50% of U.S. dairies have vanished since 2013. Will yours survive the next bloodbath? The math doesn’t care about tradition – adapt or die.

EXECUTIVE SUMMARY: The U.S. dairy industry’s consolidation is accelerating, with half of all farms disappearing since 2013 and another 50% projected to vanish by 2035. Survival hinges on scaling to 1,000+ cows or pivoting to niche markets like organic/grass-fed production while leveraging cost-slashing techs like robotics and genomics. Mega-dairies now dominate 70% of milk output, leaving smaller farms battling volatile prices and 34% higher feed costs. Brutal economics favor radical growth or hyper-specialization, with collaboration and tech adoption becoming non-negotiable. The clock is ticking farms must choose their path now or join the 4% annual closure rate.

KEY TAKEAWAYS:

Consolidation is accelerating: Industry half-life shrunk from 12 to 10 years – 12,000 farms will remain by 2035.

Tech is the great equalizer: Robotics, genomics, and methane digesters separate winners from casualties.

Collaborate or perish: Resource-sharing cooperatives and collective bargaining offset consolidation pressures.

No middle ground: Operators must commit to growth or specialization – hesitation guarantees obsolescence.

The numbers don’t lie: 50% of U.S. dairy farms vanished between 2013 and 2025. If that gut-punch statistic doesn’t rattle you, consider this—the industry’s consolidation “half-life” is accelerating. What took 12 years to cull half our farms now happens in 10. By 2035, only 12,000 dairies will remain. The question isn’t whether consolidation will claim more farms but whose. Are you evolving fast enough to outpace the 4% annual closure rate, crushing your neighbors? Let’s pull no punches: survival demands radical adaptation.

The Great Dairy Shakeout: By the Numbers

Here’s the cold reality:

Milk production surged 25.3 billion pounds since 2013, but 48 states lost dairy farms.

Texas added 195,000 cows while traditional strongholds like California bled operations.

