Uncover the dynamics driving late-week surges in the milk markets. Witness the ascent of Class III and IV milk prices. Eager to learn about the latest movements in dairy and grain sectors? Continue reading.

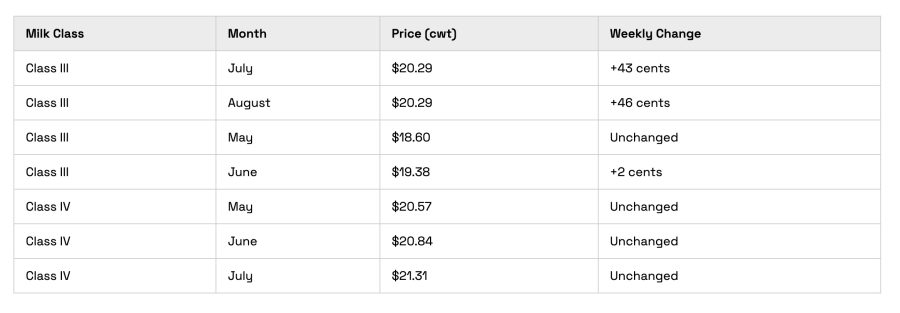

The milk markets experienced a volatile week, culminating in a significant late-week surge that notably impacted Class III and Class IV milk prices. The strength of class III milk, particularly in the latter half of the year, was a key highlight. July’s contracts saw a substantial increase of 43 cents to $20.29, while August mirrored this trend with a 46-cent climb to the same price of $20.29/cwt. In contrast, earlier months such as May and June were more subdued, with May closing at $18.60 and June showing a minimal increase of just 2 cents to $19.38/cwt.

Market analysts observed, “The late-week buying frenzy brought a refreshing upswing to the milk markets, particularly benefiting Class III prices in the latter months of the year.”

Class IV milk prices demonstrated a more tempered response, maintaining stability despite a modest gain in butter prices. May’s contracts settled at $20.57, June at $20.84, and July reached $21.31/cwt. These figures underscore the nuanced variations within the different milk classes, reflecting broader market dynamics and investor sentiment.

Class III Milk Prices Enjoy Summer Surge Amid Subdued Early-Year Performance

| Date | May | June | July | August |

|---|---|---|---|---|

| Monday | $18.60 | $19.36 | $19.86 | $19.83 |

| Tuesday | $18.60 | $19.37 | $19.96 | $19.94 |

| Wednesday | $18.60 | $19.38 | $20.09 | $20.05 |

| Thursday | $18.60 | $19.38 | $20.15 | $20.15 |

| Friday | $18.60 | $19.38 | $20.29 | $20.29 |

Class III milk experienced a notable improvement in the latter part of the year. July increased by 43 cents to reach $20.29 per hundredweight (cwt), while August followed with a rise of 46 cents, also hitting $20.29/cwt. In contrast, May ended at $18.60, showing little change, and June gained just 2 cents to close at $19.38/cwt. These numbers highlight a clear seasonal trend, with more robust market dynamics emerging in the summer months for Class III milk.

Class IV Milk Market Remains Steady Amid Modest Butter Price Gains

| Future | May | June | July |

|---|---|---|---|

| Monday | $20.57 | $20.84 | $21.31 |

| Tuesday | $20.57 | $20.84 | $21.31 |

| Wednesday | $20.57 | $20.84 | $21.31 |

| Thursday | $20.57 | $20.84 | $21.31 |

| Friday | $20.57 | $20.84 | $21.31 |

The week in the dairy market has displayed notable shifts, particularly in the Class IV milk futures. Despite the muted movement, the overall trend leans toward stability with a few upward adjustments compensating for earlier lukewarm phases. For a clearer illustration, let’s delve into the Class IV milk futures trends over the past week:

Class IV milk prices remained steady compared to Class III, showing minimal volatility. Class IV milk held its ground despite a modest 6-cent rise in butter prices. May closed at $20.57/cwt, June slightly up at $20.84, and July continued this trend at $21.31. These figures highlight a consistent market with gradual gains, reflecting the steady performance of Class IV milk.

