The T.C. Jacoby Weekly Market Report Week Ending August 25, 2023

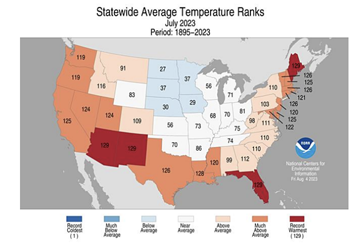

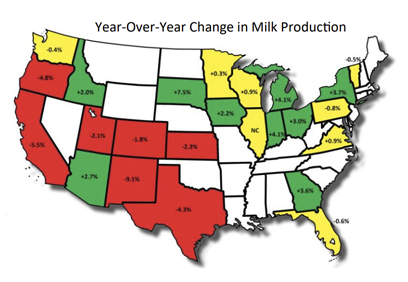

U.S. milk output turned negative in July, as the heat took a terrible toll on milk yields. The milk production map and the July weather maps look nearly identical. The August weather map – and presumably the milk production map – will look much different.

U.S. milk output turned negative in July, as the heat took a terrible toll on milk yields. Milk  output totaled 19.08 billion pounds last month, down 0.5% from July 2022. The milk production map and the July weather maps look nearly identical. Simply put, milk output was down hardest where it was hottest. The August weather map – and presumably the milk production map – will look much different. Tropical Storm Hilary brought unusually mild temperatures to the West Coast, but the Upper Midwest is scorching. Through much of the summer, dairy producers in the heartland reported only modest declines in milk yields relative to the spring peak. But the bulk tanks are not as full today.

output totaled 19.08 billion pounds last month, down 0.5% from July 2022. The milk production map and the July weather maps look nearly identical. Simply put, milk output was down hardest where it was hottest. The August weather map – and presumably the milk production map – will look much different. Tropical Storm Hilary brought unusually mild temperatures to the West Coast, but the Upper Midwest is scorching. Through much of the summer, dairy producers in the heartland reported only modest declines in milk yields relative to the spring peak. But the bulk tanks are not as full today.

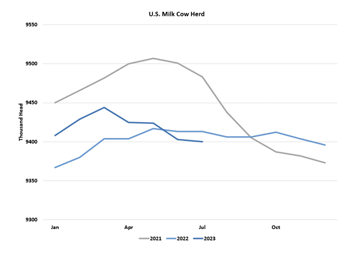

Dairy producers cashed a paltry milk check and some surprisingly large beef checks in July, and they culled hard. But the dairy herd barely budged. USDA estimates the dairy herd shrank by only 3,000 head in July. But the agency cut another 5,000 head from its estimate of the  June milkcow head count, bringing the May-to-June decline to a steep 21,000 head. There were 9.4 million cows in U.S. milk parlors last month, 13,000 fewer than there were a year ago. A steeper setback in cow numbers is likely in August. Setting aside slaughter volumes in 1986 during the cow-kill program, dairy slaughter volumes have been record high for this time of year in four of the last seven weeks.

June milkcow head count, bringing the May-to-June decline to a steep 21,000 head. There were 9.4 million cows in U.S. milk parlors last month, 13,000 fewer than there were a year ago. A steeper setback in cow numbers is likely in August. Setting aside slaughter volumes in 1986 during the cow-kill program, dairy slaughter volumes have been record high for this time of year in four of the last seven weeks.

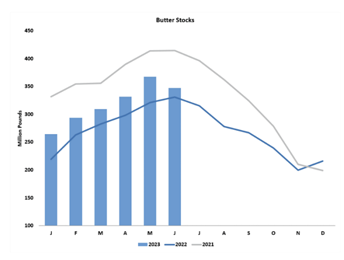

Both cheese and butter stocks tightened in July, which helps to explain the strong showing for both commodities in the spot markets last month. Butter inventories dropped 20.4 million pounds from June to July, an unusually steep decline. There were 347.5 million pounds of butter in cold storage warehouses last month. That’s 5% more than the very small volumes reported a year ago but considerably less than the mountain of butter in storage in July 2021.

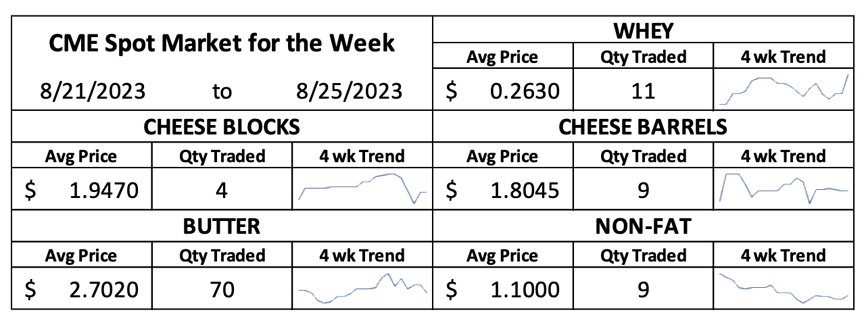

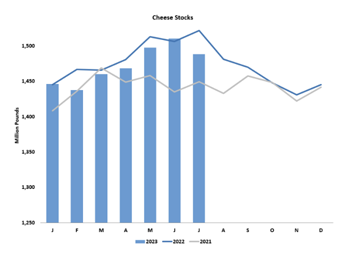

In recent years, cheese stocks have typically grown from June to July, so this year’s 21.75-million-pound setback surprised. Cheese inventories tipped the scales at 1.489 billion pounds last month. That’s a lot of cheese, to be sure, but it’s 2.2% less than last year. The month-tomonth decline suggests that export deals booked earlier in the year helped keep product moving this summer. But today, with prices much higher, there are likely few buyers willing to return U.S. cheese exporters’ calls. After topping $2 last week, CME spot Cheddar blocks retreated, falling 8.25ȼ to a still lofty $1.945 per pound. Barrels slipped 0.75ȼ to $1.80. Butter also fell back from the recent highs, dropping 3ȼ to $2.67.