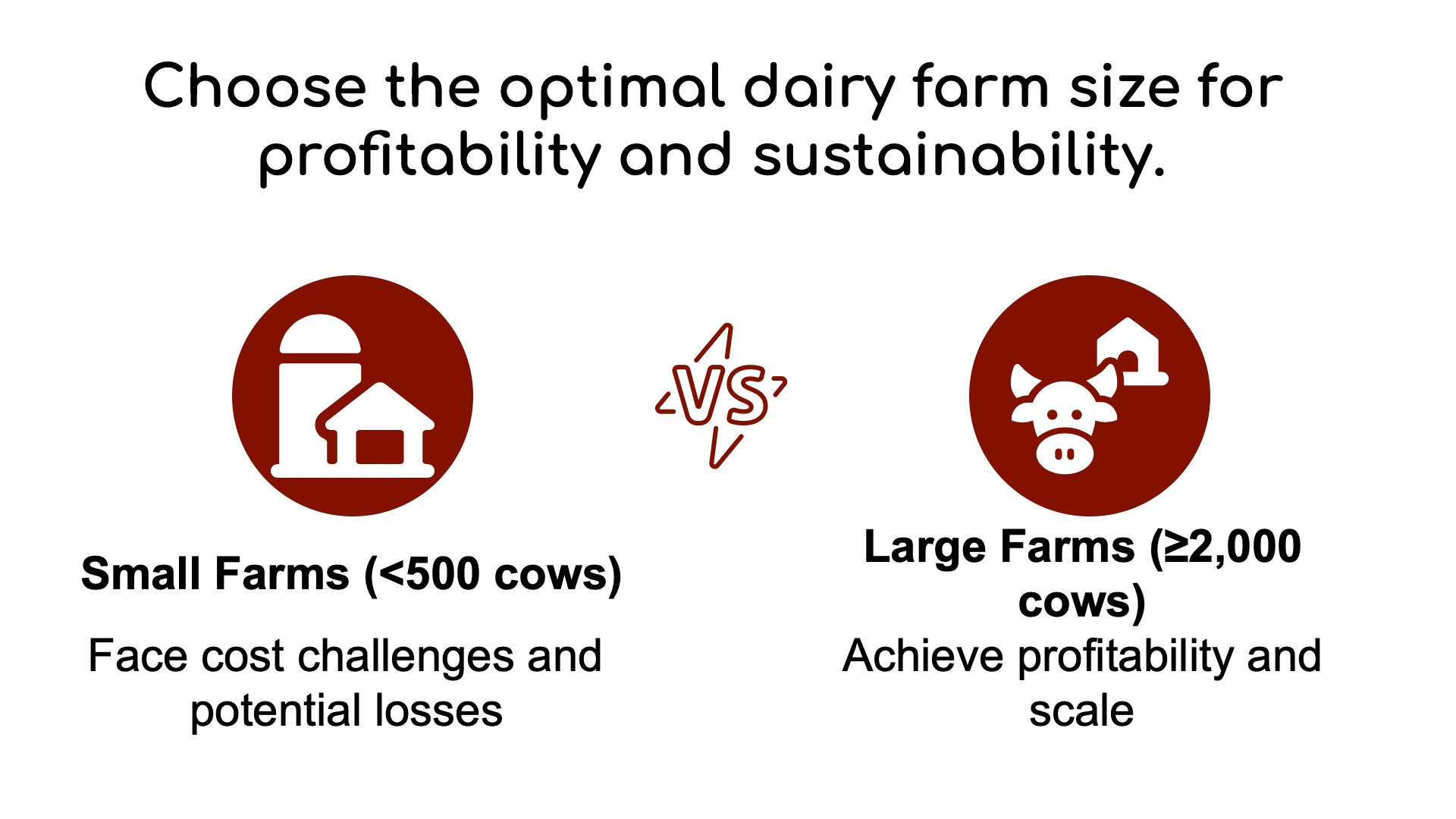

80% of farms milk <500 cows, yet 70% of U.S. milk flows from 1,000+ herd mega-dairies.

This isn’t your grandfather’s industry. The USDA confirms what every farmer feels: scale equals survival. Herds under 500 cows face average costs exceeding milk prices, while 2,000+ cow operations turn profits. Dennis Rodenbaugh, CEO of Dairy Farmers of America (DFA), says, “Anticipating disruption isn’t optional. You build bridges to the future or get washed away”.

Scale or Fail: The New Reality of Milk Production

Forget ‘if’—ask ‘how fast’ you’ll scale. The 1,000-cow threshold isn’t arbitrary. USDA data shows these herds achieve 18% lower production costs than 500-cow operations through bulk purchasing, robotic efficiencies, and negotiating power.

But growth ain’t for the faint-hearted. Rodenbaugh warns, “Get disciplined or get out. The storm separating winners from casualties is accelerating”. Case in point: Midwest families selling out to Panhandle conglomerates where 25,000 cow goliaths churn out milk cheaper than Wisconsin’s pastures ever could.

The Price of Standing Still:

Feed costs up 34% since 2020

Heifer replacement expenses doubling

Milk price volatility swinging ±25% annually

“You’re either acquiring neighbors or becoming acquired,” says a fourth-gen Wisconsin dairyman who tripled his herd to 900 cows. “My kids won’t survive on 300-head nostalgia.”

Beyond Expansion: Alternative Paths Through the Storm

Not everyone can—or should—chase mega-dairy status. For sub-500 herds, niching down beats scaling up:

1. Organic Premium Play

Organic milk fetches $32.69/cwt vs. $21.50 conventional

But tread carefully: transitioning requires 3 years and $150K+ certification costs

2. Grass-Fed Guerrilla Tactics

Direct-to-consumer raw milk sales bypass processors, capturing a 300% markup

Caveat: Regulatory landmines lurk in 38 states

3. Tech-Enabled Micro-Dairies

Robotic milkers slashed labor by 40% for a 150-cow Vermont operation

AI breeding algorithms boosted conception rates by 22%

Sarah Lloyd, a Wisconsin dairy advocate, argues: “We’ve romanticized ‘get big or get out.’ Smart-small dairies leveraging tech and margins can outmaneuver dinosaurs”.

