Class III stands solidly above $20 per cwt. Fourth-quarter contracts hover in the high $19s. Class IV futures are robust in the $21s and $22s.

Prices climbed across the CME spot market, led by whey – the unsung hero of the Class III complex.

The recent surge in whey powder, with a significant 13.25% increase, along with solid gains in Cheddar blocks and barrels, is a clear indicator of the market’s strength. This bullish trend in Class III and IV futures not only highlights the current market strength but also promises potential growth and stability.

Product

Avg Price

Qty Traded

4 Wk Trend

Whey

$0.4445

7

13.25% increase

Cheese Blocks

$1.8660

13

Up

Cheese Barrels

$1.9550

13

Up

Butter

$3.1040

5

Stable

Non-Fat Dry Milk (NDM)

$1.1895

31

Up

Class III Futures Soar: A Promising Summer and Year-End Forecast

Contract

Price as of Last Week

Price This Week

Change

July Class III

$19.50

$20.25

+3.85%

August Class III

$19.75

$20.45

+3.54%

September Class III

$20.00

$21.10

+5.50%

October Class III

$19.20

$20.10

+4.69%

November Class III

$19.00

$19.75

+3.95%

December Class III

$18.50

$19.40

+4.86%

The steady trend of class III futures, which are on a roll this summer and heading into the end of the year, offers a clear outlook for dairy producers. With contracts from July through December hitting life-of-contract highs and third-quarter Class III prices solidly above $20 per cwt., there is robust demand in the market. The prices for the fourth quarter, settling in the $19s, further reinforce the potential profitability for dairy producers.

Class IV Futures Climb Higher: Butter and NDM Lead the Charge

Month

Avg Price

Qty Traded

4 wk Trend

July 2024

$21.50

10

⬆

August 2024

$21.75

12

⬆

September 2024

$22.00

14

⬆

October 2024

$21.95

11

⬆

November 2024

$22.10

13

⬆

December 2024

$22.25

15

⬆

Class IV futures are on the rise, now solidly in the $21s and $22s. This reflects the strong and resilient market fundamentals of the dairy sector. The hike in Class IV prices highlights robust demand for butter and nonfat dry milk (NDM), both showing remarkable performances recently. With higher butter output meeting strong demand and climbing NDM prices, these components are crucial to Class IV’s upward trend. This surge boosts market sentiment and provides dairy producers with better financial incentives to increase production despite current challenges, instilling a sense of stability and confidence in the market.

A Week of Robust Gains: Whey Leads the Charge in the CME Spot Market

The CME spot market buzzed this week, with significant gains led by whey. Spot whey powder jumped 5.5ȼ, a solid 13.25% increase, hitting 47ȼ per pound for the first time since February. This rise shows the strong demand for high-protein whey products as manufacturers focused more on concentration.

Spot Cheddar also saw gains, with blocks up 3.5ȼ to $1.845 per pound and barrels rising 1.5ȼ to $1.955 per pound. This climb, even with a drop in Cheddar production, reflects strong domestic and international cheese demand, especially with U.S. cheese exports to Mexico hitting record highs.

Nonfat dry milk (NDM) increased by 2.75ȼ to $1.195 per pound, supported by a robust Global Dairy Trade auction. Despite the price rise, NDM stocks saw their most significant March-to-April jump, suggesting slower exports.

Butter prices edged slightly, by a fraction of a cent, to settle at $3.0925 per pound. Despite a 5.3% year-over-year production increase, the continued strength in butter prices indicates strong demand holding up the market prices.

April’s Milk Output: High Components Drive Record-Breaking Butter Production

Month

Butter Production (million pounds)

Year-Over-Year Change (%)

January

191.0

+4.0%

February

181.3

+3.5%

March

205.5

+5.1%

April

208.0

+5.3%

The bulls are back in charge on LaSalle Street. July through December Class III and a smattering of Class IV futures notched life-of-contract highs this week. While most Class III contracts ultimately settled a little lower than they did last Friday, Class

April’s milk output brought some notable developments. Despite lower overall volume than last year, higher milk components led to an uptick in cheese and butter production. Manufacturers churned out nearly 208 million pounds of butter, a 5.3% increase over April 2023. This marks the highest butter output for April, only behind April 2020, when pandemic shutdowns diverted cream to butter production. This spike in butter output indicates solid market demand despite the large volumes.