The CME Spot Trade Closes the Week with Significant Activity in the Dairy

| Product | Monday | Tuesday | Wednesday | Thursday | Friday | Weekly Trend |

|---|---|---|---|---|---|---|

| Butter ($/lb) | $3.03 | $3.04 | $3.05 | $3.07 | $3.09 | ▲6 cents |

| Cheddar Blocks ($/lb) | $1.81 | $1.81 | $1.81 | $1.81 | $1.81 | ─ |

| Cheddar Barrels ($/lb) | $1.94 | $1.94 | $1.94 | $1.94 | $1.94 | ─ |

| Dry Whey ($/lb) | $0.41 | $0.41 | $0.41 | $0.41 | $0.41 1/2 | ▲1/2 cent |

| Grade A Non Fat Dry Milk ($/lb) | $1.16 | $1.16 | $1.16 | $1.16 | $1.16 3/4 | ▲3/4 cent |

The CME spot trade saw significant action in the dairy sector, especially in the butter and cheese markets. Butter prices rose 6 cents to $3.09 per pound, hinting at increased demand or limited supply, which could positively impact the broader dairy market.

Cheddar cheese prices remained stable, with Blocks at $1.81 and Barrels at $1.94 per pound. This consistency suggests a balanced market without primary surpluses or deficits.

The block/barrel spread stayed inverted at 13 cents, indicating supply concerns or quality preferences. Typically, Blocks are pricier due to their broader use and better quality. The sustained average price of $1.87 1/2 per pound reflects the market’s effort to balance these differences, providing insight into future price trends in the dairy sector.

Powder Markets Show Promise with Incremental Price Gains

| Product | Price (per lb) | Change | Trend |

|---|---|---|---|

| Dry Whey | $0.41½ | +1 cent | Up |

| Grade A Non Fat Dry Milk | $1.16¾ | +½ cent | Up |

The powder markets exhibited a solid performance this past week, signaling promise in this sector. Dry Whey climbed by a penny to $0.41 1/2 per pound, indicating a steady demand. This rise may suggest market stability amid fluctuating dairy prices.

Grade A Non-Fat Dry Whey also increased by 1/2 cent, reaching $1.16 3/4 per pound. This small but significant uptick reflects the strength of the dairy industry and hints at a balanced supply and demand. These incremental gains not only reinforce market stability but also inspire confidence in the potential growth of the powder markets, which could have broader economic implications for those invested in commodities.

Grain and Feed Markets Reflect Broader Economic and Environmental Instabilities

| Commodity | Contract Month | Closing Price | Price Change |

|---|---|---|---|

| Corn | July | $4.46 1/4 | Down 2 1/2 cents |

| Soybeans | July | $12.05 | Down 4 3/4 cents |

| Soybean Meal | July | $364.10/ton | Up $1.10 |

| Wheat | July | $6.78 | Down 2 1/2 cents |

| Rice | July | $17.67 | Down 16 cents |

| Feeder Cattle | August | $256.40 | Down $2.67 |

The grain and feed markets faced a notable shift towards the weekend, marked by varied price movements across critical commodities. Corn slipped slightly, with July futures closing at $4.46 1/4, down 2 1/2 cents. This minor dip mirrors broader market trends where corn battles to sustain momentum amid changing demand-supply dynamics. Soybeans followed suit, with July futures dropping 4 3/4 cents to $12.05 per bushel, reflecting ongoing market volatility and the impact of trade conditions and weather on crop yields.

Despite a modest rise in soybean meal prices, the feed markets remained complex. July prices increased by $1.10, finishing the week at $364.10 per ton. However, prices remained over $25 per ton below earlier weekly highs, underscoring the intricate and volatile nature of the feed markets. These shifts serve as a reminder of the need for caution in the grain and feed sectors, mirroring the broader economic and environmental uncertainties.

The Bottom Line

The week concluded with a notable rise in milk markets, spurred by a robust late-week surge in Class III milk. Gains in July and August highlighted its strength, contrasting a quieter early-year performance. Class IV milk displayed a steadiness, with modest butter price increases.

Significant activity marked the CME spot trade, with butter and cheese showing price movements and powder markets finishing the week with gains. In contrast, grain and feed markets slid into the weekend, impacted by economic and environmental challenges. Corn, soybeans, and soybean meal exhibited varied performances, reflecting the intricate dynamics of agricultural markets.

Key Takeaways:

- Class III milk prices experienced an encouraging surge in late-week trading, showing notable gains for July and August contracts.

- Earlier months like May and June saw more modest price movements, with minimal increases observed.

- Class IV milk prices remained relatively stable, with slight upward adjustments despite varied commodity performance within the dairy market.

- The CME spot trade highlighted a 6-cent gain in Butter prices, while Cheddar Blocks and Barrels maintained their previous levels, keeping the block/barrel spread inverted.

- Powder markets closed the week on a positive note, with Dry Whey and Grade A Non-Fat Dry Whey inching upward.

- Grain and feed markets displayed downward trends, with slight declines in corn and soybeans and a notable drop in soybean meal from earlier highs.