The Innovators: Tech Titans Reshaping Dairy

Game-changing tools separating survivors from the bankrupt:

Technology

Cost Range

ROI Timeline

Herd Size Suitability

Automated Feed Systems

$50K–$200K

2–4 years

500+ cows

Methane Digesters

$1M–$5M

5–7 years

1,000+ cows

Genomics Testing

$25/head

Immediate

All sizes

Robotic Milkers

$150K–$250K/unit

3–5 years

100–500 cows

Texas’s 5,000-cow colossus slashed labor costs by 60% via drones monitoring herd health. Meanwhile, Idaho’s 120-cow boutique dairy uses blockchain to trace grass-fed butter to Manhattan chefs at $12/lb.

The Bottom Line: Blood, Sweat, and 4% Annual Decline

Dairy’s Darwinian reckoning won’t pause for sentiment. Here’s your survival checklist:

Crunch your half-life math: If scaling to 1,000+ cows seems impossible, pivot to hyper-specialization now.

Embrace ‘coopetition’: Pool resources with neighbors for bulk inputs, tech sharing, and collective bargaining.

Bet on genomics: Top 1% genetics can boost yields 2,000+ lbs/cow annually.

Rodenbaugh’s final word? “The dairy game isn’t dying—it’s evolving. Future winners think in decades, not seasons”.

Your move. Will you be among the 12,000 left in 2035—or a statistic in The Bullvine’s following obituary for America’s heartland?

Dairy Product Alternatives: What is the Situation? Dive into the impact of plant-based dairy alternatives on traditional milk markets and learn how producers are fighting back to protect their industry.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

While politicians celebrate National Ag Day in DC, 40% of dairy farms have vanished in just five years. The hard truth is that big gets bigger while small disappears.

While bureaucrats and politicians pat themselves on the back during today’s National Ag Day celebrations, dairy farmers across America continue milking cows at 4 AM with little recognition and mounting regulatory burdens. The USDA’s glossy presentations and Capitol Hill photo-ops won’t mention how dairy farm numbers have plummeted while plant-based alternatives receive favorable treatment from regulators and media alike. Today’s National Ag Day events in Washington showcase agriculture’s importance, but The Bullvine asks: Why is dairy consistently treated as agriculture’s problematic stepchild despite being its economic backbone?

QUICK TAKE: NATIONAL AG DAY & DAIRY’S REALITY

The U.S. has lost 95% of dairy farms since 1970 (from 648,000 to 24,470)

Farms with 1,000+ cows (just 8% of farms) produce 68% of America’s milk

Large operations ($10/cwt cost advantage) are the only growing segment

Despite losing 40% of farms since 2017, milk production increased 5%

The Inconvenient Truth About National Ag Day Celebrations

National Ag Day, celebrated today during National Agriculture Week, was designed to recognize the contributions of all agricultural sectors. But let’s be honest about what’s happening. While officials gather in climate-controlled conference rooms in Washington DC, America’s dairy farmers face an increasingly hostile regulatory environment that threatens their existence.

The Agriculture Council of America hosts today’s main events: a morning virtual livestream from the USDA, an in-person celebration at the USDA Whitten Patio from 8:30-10:30 AM featuring the standard parade of officials, and an evening reception at the Russell Senate Office building. But how many of these events will directly address the challenges squeezing dairy producers nationwide? How many dairy farmers can afford to leave their operations to attend these political theater performances?

The stark reality is that while government officials celebrate agriculture in general, specific policies continue undermining dairy’s position in the American food system. The most alarming evidence is that the U.S. has lost nearly 40% of its dairy farms since 2017, according to the 2022 Census of Agriculture data released by the USDA’s National Agricultural Statistics Service. This represents the largest decline between adjacent Census reports dating back to 1982.

“Even though we’ve lost close to 15,000 dairy farms in five years, the amount of milk that we’re producing in this country has gone up from a similar number of cows,” says Lucas Fuess, dairy analyst with RaboResearch, highlighting the intense consolidation pressure facing the industry.