Record Cheese Production in April: Mozzarella and Italian-Style Cheeses Shine

Cheese Type

April 2023 Production (Million lbs)

April 2024 Production (Million lbs)

Year-over-Year Change (%)

Mozzarella

379

402

+6.2%

Italian-Style

496

527

+6.2%

Cheddar

349

319

-8.6%

Total Cheese

1,170

1,191

+1.8%

April saw U.S. cheese production reach new heights, with Mozzarella and Italian-style cheeses leading the charge. Mozzarella production hit record levels, and Italian-style cheese output was up 6.2% compared to last April. This high demand ensures quick consumption or export, avoiding the stockpiles that sometimes affect Cheddar.

Cheddar, however, experienced an 8.6% drop in production from last year, showing a 5.9% decline from January to April compared to 2023. Yet, strong cheese exports, especially to Mexico and key Asian markets, are balancing things out. Exports are up 23% year-to-date, which helped push cheese prices above $2 briefly.

Continued export growth might be challenging, with cheese prices around $1.90, but the trends are promising for U.S. cheese producers.

Whey Powder Renaissance: Demand for High-Protein Products Fuels Price Surge

Whey powder, often underrated in the dairy market, is returning thanks to a strong demand for high-protein products. Health-conscious consumers are driving this trend, leading manufacturers to concentrate more on whey and produce less powder. Although April’s whey powder output matched last year’s, stocks have declined. This reduced supply and steady demand have fueled the current price surge. The recent 5.5ȼ gain, a 13.25% increase, underscores the market’s strength.

A Tale of Supply and Demand: NDM Production Slumps While Stockpiles Surge Due to Sluggish Exports

Nonfat Dry Milk (NDM) and Skim Milk Powder (SMP) production fell significantly in April to 209.6 million pounds, down 14.2% year-over-year, marking the lowest April output since 2013. Despite this, NDM stocks surged, hitting a record March-to-April increase. Slower exports are the leading cause. In April, the U.S. exported 144 million pounds of NDM and SMP, down 2.5% from last year and the lowest for April since 2019. This highlights the delicate balance between production, stock levels, and international trade.

Promising Prospects: Mexico’s Shift to NDM Could Boost Exports and Stabilize Markets

There’s hope for increased NDM export volumes, particularly to Mexico. Higher cheese prices might push Mexico to import more affordable NDM instead of cheese. Mexican manufacturers can use NDM to boost their cheese production efficiently. This shift could reduce current NDM stockpiles and stabilize market prices.

Proceed with Caution: Navigating Volatility and Barriers in Milk Production

The recent data highlight extreme volatility in the dairy complex. While high prices are tempting, caution is crucial. There are significant barriers to milk production expansion. High interest rates make investments riskier, and a scarcity of heifers limits rapid growth. Even issues like the bird flu impact the supply chain and market stability.

Economic Incentives and Strategic Tools Empower Dairy Producers to Boost Output and strategically navigate the market. This potential for strategic growth and control over the market dynamics can be a powerful motivator for dairy producers and traders. The current market conditions for dairy producers are a strong incentive to boost milk production. Class III futures are up $3.50 from last year, and with corn prices down $1.55, feed costs are more affordable, making it easier to increase output.

Despite market ups and downs, there’s a great chance to protect your margins. You can lock in current high prices using futures and options, ensuring steady profits. The Dairy Revenue Protection (DRP) insurance program offers a safety net against price drops or production issues. These tools help you navigate the market smartly and aim for maximum profitability.

The feed markets had their ups and downs this week but ended up close to where they started. July corn settled at $4.4875, a slight increase of 2.5ȼ. Meanwhile, July soybean meal dropped $4.10 to $360.60 per ton.

Farmers are almost done planting their crops, with just a few acres left. A drier forecast will help them wrap up. Although heavy spring rains posed initial challenges, they also improved moisture reserves for the upcoming summer months.

Less favorable global farming conditions might boost U.S. export prospects, stabilizing prices and preventing steep drops. With average weather, a large U.S. harvest is expected, potentially lowering feed costs even more.

The Bottom Line

The current dairy market offers both opportunities and challenges for producers. Class III and IV futures show solid gains and higher prices thanks to robust demand and reduced milk output. Whey and cheese markets are performing exceptionally, and export volumes could improve. However, volatility remains a concern. High interest rates, scarce resources, and global health threats add to the uncertainty. Farmers can secure attractive margins using strategic tools like futures, options, and insurance programs. Favorable planting conditions and resilient feed markets provide added support. Staying informed and agile will be vital to capitalizing on these dynamics while managing risks.

Key Takeaways:

Strong bullish trends observed in Class III and IV futures, with significant life-of-contract highs.

Third-quarter Class III prices solidly above $20 per cwt, and fourth-quarter contracts in the $19 range.