In recent years, cheese stocks have typically grown from June to July, so this year’s 21.75-million-pound setback surprised. Cheese inventories tipped the scales at 1.489 billion pounds last month. That’s a lot of cheese, to be sure, but it’s 2.2% less than last year. The month-tomonth decline suggests that export deals booked earlier in the year helped keep product moving this summer. But today, with prices much higher, there are likely few buyers willing to return U.S. cheese exporters’ calls. After topping $2 last week, CME spot Cheddar blocks retreated, falling 8.25ȼ to a still lofty $1.945 per pound. Barrels slipped 0.75ȼ to $1.80. Butter also fell back from the recent highs, dropping 3ȼ to $2.67.

As always, the milk powder market took its cues from abroad. Whole milk powder (WMP) prices lost a little more ground at Tuesday’s Global Dairy Trade Pulse auction, and U.S. nonfat dry milk (NDM) values faded early in the week. Then after European and Kiwi skim milk powder (SMP) futures strengthened, CME spot NDM bounced back. It closed the week at $1.105, on par with last Friday.

As always, the milk powder market took its cues from abroad. Whole milk powder (WMP) prices lost a little more ground at Tuesday’s Global Dairy Trade Pulse auction, and U.S. nonfat dry milk (NDM) values faded early in the week. Then after European and Kiwi skim milk powder (SMP) futures strengthened, CME spot NDM bounced back. It closed the week at $1.105, on par with last Friday.

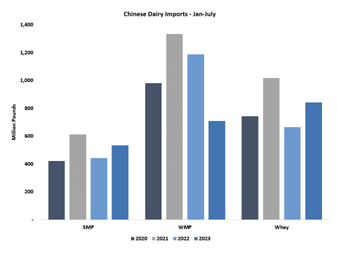

The milk powder trade is desperately searching for any sign that Chinese WMP imports are set to improve. If you squint, the data looked a  little less troubling than they once did. Chinese WMP imports topped year-ago volumes in May, June, and July. On its own, the monthly figures seem encouraging, with July WMP imports up 22.5% from a year ago. But a wider view paints a different picture. China is simply not importing WMP at the pace required to make up for this year’s very slow start. Chinese WMP imports are down 40.3% from last year to the lowest January through June total since 2016. Chinese imports of other dairy products look much better, with year-to-date imports of cheese, SMP, and whey at their second-highest totals on record, behind 2021.

little less troubling than they once did. Chinese WMP imports topped year-ago volumes in May, June, and July. On its own, the monthly figures seem encouraging, with July WMP imports up 22.5% from a year ago. But a wider view paints a different picture. China is simply not importing WMP at the pace required to make up for this year’s very slow start. Chinese WMP imports are down 40.3% from last year to the lowest January through June total since 2016. Chinese imports of other dairy products look much better, with year-to-date imports of cheese, SMP, and whey at their second-highest totals on record, behind 2021.

Whey prices finally firmed this week. Spot whey climbed a penny to 28ȼ, their best showing in more than two months. USDA’s Dairy Market News explains, “Limited milk availability for cheese processing, along with recently firming high protein blend markets have created a slightly bullish safety net for a market that has been struggling to gain traction for the better part of the calendar year.”

Whey prices finally firmed this week. Spot whey climbed a penny to 28ȼ, their best showing in more than two months. USDA’s Dairy Market News explains, “Limited milk availability for cheese processing, along with recently firming high protein blend markets have created a slightly bullish safety net for a market that has been struggling to gain traction for the better part of the calendar year.”

Spot market action did not imply big gains for the dairy markets this week. But heat in the cheese states and a friendly Cold Storage report propelled Class III futures sharply higher. The September contract climbed 45ȼ to $18.94 per cwt. October Class III jumped 66ȼ to $18.65. The Class IV markets were less exuberant. September Class IV fell 35ȼ to $18.90, and deferred contracts lost a little ground as well.

The Corn Belt heat wave and the ProFarmer crop tour gave the grain trade a lot to chew on this week. After taking corn and soybean samples in seven states, the tour pegged the national average corn yield at 172 bushels per acre, below USDA’s August estimate of 175.1 bushels but comfortably near the market consensus. ProFarmer assessed the soybean yield at 49.7 bushels per acre, also below USDA’s August figure at 50.9 but slightly above last year’s tour average at 49.5.

The trade assumes that the soaring temperatures will not help either row crop, but, judging by the calendar, the impact will be much more severe for soybeans than for corn. With that in mind, November soybeans surged 34.5ȼ this week to $13.8775 per bushel and December soybean meal jumped $26 to $415 per ton. December corn futures bounced around but ultimately finished at $4.88, a nickel lower than last Friday.

Original Report At: https://www.jacoby.com/market-report/heat-takes-a-terrible-toll-on-milk-yields/