USDA’s Double Standard: Promoting Plant-Based While Dairy Struggles

The 2025 US Dietary Advisory Committee recommendations that may influence upcoming guidelines propose significant changes that could further challenge the dairy industry. Meanwhile, the Federal Milk Marketing Orders (FMMO) system, established in 1937 to regulate milk pricing based on end use, classifies milk prices by categories: Class 1 (bottled milk), Class 2 (yogurt), Class 3 (cheese), and Class 4 (butter and powdered dry milk).

The USDA ensures the public’s well-being and dietary recommendations are grounded in established, periodically updated science. The agency has also provided labeling guidance for plant-based milk alternatives to help consumers make informed choices. However, these efforts don’t address dairy producers’ fundamental economic challenges.

The Concerning Consolidation of American Dairy

The numbers tell a concerning story about dairy’s future. While nearly 40% of dairy farms disappeared in just five years, milk production increased by 5%. How? Through rapid consolidation. Today, just 2,013 farms with 1,000 or more cows (representing only 8% of all dairy farms) produce approximately 68% of America’s milk, up from 57% in 2017, according to the 2022 Agricultural Census.

This isn’t happening organically. Economic pressures have forced smaller operations to expand or exit the industry. According to the 2022 Agricultural Census, farms with 2,500 or more cows were the only segment that grew during this period, increasing from 714 to 834 farms. Meanwhile, herds of 20-49 cows declined the most on a percentage basis, followed by herds of 50-99 cows.

The economics are stark: According to Fuess, “Farms milking more than 2,000 cows can operate about less per hundredweight than farms with 100-199 cows, with a total cost in 2022 of .06 cwt.” This cost advantage drives the relentless push toward consolidation.

The Regulatory Burden Crushing American Dairy Farms

Today’s National Ag Day celebrations conveniently ignore the crushing regulatory burden dairy producers face. Environmental regulations, labor rules, water usage restrictions, and animal welfare requirements create a complex compliance landscape that disproportionately impacts family-owned dairy operations without the legal teams employed by corporate agriculture.

“Even if they are huge, it doesn’t mean the family is necessarily removed,” Fuess explains. “Instead, it just means that they have a significant employee base or are providing jobs and making a significant impact on their local, and sometimes very rural, communities.”

The Real Story Behind Dairy Farm Numbers

The glossy presentations at today’s National Ag Day events won’t mention the uncomfortable truth: America’s dairy farm decline is accelerating dramatically. In 1970, the United States had more than 648,000 dairy farms. By 2022, just 24,470 remained—a staggering 95% decline. This isn’t just a statistical trend—it represents thousands of multi-generational family businesses disappearing from rural communities.

Agriculture adviser Milton Orr from northeast Tennessee observed, “I remember when we had over 1,000 dairy farms in this county. Now we have less than 40.” Greene County has only 14 dairy farms today, reflecting the nationwide consolidation trend transforming rural America.

What National Ag Day Should Address

If National Ag Day indeed aimed to support all agricultural sectors equally, today’s events would address several critical issues facing dairy producers:

The need for more transparent labeling requirements preventing plant-based products from using dairy terminology

Restoration of whole milk options in school nutrition programs

Streamlined regulatory compliance for small and mid-sized dairy operations

Export support programs specifically targeting dairy products

Research funding for dairy-specific innovation

Instead, today’s celebrations will likely feature generic praise for agriculture without acknowledging the dairy sector’s specific challenges. The USDA and other agencies will tout their commitment to all agricultural sectors while continuing policies undermining dairy’s position in the American food system.

How Dairy Producers Can Fight Back: Actionable Strategies

For dairy producers watching today’s National Ag Day events with justified skepticism, several evidence-based approaches offer the potential for pushing back against the industry’s marginalization:

Optimize component production—Depending on your milk market, Focus on enhancing butterfat content for Class IV utilization (butter, powder) or protein content for Class III utilization (cheese). This strategic approach can maximize returns even in challenging price environments.

Target operational efficiency – With more extensive operations enjoying a $10 per hundredweight cost advantage, small and mid-sized producers must identify operational efficiencies without sacrificing quality or animal welfare.

Build direct consumer relationships – Create direct marketing channels through farm tours, social media presence, and community events that bypass mainstream media narratives about dairy. Research shows consumers are more supportive when they understand production practices.

