Despite challenging weather and margin complications, each of the major dairy states saw volumes rise. Production growth was driven by both stronger yields and a modestly larger herd.

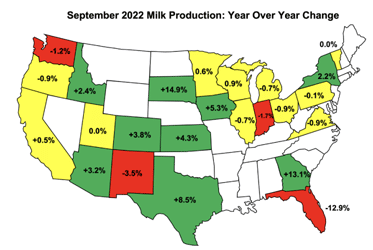

U.S. dairy producers forged ahead in September, posting increases in milk production for the third consecutive month. Totaling 18.282 billion pounds, production was 1.5% greater than in the same month last year. This represents moderately slower growth than the 1.7% reported in August as USDA revised their data up for that month. Despite challenging weather and margin complications, each of the major dairy states saw volumes rise. California, Wisconsin, and Idaho saw output increase by 0.5%, 0.9%, and

2.4%, respectively. Texas, now clearly the country’s fourth largest dairy state, saw volumes soar by 8.5%. Production in the Lone Star state was just 34 million pounds shy of Idaho’s production during the month.

Production growth was driven by both stronger yields and a modestly larger herd. Yields rose to 1,943 pounds per cow during the month, up 1.4% versus last year’s value. Meanwhile, at 9.411 million head, the national herd was 6,000 cows larger than last September. However, USDA made important revisions to their herd number

estimates in recent months. While previous numbers illustrated a herd that was growing through the summer, updated data now shows that the herd peaked in May at 9.419 million head, and has been gradually declining ever since.

U.S. producers are likely to face headwinds in the coming months, decreasing the likelihood that production will grow in a material way. Margins are coming under increased pressure as milk prices retreat from their highs while operating costs remain elevated relative to historical standards. This situation is not unique to the United States. Similar circumstances are affecting producers in other global supply regions where weather challenges and regulatory shifts are further restricting production. Looking forward, it seems difficult to believe that global milk production could grow in a significant way, which is likely to keep dairy commodity prices above historical averages over the near term.

At the Global Dairy Trade (GDT) auction held earlier this week, the GDT index fell once again by 4.6%, the second consecutive decline. Lower prices were seen across every product though milk powders fared the worse. Skim milk powder and whole milk powder prices fell by 6.9% and 4.4%, respectively, relative to the prior event. Prices are now well off their highs achieved in March and April of this year, though they remain elevated relative to historical values.

As autumn advances, cooler temperatures have ushered in stronger milk volumes and higher component levels in most parts of the country. Market participants indicate that demand has been solid from both bottlers and manufacturers and spot loads are moving around the country to fulfill their best use. Cream availability has increased, and multiples have fallen, even as demand from both Class II users and butter churns has remained strong.

Even with active churning activity and increased cream availability, spot butter prices remained elevated at the CME this week. On the heels of a small dip on Monday, a 3.25¢ gain on Tuesday pushed the butter market up to $3.20/lb. where it remained for the balance of the week. Activity was quiet, however, as no loads traded hands over the five trading days. Strong demand from the retail sector has played a key role in keeping the market supported and some participants speculate that prices will begin to retreat once retail buyers have filled their holiday orders.

On the other side of the Class IV complex, nonfat dry milk (NDM) markets continue to sink. The spot market lost ground in everyday of trading this week, ending Friday’s session at $1.42/lb. down 7¢ compared to last week’s close. Demand is lethargic, especially from international clients. Mexican buyers continue to perch on the sidelines waiting for prices to fall further before resuming their purchasing. Some are optimistic that we are nearing price levels that will be sufficient to reignite demand from south of the border.

Cheddar markets were volatile this week, with most of the activity taking place in the barrel trade. CME Cheddar barrels moved up during the first half of the week, stretching the inverted block-barrel spread as wide as 16¢ on Wednesday. Then, the tides turned and a 6¢ and 5.5¢ loss on Thursday and Friday pulled the barrel price back down to $2.09/lb., down 3.5¢ compared to last week. The block markets were more reserved with only a three-quarter cent gain on Thursday. Blocks wrapped up Friday’s session at $2.0575/lb. reducing the inverted block barrel spread to 3¢.

Cheesemakers have been active but the relationship between supply and demand has been sufficient to keep tension in the markets, especially for barrels. Foodservice and export demand has generally remained steady however retail demand has begun to weaken. Dairy Market News reports that some retail consumers are, “buying smaller cheese packages or switching to private label brands.”

Whey markets only observed modest fluctuations during the week. Robust cheese production has kept a steady whey stream available for driers. Meanwhile demand has been understated. At the CME, the dry whey market dipped slightly on Tuesday and Wednesday before posting a half penny gain on Thursday. Ultimately the market finished the week at 44¢ per pound, a quarter cent decrease compared to last week.

While daily values ebbed and flowed, grain markets moved mostly sideways this week. Corn futures settled on Friday within a few cents per bushel of Monday’s settlements. Meanwhile, soybean futures saw some modest increases with nearby contracts adding about a dime per bushel over the week. With corn contracts above $6.80/bu. and soybean above $14/bu. in the first half of next year, it appears that stubbornly high feed prices will continue to be a thorn in dairy producers’ sides in the coming months.

Source: Jacoby Dairy Product Merchants