Class IV futures robustly in the $21s and $22s, driven by high demand for butter and NDM.

Whey powder prices surged with a 13.25% gain, hitting 47ȼ per pound for the first time since February.

Cheddar blocks and barrels showed solid gains at the CME spot market, indicating strong market fundamentals.

April’s milk output featured high components, leading to record-breaking butter production.

U.S. cheese production hit record levels in April, driven by escalating Mozzarella and Italian-style cheese output.

Strong demand for high-protein whey products spurred a price surge, backed by decreased dryer availability.

NDM production saw a slump, affected by sluggish exports, but stockpiles surged with the largest March-to-April increase ever.

Mexico’s potential shift to importing more NDM could stabilize export volumes and market dynamics.

Dairy producers incentivized to boost milk production despite barriers, with improved futures and feed margins.

Feed markets exhibited resilience, with minor fluctuations in corn and soybean meal prices.

Summary: The dairy market has seen a strong bullish trend, with Class III and some Class IV futures hitting life-of-contract highs this week. Class IV futures are robust in the $21s and $22s, reflecting the strong and resilient market fundamentals of the dairy sector. The recent surge in whey powder and solid gains in Cheddar blocks and barrels is a clear indicator of the market’s strength, promising potential growth and stability. Class III futures are on a roll this summer and heading into the end of the year, offering a clear outlook for dairy producers. Contracts from July through December hit life-of-contract highs, and third-quarter Class III prices solidly above $20 per cwt., reinforcing potential profitability for dairy producers. Class IV futures are on the rise, now solidly in the $21s and $22s, reflecting the strong and resilient market fundamentals of the dairy sector. The surge in Class IV prices highlights robust demand for butter and nonfat dry milk (NDM), both showing remarkable performances recently. In April, U.S. cheese production reached record levels, with Mozzarella and Italian-style cheeses leading the charge.

Uncover how surging milk prices and decreased feed costs are enhancing dairy profitability. Interested in the freshest trends in milk production and inventory? Dive in to learn more now.

The dairy market witnessed a significant upturn in May, attributed to the rise in milk prices and the decrease in feed costs. This has led to a boost in profitability for dairy producers. Despite milk production still trailing behind last year, the gap is gradually closing, indicating a path to recovery. The USDA’s latest reports, being a reliable source, provide crucial insights that can potentially shape the dairy market.

Dairy margins improved in late May.

Milk production dropped 0.4% from last year, the smallest decline in 2023.

Weaker feed markets lowered costs.

These factors are setting the stage for improved profitability. Farmers, demonstrating their adaptability, are strategically extending coverage in deferred marketing periods to maximize these gains. Grasping these changes is of utmost importance in navigating the evolving dairy margin landscape.

Riding the Wave: Dairy Margins Climb on the Back of Market Dynamics

Dairy margins have experienced notable improvements, especially towards the end of May. Apart from the spot period in Q2, ongoing rallies in milk prices coupled with declines in feed market costs have significantly bolstered profitability for dairy producers. This positive shift in margins can be traced back to several market dynamics that have unfolded over the past month.

Steadying the Ship: Signs of Stability in Milk Production Trends

Month

Milk Production (billion pounds)

Year-over-Year Change (%)

Dairy Herd Size (million head)

February 2023

17.925

-0.8

9.36

March 2023

18.945

-0.7

9.35

April 2023

19.135

-0.4

9.34

March 2023 (Revised)

18.945

-0.7

9.36

April 2024

19.135

-0.4

9.34

Milk production trends show a continued year-over-year decline, but the gap is narrowing, hinting at stability. The USDA’s April report recorded 19.135 billion pounds of milk, a slight 0.4% drop from last year. This is the smallest decline in 2024, indicating that production levels may stabilize.

The USDA also revised March data, showing a 0.7% decrease compared to the reported 1.0%. This revision suggests that the production landscape might be improving. While still below last year’s levels, these updates point to a possible upward trend.

Adapting to Market Pressures: Implications of the Changing U.S. Dairy Herd

The dynamics of the U.S. dairy herd tell of broader milk production trends and market conditions. The USDA reported a reduction from 9.348 million dairy cows in March to 9.34 million in April, marking an 8,000-head decline. Year-over-year, the herd is down by 74,000 cows.

These figures underscore a contraction in the dairy herd, a crucial aspect for comprehending market dynamics. A revision of March’s data revealed the herd was more significant than initially reported, indicating dairy producers are adapting to market pressures for sustainability and profitability.