Engage with policymakers – Rather than assuming officials understand dairy’s challenges, maintain consistent communication with representatives about specific regulatory burdens and their real-world impacts on your operation.

Document your sustainability story – As environmental concerns shape food choices, measure and communicate your operation’s progress in reducing environmental impacts and enhancing sustainability practices.

Participate in industry advocacy – Support organizations fighting for policy changes that level the playing field between dairy and plant-based alternatives. As the Census data shows, individual farms have limited power against structural economic forces.

Explore value-added opportunities – Consider processing capabilities or specialty products that capture more of the consumer dollar rather than remaining solely in commodity production.

Next Steps: Taking Action Today

As National Ag Day unfolds, dairy professionals can take immediate actions to address industry challenges:

Contact your representatives today – Use National Ag Day as an opportunity to call or email your congressional representatives about specific dairy policy concerns

Share your real farm story. Post authentic content about your operation on social media using the #NationalAgDay and #DairyReality hashtags.

Connect with industry advocates—Contact organizations like the American Dairy Coalition or your state dairy association to strengthen collective advocacy efforts.

Evaluate your cost structure – Begin systematically analyzing operational costs to identify areas where efficiency improvements could reduce your cost per hundredweight.

Conclusion: Beyond the National Ag Day Platitudes

As today’s National Ag Day events proceed with their predictable celebrations of American agriculture, dairy producers deserve more than platitudes and photo opportunities. They deserve policies recognizing dairy’s essential role in nutrition and rural economies.

The disconnect between National Ag Day’s celebratory tone and the harsh realities facing dairy producers highlights why The Bullvine continues providing an unfiltered platform for industry perspectives. When government agencies and mainstream agricultural organizations fail to acknowledge dairy’s unique challenges, independent voices become essential for driving meaningful change.

While today’s celebrations may temporarily spotlight agriculture’s contributions, the dairy industry’s future depends on year-round advocacy, challenging policies that undermine its position in the American food system. National Ag Day should represent a starting point for these discussions rather than a one-day acknowledgment before returning to policies that continually marginalize dairy producers.

Proper support for agriculture means supporting all its sectors – including dairy – with policies that enable producers to thrive rather than merely survive. Until National Ag Day celebrations reflect this reality, they remain incomplete acknowledgments of American agriculture’s diversity and challenges.

Key Takeaways

America has lost 95% of its dairy farms since 1970, with the most dramatic decline occurring in recent years, yet milk production continues to rise through dramatic consolidation.

Economics drives the trend: operations with 2,000+ cows produce milk for approximately $10 less per hundredweight than farms with 100-199 cows.

Rather than waiting for policy changes, dairy producers can take immediate action through component optimization, direct marketing, and documenting sustainability progress.

National Ag Day events fail to address dairy’s unique challenges, focusing instead on general agricultural celebrations that ignore the industry’s consolidation crisis.

Effective advocacy requires year-round engagement with policymakers, not just participation in ceremonial agriculture celebrations.

Executive Summary

As National Ag Day unfolds with ceremonial celebrations in Washington DC, America’s dairy farmers face a stark reality hidden behind the platitudes: nearly 40% of dairy operations have disappeared in just five years while milk production increased by 5%. This consolidation crisis isn’t happening by accident—large operations with over 2,000 cows enjoy a $10 per hundredweight cost advantage over mid-sized farms, creating economic pressure rapidly reshaping rural America. Behind the concerning statistics lies a system where just 8% of farms (those with 1,000+ cows) now produce 68% of America’s milk, up from 57% in 2017. Despite this existential threat to traditional dairy farming, National Ag Day events will likely feature generic agricultural praise without addressing dairy’s specific challenges, highlighting the disconnect between celebratory rhetoric and the industry’s harsh economic reality.

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Unpack the surprising rise in fluid milk demand despite falling production. How’s this shift shaping the dairy market? Find out more.

Summary:

Welcome to the ever-evolving dairy world, where fluid milk consumption bucks the trend up against a background of declining production. As we dive into this report, fluid milk is making a solid comeback, outpacing population growth and showing a 1.6% increase in August compared to the previous year. On the other hand, milk production is slipping, marking a curious case for the industry. Export figures tell a success story, too, with over 17% of U.S. milk solids finding international markets for three months straight, a feat not seen since late 2022. The market dynamics are equally fascinating, with a notable rise in butter and cheese prices, even as traditional cheese production growth slows. Engaging with these dynamics, the dairy sector faces dual challenges of meeting rising consumer demands amid tighter production margins, as evident from the 14-month consecutive decline in milk production. This trend could lead to reduced revenues without compensatory high prices, while farmers encounter increased costs, potentially jeopardizing smaller family farms. The effects ripple through the supply chain, pushing innovations and supportive policies to stabilize and boost production in this dynamic landscape. As we delve deeper, here’s what to ponder: Is this a sustainable shift or a fleeting phenomenon?

Key Takeaways:

Fluid milk consumption continues to rise, even as raw milk production declines.

Annual per capita consumption of dairy products like yogurt, butter, and cheese is increasing.

The U.S. dairy industry saw significant export activity, with over 17% of milk solids exported for three consecutive months.

August marked the highest Dairy Margin Coverage margin since 2015, indicating safety-net solid performance.

National Dairy Product Sales Report revealed peak prices for essential dairy products in September 2024.

There is a noticeable divergence in trends between butter production growth and stagnating cheese production.

Federal Order class prices are affected by recent shifts in butter and cheese cash market prices.

Why is fluid milk consumption rising even as milk production declines, creating a curious paradox? Despite a downward trend in raw milk output, consumer demand for fluid milk climbs, challenging and fascinating dairy farmers and industry experts. This dichotomy presents an opportunity for the industry to innovate and strategize effectively, empowering us to make proactive changes. Let’s explore the factors behind this trend and consider how the market can adapt to these evolving dynamics, knowing that strategic adaptations are within our reach.

Year

Total Fluid Milk Consumption (% Change)

Milk Production (% Change)

U.S. Dairy Exports (% of Solids)

Average Milk Price ($/cwt)

2023

+0.7%

-0.8%

16%

$22.20

2024 (Projected)

+1.6%

-0.1%

17%

$23.60

Milk’s Curious Rise: Navigating the Shift in Consumer Trends

Fluid milk consumption has exhibited a significant uptick, with a 1.6% increase in August compared to the previous year, serving as a testament to the changing dynamics in consumer preferences. This surge reflects a broader trend across the dairy sector, where products like yogurt and butter have also witnessed marked consumption growth. However, this rise in fluid milk consumption might also lead to a decrease in the consumption of other dairy products, potentially impacting their production and pricing. Interestingly, these developments occur in the backdrop of a U.S. population growth rate that lags at just 0.57% over the same period. This disparity suggests a heightened per capita consumption of dairy products, indicating either a shift in dietary habits or possibly greater diversity and innovation in dairy offerings to entice more consumers. It’s a scenario that challenges our traditional understanding of market demands, urging the dairy industry to reevaluate its production strategies and consumer engagement.

Export Surge and Waning: A Tale of Peaks and Valleys

The year kicked off with a bang for U.S. dairy exports, showcasing strength not seen in winter months. In January, exports reached the third-highest level for the month, only to be surpassed by February’s record-breaking performance. This surge marked a promising beginning, substantiating the pivotal role of dairy in international trade. However, as swiftly as it surged, the export volumes waned over the next four months, dipping below the 17% mark of U.S. milk solids production exported. This could be due to changes in global demand, trade policies, or even weather conditions affecting production. This ebb and flow illustrates the unpredictable nature of global demand and the intricate balance of maintaining export momentum.

Nonfat dry milk/skim milk powder is central to these export dynamics. As the most significant product category, its influence is substantial. Variations in demand and market trends can significantly impact the broader export figures. Essentially, nonfat dry milk/skim milk powder is a barometer for the U.S. dairy export market, moving the needle with its performance.