Contrasting Fortunes: Dramatic Spike in Butter Stocks versus Modest Cheese Inventory Growth

Product

April 2023 (lbs)

March 2024 (lbs)

April 2024 (lbs)

Change from March to April 2024 (lbs)

Change from March to April 2024 (%)

Butter

331.7 million

317.3 million

361.3 million

44 million

13.9%

Cheese

1.47 billion

1.45 billion

1.46 billion

5.6 million

0.4%

According to the USDA’s April Cold Storage report, butter inventories notably increased. As of April 30, there were 361.3 million pounds of butter in storage, up 44 million pounds from March – the most significant jump since the pandemic. This rise indicates strong domestic production outpacing demand, with stocks now up 9% from last year, highlighting consistent growth in 2024.

Conversely, the cheese market experienced milder growth. Cheese stocks rose by only 5.6 million pounds from March to April, totaling 1.46 billion pounds by the end of April, down 0.6% from last year. This limited increase is mainly due to a surge in cheese exports this spring. However, with U.S. cheese prices losing global competitiveness, these exports may slow down, potentially changing this trend.

Export Dynamics: The Balancing Act of U.S. Cheese Inventory

Year

Cheese Exports

Price Competitiveness

Key Markets

2020

800 million lbs

High

Mexico, South Korea, Japan

2021

850 million lbs

Moderate

Mexico, South Korea, Canada

2022

900 million lbs

High

Mexico, China, Japan

2023

950 million lbs

Moderate

Mexico, South Korea, Australia

2024

500 million lbs (estimated)

Low

Mexico, South Korea, Japan

Cheese exports have significantly influenced U.S. cheese inventories this spring. Increased exports have helped manage domestic cheese stocks despite high production levels. However, with U.S. cheese prices losing their competitive edge onthe global market, exports will likely slow. This may result in growing domestic cheese stocks, presenting new challenges for inventory management.

Looking Ahead: Promising Outlook for Dairy Margins

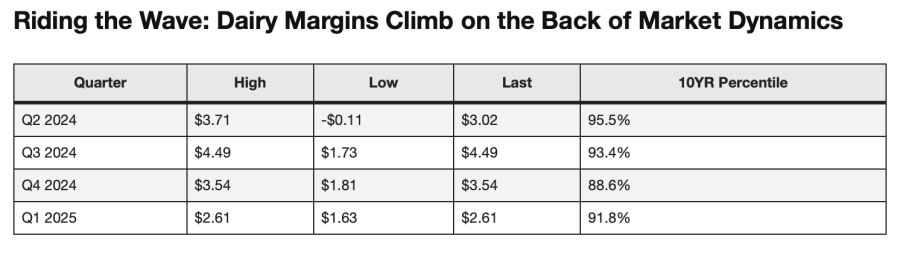

Looking ahead, dairy margins show promise. In Q2 2024, margins ranged from -$0.11 to a high of $3.71, with the latest at $3.02, in the 95.5th percentile over the past decade. This is a solid historical position. For Q3 2024, margins vary from $1.73 to $4.49, currently at the high end of $4.49, in the 93.4th percentile. This suggests continued profitability. Q4 2024 sees more variability, with margins from $1.81 to $3.54, currently at $3.54, in the 88.6th percentile. Lastly, Q1 2025 shows a slight dip with margins from $1.63 to $2.61, but still favorable at the 91.8th percentile. These figures depict an optimistic outlook for dairy margins in the coming quarters, driven by solid milk prices and stable feed costs.

The Bottom Line

Due to rising milk prices and weakening feed markets, recent market dynamics have boosted dairy margins. Despite a year-over-year drop in milk production, USDA data revisions show smaller declines and changes in dairy herd numbers. Butter and cheese inventory trends emphasize the importance of diligent market monitoring.

Understanding these margins and staying informed is crucial for dairy producers. Fluctuations in butter and cheese stocks highlight the industry’s ever-changing landscape. Extending coverage in deferred marketing periods can offer strategic advantages.

Stay ahead by monitoring industry reports like the CIH Margin Watch report. For more information, visit www.cihmarginwatch.com. Adapting to market changes is critical to sustaining profitability in the dairy industry.

Key Takeaways:

Improved Dairy Margins: Late May witnessed a significant rise in dairy margins as milk prices rallied and feed costs dropped.

Milk Production Trends: Though milk production is still down compared to last year, the rate of decline is slowing, signaling a move towards stability.

USDA Reports: April figures showed a smaller-than-expected decrease in milk production and larger inventories of butter, while cheese inventories grew at a slower pace.

Future Margins: Projections show promising dairy margins through the end of 2024 and into early 2025, suggesting sustained profitability for dairy farmers.