While exports present a dynamic landscape, imports tell a different story. They remain a minor feature of the U.S. dairy economy, even when traced across historical data. July and August saw imports running close to 4% of U.S. milk solids production, ranking fifth and sixth highest over more than 15 years. Yet, despite these peaks, imports do not carry the same weight as exports, mainly due to the robust domestic production capabilities. This creates a uniquely American dairy narrative—heavily export-oriented, with imports playing a supplementary, albeit limited, role.

Milking the Dilemma: Navigating the Production Paradox

While the rise in fluid milk consumption is promising, the 14-month consecutive decline in milk production signals a pressing concern for the dairy industry. This prolonged downturn, in which production levels continually fall below the previous year, shows a sector facing substantial challenges. What does this mean for our dairy farmers and the broader market dynamics?

The impact on dairy farmers is direct and tangible. Lower milk production can reduce revenues unless higher milk prices compensate. However, sustained production deficits can cause additional strain, as fixed costs must be spread over fewer pounds of milk. Farmers might find themselves in a tight spot, juggling increased operational costs, feed expenses, and the need to maintain herd health with dwindling outputs. The financial pressure could push some smaller family farms to the brink, prompting consolidation considerations or even exit from the industry.

The ripple effects extend beyond the farms to the entire supply chain. A decrease in the raw milk supply can affect processors, who might face increased milk prices, leading to higher costs for end products. This could trickle down to consumers, who may notice fluctuations in the availability and pricing of dairy products. On a larger scale, such trends could challenge maintaining U.S. dairy’s competitiveness on the global stage, especially if production deficiencies lead to reduced export capabilities.

How should the industry respond to these challenges? Diversification and innovation in farming practices and supportive policies might offer pathways to stabilize and boost production, instilling optimism and forward-thinking. As we navigate this changing landscape, the question remains: How will the collective efforts of producers, processors, and policymakers redefine the future of dairy farming in response to these persistent challenges?

Butter vs. Cheese: The Market Tug-of-War

The current landscape of dairy product production reveals intriguing dynamics that could have significant implications for the market. Cheese production, for instance, has experienced a deceleration in growth. From a robust increase in prior years, it has only increased by a mere 0.2% through August 2024 compared to the same period in 2023. This moderation starkly contrasts the soaring growth rates of 4.6% and 3% observed in the pandemic years of 2021 and 2022. Meanwhile, butter production presents an opposite trajectory. Having slumped during the pandemic, it has rebounded strongly, with a notable 5.3% growth year-to-date.

But how do these antagonistic production trends ripple through the dairy market? At a glance, one might assume that the imbalance in production growth rates could shift consumer behaviors or market demands. Given the limited expansion in supply, stagnant cheese growth would suggest potential price stabilization or even a rise. Conversely, the uptick in butter output might depress prices due to increased availability, particularly if demand does not parallel supply growth.

Moreover, these production shifts highlight the adaptability and priority shifts within the dairy sector. If butter continues to ascend while cheese lags, could we see a strategic pivot among dairy farmers and associated businesses toward a butter-favored production model? Exploring such correlations is vital for stakeholders anticipating future shifts and demands.

Are these trends supply-driven, or are they reacting to growing consumer preferences? Consider the dietary shifts and culinary trends emerging from the pandemic, such as a surge in home cooking, which likely fuels butter’s rise. Outputs like these, prompted by both an economic backdrop and evolving consumer demands, pose intriguing questions to the market. This exploration thus warrants a more profound analysis as stakeholders recalibrate to the evolving dairy product production landscape.

Stock Strategies: The Hidden Hands Behind Dairy Demand

Have you ever considered how inventory levels directly impact commercial use and the dairy supply chain? Consider the recent movements in butter and cheese stocks. Butter stocks have seen a steady decline since their peak in May, but intriguingly, they’ve been climbing in an annual context. For instance, July showed a 7.4% increase year-over-year by volume. But here’s the kicker: when you measure by days of commercial use in stock, that increase is just 1.5% for the same month. This tells us that the relationship between inventory volume and commercial use is nuanced. As more consumers reach for butter, the baseline stock levels necessary to keep shelves full also rise.

The cheese market tells a slightly different story. Since July 2023, cheese stocks have generally dropped. Could this be a sign of rising commercial use and demand exceeding production capacity? Or perhaps it hints at strategic adjustments within the supply chain to maintain balance amid fluctuating production rates and consumer preferences?

Pricing Puzzles: Butter and Cheese Lead the Dairy Dance

The price dynamics within the dairy market often resemble a volatile dance, particularly with products like butter and cheese leading the charge. Notably, in September, the National Dairy Product Sales Report marked a considerable rise in butter and cheese wholesale prices—up $0.40/lb and $0.35/lb, respectively, compared to the previous year. Meanwhile, September’s retail prices were not as straightforward, with butter climbing by $0.60/lb, yet cheddar cheese decreased by $0.12/lb.

Such fluctuations bear significant implications for both the market and consumers. From the producer’s standpoint, fluctuating wholesale prices can be a double-edged sword. While it offers the potential for higher revenue, it also introduces elements of unpredictability, affecting production planning and inventory management. Retail consumers face the brunt of these shifts, particularly in light of the Consumer Price Index for All Urban Consumers (CPI-U). Here’s where butter stands out: achieving a record-high CPI-U of 324.8 in September, ahead of general inflation.

These CPI-U figures are essential for interpretative context. They offer a glimpse into the purchasing power required by consumers today compared to decades ago, emphasizing the pressure on household budgets, especially for staples like dairy. Butter’s hike surpasses even margarine in the CPI-U stakes, highlighting butter’s elevated status in consumer expenses. On the contrary, fluid milk’s CPI-U remains more stable at 258.7, a brighter spot for cost-conscious buyers than 219.5 in nonalcoholic beverages.

In the grand scheme, these price movements reflect the immediate impact on consumer wallets and hint at underlying trends—perhaps a shift towards or away from certain products based on affordability and perceived value. As these trends develop, market players and consumers are urged to stay alert and adapt, ensuring supply aligns closely with demand while navigating the ever-changing pricing landscape.

Financial Currents in the Dairy Sector: Riding the Margin Wave or Weathering the Storm?

The recent shifts in milk and feed prices have certainly stirred the pot. With the Dairy Margin Coverage (DMC) program’s margin soaring to a remarkable $13.72 per cwt in August, the highest since this safety net’s inception in 2015, dairy farmers have much to ponder. This boost, driven by a substantial increase in the all-milk price to $23.60 per cwt, coupled with a drop in feed costs, begs the question: How will farmers navigate these financial waters?

This upward margin trend signals a potential opportunity for savvy dairy producers to reinvest in their operations, consider expansion, or diversify risk. The decreased feed costs, primarily attributed to lower corn prices, offer a welcomed reprieve. They could facilitate an increase in feed quality or allow savings to be channeled into other operational areas. Yet, there’s an inherent challenge: maintaining profitability if these prices become volatile again.

Furthermore, these price dynamics profoundly shape decision-making strategies. Farmers must weigh short-term gains against long-term sustainability. The heightened margins might tempt some to ride the wave of immediate profits without considering potential future fluctuations in market trends. A balanced approach, planning against both boom and bust cycles, will be crucial for enduring success in the competitive dairy landscape.

The Bottom Line

The USDA forecasts and WASDE reports hint at a distinctly dynamic future for the dairy industry, suggesting that producers should brace themselves for daunting tasks and potential opportunities. With the expected dip in U.S. milk production to 225.8 billion pounds, questions loom: How will this decrease impact dairy farmers’ strategies? Meanwhile, WASDE’s projection indicates a slip in the average all-milk price to $22.80/cwt, factors bound to affect budgeting and long-term planning.

As the market continues to evolve, with fluctuating production and prices, the implications for dairy operations are manifold. Depending on each farm’s or company’s position in the dairy ecosystem, these changes could herald adjustments in supply chain tactics, cost management, and product offerings.

Now is the time to examine these forecasts and consider their impact on your operations. How might these trends shape your strategic decisions in the future? Are you considering strategies to mitigate potential challenges or capitalize on anticipated opportunities? Let’s continue this conversation in the comments below. Your insights and experiences could offer invaluable perspectives to others in our community navigating this complex landscape.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

Join the Revolution!

Join the Revolution! Join the Revolution!

Join the Revolution!